Home / Healthcare / Pharmaceutical / Plasma Fractionation Market

Plasma Fractionation Market Size, Share & Industry Analysis, By Product (Albumin, Immunoglobulin (Intravenous Immunoglobulin (IVIG), Subcutaneous Immunoglobulin (SCIG)), Coagulation Factors (Factor IX, Factor VIII, Prothrombin Complex Concentrates, Fibrinogen Concentrates, and Others), Protease Inhibitors, and Others), By Application (Immunology & Neurology, Hematology, Critical Care, Pulmonology, and Others), By End-user (Hospitals & Clinics, Clinical Research Laboratories, and Others), and Regional Forecast, 2024-2032

Report Format: PDF | Latest Update: Dec, 2024 | Published Date: Apr, 2024 | Report ID: FBI101614 | Status : PublishedThe global plasma fractionation market size was valued at USD 32.83 billion in 2023 and market is projected to grow from USD 35.21 billion in 2024 to USD 62.83 billion by 2032, exhibiting a CAGR of 7.5% during the forecast period (2024-2032). North America dominated the global Plasma Fractionation Market with a market share of 55.86% in 2023.

Plasma fractionation is a manufacturing process separating plasma proteins to develop various therapies. The fractionation of human plasma is the fundamental approach to developing several life-saving protein therapies comprising a range of coagulation factors, albumin, immunoglobulins, protease inhibitors, and others.

The clinical usage of these plasma-derived medicinal products generally encompasses substitute intravenous protein therapy for treating immunological, hemostatic, metabolic disorders, and other life-threatening disorders.

The growing burden of various disorders, such as primary immunodeficiencies, and increasing demand for plasma derived products to prevent shock following burns, serious injury, and others are propelling the market's growth. Furthermore, to cater to the rising demand, many prominent players operating in the market are investing heavily in R&D activities and expanding manufacturing capabilities to launch new plasma-derived products. Therefore, major company's strategic efforts are expected to drive market growth.

The plasma fractionation market witnessed a slow growth during the COVID-19 pandemic due to the plasma collection process disruption. Furthermore, strict guidelines implemented during the pandemic resulted in a decline in the plasma centers' plasma volume. Many key players operating in the market observed a decrease in their revenue during the pandemic. However, the market regained normalcy post-pandemic due to the upliftment of the stringent regulations implemented during the pandemic. Companies have witnessed a significant increase in their plasma collection volume and revenue in the post-pandemic years.

Plasma Fractionation Market Trends

Launch of New Technologies by Key Players to Augment Market Growth

The plasma fractionation process involves breaking down plasma into various individual proteins, such as albumin, immunoglobulin, coagulation factors, and protease inhibitors, for clinical use. Major key players in this market have their plasma fractionation centers where they can extract such proteins. The current demand for plasma-derived therapies has led to the launch of various technologies that can make the process faster.

- For instance, in April 2021, GEA delivered a new separator technology to Biopharma S.A. in its new plant in Bila Tserkva, Ukraine.

In March 2022, the U.S. Food and Drug Administration also cleared Terumo Corporation’s BCT collection system to meet the increasing demand for plasma-derived therapies. Rika Plasma Donation System is said to be a next-generation automated technology designed to meet the growing demand for plasma-derived therapies. On average, the device can complete plasma collection within 35 minutes, ensuring that at one time, there are not more than 200 milliliters of blood outside the donor’s body. The continuous efforts by various players to introduce technologies for the plasma fractionation process will augment the growth opportunities for the market over the forecast period.

Plasma Fractionation Market Growth Factors

Rising Incidence of Immunodeficiency and Rare Disorders to Augment Market Growth

Plasma-derived medicinal products are generally used to replace deficient proteins in an individual. Products derived from plasma aid in treating rare conditions affecting a relatively smaller proportion of the population. There is an exponential surge in the demand for plasma-derived therapies across the globe due to the rising burden of various immunodeficiency and rare genetic disorders.

Bleeding disorders, such as von Willebrand disease, Hemophilia, and others, are rare genetic disorders that result from a lack of certain clotting factors, such as factor VIII, factor IX, and others. The growing cases of bleeding disorders across the globe are one of the key factors contributing to the rising demand for plasma fractionated products.

- For instance, according to the global survey published by the World Federation of Hemophilia 2022, 454,690 people were suffering from bleeding disorders across the globe in 2022, compared to 393,658 in 2020.

Moreover, primary immunodeficiency is a group of 300 diseases characterized by recurrent chronic infections, autoimmunity, allergy, or inflammation. These infections are a consequence of genetic alteration, which affects the immune system. The treatment for such disorders can be done through immunoglobulin substitution or specific immunoglobulin therapies. Therefore, the growing requirement for such treatments leads to increased immunoglobulin production by these processes, thus driving the global market.

- According to the World Health Organization (WHO), in 2022, about 39.0 million people across the globe were living with human immunodeficiency virus infection.

Thus, the growing incidence or prevalence of rare genetic disorders and various immunodeficiency disorders is boosting the demand for plasma-derived medicinal products, thereby propelling the plasma fractionation market growth.

Growing Government Initiatives to Promote the Production of Plasma-Derived Products to Fuel Market Growth

Plasma-Derived Medicinal Products (PDMPs) are prepared industrially with the help of human plasma. These products include albumin, immunoglobulins, and coagulation factors. The World Health Organization (WHO) included several PDMP products in the model list of essential medicines. This initiative highlighted these medications as effective and safe for major needs in a health system, thus increasing their demand. Additionally, governments are taking initiatives to increase the accessibility of plasma-derived products in various regions across the globe.

