Hunter Syndrome Treatment Market Size, Share & Industry Analysis, By Treatment (Enzyme Replacement Therapy (ERT), and Others), By Route of Administration (Intravenous, and Intracerebroventricular (ICV)/ Intrathecal), By End User (Hospitals, Specialty Clinics and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

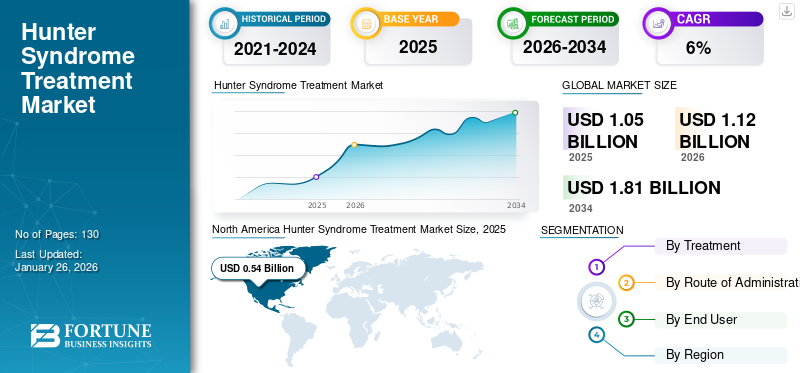

The global hunter syndrome treatment market size was valued at USD 1.05 billion in 2025, The market is projected to grow from USD 1.12 billion in 2026 to USD 1.81 billion by 2034, exhibiting a CAGR of 6.20% during the forecast period. North America dominated the hunter syndrome treatment market with a market share of 50.84% in 2025.

Hunter’s syndrome, also known as Mucopolysaccharidosis II and MPS II, is one of the key diseases which is part of the mucopolysaccharidosis group of inherited conditions in which the body is unable to properly breakdown mucopolysaccharides, a form of sugar molecule. Hunter’s syndrome is a very rare inherited genetic disorder which primarily affects males. When left untreated, Hunter syndrome is potentially lethal and leads to a shorter life span of the individuals diagnosed. There are various clinical trials being conducted by market players for the development of new Hunter syndrome Treatment, especially the neurological symptoms and complications.

Hunter Syndrome Treatment Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 1.05 billion

- 2026 Market Size: USD 1.12 billion

- 2034 Forecast Market Size: USD 1.81 billion

- CAGR: 6.20% from 2026–2034

Market Share:

- North America held the largest share at 50.84% in 2025, driven by higher diagnosis and treatment rates for rare diseases, strong reimbursement policies, and the presence of major biopharmaceutical companies with active clinical pipelines.

- By Treatment: Enzyme Replacement Therapy (ERT) dominated in 2024 due to the market reliance on the only two approved drugs—Elaprase and Hunterase—both of which are ERTs. This segment maintains leadership as these therapies are the current standard for Hunter syndrome.

Key Country Highlights:

- Japan: Demand growth supported by the presence of Hunterase, favorable regulatory approvals, and increasing diagnosis rates for mucopolysaccharidosis (MPS) disorders.

- United States: Strong reimbursement coverage for orphan drugs, higher awareness, and active clinical research pipelines, including advanced enzyme replacement and gene therapy trials.

- China: Large underdiagnosed patient pool, improving rare disease awareness, and government initiatives to expand access to orphan disease treatments.

- Europe: Growing adoption of ERTs, supportive rare disease policies, and ongoing introduction of advanced therapies, with countries like Germany and the U.K. at the forefront of treatment availability.

MARKET TRENDS

Increasing R&D for rare diseases to augment market growth

One of the key market trends prevailing in the Hunter syndrome Treatment market is the increasing R&D investments by key players for the development of novel therapies. Since, Hunter syndrome is a key orphan disease, a number of prominent clinical stage biopharmaceutical companies such as ArmaGen and REGENXBIO Inc. have strong pipeline candidates in various stages of clinical trials. This increasing interest into rare diseases’ therapeutics is due to the fact that major pharmaceutical breakthroughs leading to the development of blockbuster drugs are more probable in these diseases as compared to the traditional pharmaceutical portfolios.

Another driving factor for this trend is that the pharmaceutical companies are required to run larger outcome studies for the approval of traditional therapeutics for diseases such as diabetes and coronary artery disease (CAD) as compared to the approval for orphan diseases such as Hunter syndrome. This is projected to further propel the mucopolysaccharidosis II treatment market growth during the forecast period.

Download Free sample to learn more about this report.

MARKET DRIVERS

Unmet clinical needs and need for better treatment outcomes to fuel demand

One of the critical market drivers of the market is the lack of presence of multiple therapeutics for the patients and also presence of the monopoly of one therapeutic, Elaprase. Elaprase is a particularly expensive treatment option and often patients from emerging countries do not have access to such therapeutics. Patients without the access to proper treatment often have significantly shorter life span compared to their counterparts in the developing countries who often have access to these expensive therapeutics.

Apart from Elaprase, the only other approved therapeutic is Hunterase, which is only approved in some of the countries. Despite that, the cost of Hunterase is prohibitively high, and patients in the emerging countries such as India, often cannot afford these therapeutics in spite of increasing governmental initiatives. Introduction of low cost and effective therapeutics is anticipated to drive the growth of the global market during the forecast period.

The other critical driver is the need for better clinical and therapeutic outcomes for the patients for Hunter syndrome. The currently approved and used therapeutics such as Elaprase, are not capable of crossing the blood-brain barrier. Hence, these therapeutics are not able to effectively manage the neurological symptoms and complications of the severely affected patients of Hunter syndrome. In the severely affected patients of Hunter syndrome, which affects an estimated two-thirds of the total patient population, the neurological symptoms are severely debilitating.

The currently utilized therapeutics are not able to reach the central nervous system, thus a significant proportion of the population remains ineffectively treated. This is projected to drive the demand for advanced therapeutics which aid in the management of all types of the symptoms of the Hunter syndrome and drive the growth of the Hunter syndrome drug market size during the forecast period.

Presence of key pipeline candidates in the r&d pipelines of market players to drive the market growth

There is an increasing R&D activity in the development of efficient therapeutics for a number of orphan diseases and Hunter syndrome is one of these diseases. According to the Genetic and Rare Diseases Information Center (GARD), there can be an estimated 7,000 rare diseases and the total number of individuals in the U.S. from these rare diseases can be 25-30 million. According to an analysis published on The Pharma Letter in April 2019, it was estimated that in Japan, approximately 150 individuals suffered from Hunter syndrome.

Such patient statistics and trends are further leading to the presence of significant pipeline candidates in the pipelines of prominent companies. A number of prominent clinical stage biopharmaceutical companies such as ArmaGen, Denali Therapeutics, and REGENXBIO Inc., all have pipeline candidates for Hunter syndrome in several stages of clinical trials. The above factors combined with the need for efficient therapeutics is further projected to fuel the demand for these drugs and boost the Hunter syndrome treatment market growth.

MARKET RESTRAINT

High cost of approved therapeutics and lower treatment rates in emerging countries to limit the adoption of hunter syndrome therapeutics

Despite increasing incidence of rare diseases such as Hunter syndrome globally, and higher prevalence of these conditions in emerging regions such as Asia, there are certain factors that are limiting the adoption of these therapeutics. One of the major factors restraining the growth of the market is lower treatment rates in emerging countries due to the high costs attributable to these enzyme replacement therapies (ERT), which is the primary treatment for Hunter syndrome.

This has led to a limited number of patients undergoing treatment, and a significant proportion of the patients of Hunter syndrome are left without treatment. Often, these treatment options are not accessible to the patients in the emerging countries due to lack of awareness and also appropriate payment plans for these diseases. The governments in these countries are highly unaware of these diseases and do not adequately reimburse them, which leads to the creation of these major factors restraining Market growth for the Hunter Syndrome Treatment.

SEGMENTATION

By Treatment Analysis

To know how our report can help streamline your business, Speak to Analyst

Enzyme replacement therapy (ERT) dominated the global market

The Enzyme Replacement Therapy (ERT) segment is projected to dominate the market with a share of 93.38% in 2026. Based on treatment, the global market is segmented into enzyme replacement therapy (ERT), and others. Since, Hunter syndrome belongs to a group of disorders called lysosomal storage disorders, the primary treatment for such disorders is enzyme replacement therapy (ERT). Hence, the enzyme replacement therapy (ERT) segment dominated the Hunter syndrome therapeutics market share in 2024. The only two therapeutics approved by the regulatory agencies globally: Elaprase and Hunterase are both ERTs and have been instrumental in the dominance of this segment in the global market.

The others segment is anticipated to grow at a comparatively higher CAGR. The increasing clinical trials involving the usage of the hematopoietic stem cell transplant (HSCT) is also anticipated to take place during the forecast period and drive the MPS II treatment market growth during the forecast period. Apart from the increasing trials by stem cell transplantation, a number of key clinical stage biopharmaceutical companies are conducting trials on gene therapy as a means of treatment for Hunter syndrome.

By Route of Administration Analysis

Clinically proven effectiveness of intravenous therapeutics in hunter syndrome to aid dominance of the segment

The Intravenous segment is expected to lead the market, contributing 97.46% globally in 2026. In terms of route of administration, the market is segmented into intravenous, and intracerebroventricular (ICV)/ intrathecal. The intravenous type is anticipated to dominate the route of administration segment, because of the most prominent Hunter syndrome treatment, Elaprase is administered intravenously. Elaprase holds a monopoly over the Hunter syndrome therapeutics market and is anticipated to hold control over its market share in the forecast period, is primary reason for dominance of intravenous type in the global Hunter syndrome drugs market.

Hunterase is the other approved therapeutic and the route of administration is intracerebroventricular (ICV)/ intrathecal. Growing approvals in other countries of these therapeutic, along with introduction in other countries of the market, is expected to drive the growth of the segment during the forecast period.

By End User Analysis

Higher administration of therapeutics at hospitals to enable dominance of the segment

The Hospitals segment will account for 61.70% market share in 2026. In terms of end user, the hunter syndrome treatment market is segmented into hospitals, specialty clinics, and others. One of the key reasons for the dominance of hospitals segment is that the therapeutics used in Hunter syndrome treatment can often be administered in hospital settings with trained medical professionals. This enables the proper adherence to the Hunter syndrome treatment guidelines and also the appropriate and safe administration of critical therapeutics which have to be administered intravenously. Such effective treatment often allows for the appropriate control of Hunter syndrome symptoms.

Growing number of specialty clinics, along with the high level of specialist care for the Hunter syndrome patients, are some of the major factors responsible for growth of this segment in the forecast period.

These factors, along with emphasis of national government agencies for treatment of patients in advanced settings, is further fueling the demand for Hunter syndrome treatment in the global market.

REGIONAL ANALYSIS

North America Hunter Syndrome Treatment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America dominated the market with a valuation of USD 0.54 billion in 2025 and USD 0.57 billion in 2026. The MPS II treatment market size in North America stood at USD 0.51 Billion in 2024. The market in the region in characterized by higher diagnosis and treatment rates for these rare conditions, coupled with adequate reimbursement policies for these therapeutics. These factors, along with higher awareness among patient population towards new treatment options and the presence of major clinical stage biopharmaceutical companies are their pipeline candidates, are responsible for dominant share of the region in the global market. The market in Europe and Asia-Pacific is projected to register comparatively higher CAGR during the forecast period. The presence of key products in the region, are anticipated to drive the demand for Hunter syndrome drugs in Europe during 2025-2032. The U.S. market is expected to reach USD 0.53 billion by 2026.

Asia Pacific

Expected presence of some therapeutics such as Hunterase in Japan in Asia Pacific, and the presence of a large and underpenetrated market in the region, together are projected to drive the Hunter syndrome therapeutics market growth in Asia Pacific during forecast period. The rest of the world market comprises of Latin America and the Middle East & Africa and is currently in nascent stage. However, developing healthcare infrastructure in these regions and growing awareness of orphan disorders is projected to fuel the Hunter syndrome therapeutics market demand during forecast period. The Japan market is expected to reach USD 0.10 billion by 2026, the China market is expected to reach USD 0.03 billion by 2026, and the India market is expected to reach USD 0.07 billion by 2026.

KEY INDUSTRY PLAYERS

Key Product offering and core focus on rare diseases of Shire (Takeda Pharmaceutical Company Limited), to help the company to retain a leading position

Competition landscape of Hunter syndrome treatment market depicts a monopoly dominated by Shire (now owned by Takeda Pharmaceutical Company Limited). The key and only product offering of Elaprase (idursulfase), its efficiency in terms of treatment outcomes and also its indispensability in key markets, are prominent factors responsible for the dominance of the company.

However, certain prominent clinical stage biopharmaceutical companies such as ArmaGen, and REGENXBIO Inc., have entered the monopoly market of Hunter syndrome treatment with their potential drug candidates. This is projected to positively impact the global market as these companies are poised to gain market share during the forecast period through key regulatory approvals.

LIST OF KEY COMPANIES PROFILED:

- Shire (Takeda Pharmaceutical Company Limited)

- Denali Therapeutics

- ArmaGen

- Inventiva

- Green Cross Corp. (GC Pharma)

- CANbridge Life Sciences Ltd.

- JCR Pharmaceuticals Co., Ltd.

- REGENXBIO Inc.

- Sangamo Therapeutics

- Others

KEY INDUSTRY DEVELOPMENTS:

- July 2021 – Denali therapeutics Inc. announced positive results from their clinical study which evaluates the ETV: IDS, an investigational brain-penetrant enzyme replacement therapy for the treatment of peripheral manifestations of Hunter Syndrome. The results will be presented at the 16th International Symposium on MPS and related diseases.

- May 2021 –Inventiva a biopharmaceutical company, announced that they will participate in Jefferies Virtual Healthcare Conference. The company is responsible for the development of oral small molecule therapies for mucopolysaccharidoses (MPS) and other diseases which have unmet needs. During this conference the company will present their corporate overview and engage in investors meeting.

- March 2018 – Shire (Takeda Pharmaceutical Company limited) announced a strategic partnership with NanoMedSyn, to examine potential enzyme replacement therapies for lysosomal storage disorders.

REPORT COVERAGE

The Hunter syndrome treatment market report provides a detailed analysis of the market dynamics and focuses on key aspects such as prevalence of Hunter syndrome, by key regions, 2018, pipeline analysis, key industry developments, regulatory scenario by key regions, overview of emerging treatments for Hunter syndrome, and, reimbursement scenario by key regions. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over the recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD million) |

|

Segmentation |

By Treatment

|

|

By Route of Administration

|

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.05 billion in 2025 and is projected to reach USD 1.81 billion by 2034.

In 2025, the market value stood at USD 1.05 billion.

Growing at a CAGR of 6.20%, the market will exhibit steady growth in the forecast period (2026-2034).

Enzyme Replacement Therapy (ERT) segment is expected to be the leading segment in this market during the forecast period.

Anticipated introduction of more advanced therapeutics in the market, coupled with significant unmet clinical need, is fueling the demand for Hunter syndrome treatment market.

Shire (Takeda Pharmaceutical Company Limited) is the leading player in the global market.

North America dominated the market share in 2025.

Growing R&D and clinical trials by market players is leading to the development of advanced and efficient therapeutics for Hunter syndrome treatment in the market.

- 2021-2034

- 2025

- 2021-2024

- 130

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us