- For instance, in March 2021, the World Health Organization published guidance to increase the supplies of plasma-derived medicinal products in low-and-middle-income countries through plasma fractionation of domestically collected plasma.

- Additionally, in July 2023, the Medicines and Healthcare Products Regulatory Agency (MHRA) lifted the ban on producing plasma-derived medicinal products containing albumin, which was levied to limit the spread of Creutzfeldt Jakob Disease (CJD).

Moreover, various players are entering the market to cater to the rising demand for plasma-derived medicinal products. In November 2022, Sinovac Biotech, a China-based company, started the production of Plasma-derived Medical products (PDMP) in Bangladesh with an investment of USD 450.8 million.

RESTRAINING FACTORS

Emergence of Recombinant Therapies as an Alternative to Plasma-Derived Medicines Hampers Market Growth

In recent years, many recombinant alternatives have been developed for various plasma-driven therapies. Recombinant products are used prophylactically and are comparatively less immunogenic than plasma-derived products. In addition, various other longer-acting replacement factors are in the development pipeline. These products provide significant benefits, such as less frequent administration, and are more effective in prophylactic use. The growing use of recombinant factors and their increased use in prophylactic therapies is thus a major factor limiting the adoption of plasma products.

The recombinant product version of plasma-derived products is manufactured by the expression of equivalent proteins from genetically engineered cells. It offers a safer option than plasma-derived products as they avoid potential blood-borne transmission of infectious diseases. Therefore, the advantages associated with such products make them more reliable than plasma-derived products, thus restraining market growth. Also, manufacturers are developing and launching recombinant plasma products, limiting the adoption of plasma-based products, thus limiting the market growth.

- For instance, in February 2023, Sanofi received the U.S. FDA approval for ALTUVIIIO Antihemophilic Factor (Recombinant), a factor VIII replacement therapy for patients suffering from hemophilia A.

Plasma Fractionation Market Segmentation Analysis

By Product Analysis

Immunoglobulin Segment Dominated the Market Due to High Product Demand for Immunodeficiency Diseases

Based on product, the market is categorized into albumin, immunoglobulin, coagulation factors, protease inhibitors, and others. The immunoglobulin segment can be sub-segmented into Intravenous Immunoglobulin (IVIG) and Subcutaneous Immunoglobulin (SCIG). The coagulation factors segment can be further sub-segmented into factor IX, factor VIII, prothrombin complex concentrates, fibrinogen concentrates, and others.

The immunoglobulin segment dominated the market in 2023 and is anticipated to continue its dominance in the coming years. The segment's dominance is mainly attributed to the rising demand for IVIG products for various primary and secondary immunodeficiency disorders. Furthermore, the growing prevalence of autoimmune diseases and rising awareness regarding the management of such disorders have led to a surge in the demand for intravenous immunoglobulin (IVIG).

- According to the 2022 report published by the GBS/CIDP Foundation International, a global nonprofit organization supporting patients affected by Guillain-Barre’ syndrome (GBS), Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) and associated conditions, the prevalence of CIDP in the U.S. is about 60,000 individuals.

Moreover, key players continuously investing in the research and development and launching of IVIG products also contribute to the segment growth.

On the other hand, the coagulation factors segment held the second dominant position in 2023. The segment’s dominance was attributed to the growing prevalence of hematological disorders, approval of new products, and growing usage of plasma-based clotting factors for the treatment of bleeding disorders, among others.

- For instance, as per the World Federation of Hemophilia 2022 report, the factor VIII usage per capita was 1.383 IU in the year 2022 as compared to 0.945 IU in 2020.

The protease inhibitor segment is expected to grow at a comparatively higher CAGR than other segments, as protease Inhibitors have wide applications in diagnosing and treating various bacterial, viral, and parasitic diseases. Furthermore, protease inhibitor-based drugs are increasingly used for treating immunological disorders, cancers, and cardiovascular and neurodegenerative disorders. The rising burden of various infectious and chronic disorders is anticipated to increase demand. Additionally, manufacturers are shifting their focus to research and launch new protease inhibitor-based drugs. Thus, these factors are contributing to the growth of the segment.

- For instance, in May 2023, Pfizer Inc. received the U.S. FDA clearance for its drug PAXLOVID, a 3CI protease inhibitor-based oral tablet for treating adults suffering from mild to moderate COVID-19 with a risk for progression to severe infection.

By Application Analysis

Adoption of Plasma Proteins in Immunology & Neurology Procedures to Drive Segment Growth

Based on application, the market is segmented into hematology, critical care, pulmonology, immunology & neurology, and others.

The immunology & neurology segment is projected to grow at a higher growth rate during the forecast period and had a comparatively higher market share in 2023. The increasing burden of immunodeficiency and autoimmune diseases led to strong global demand for these products. The growing prevalence of immunological & neurological diseases led to the extensive use of plasma proteins, such as coagulation factors and immunoglobulins, in various treatment procedures. Combined with this, numerous plasma-based proteins are under development or undergoing clinical trials for neurology and immunology applications, leading to segment growth.

The pulmonology segment is anticipated to grow at a moderate CAGR during the forecast period. The development of the segment can be due to the use of IVIG in various pulmonary diseases. For example, as per an article published in ScienceDirect in 2019, intravenous immunoglobulin treatment has been proven as a salvage therapy for patients with active and progressive Interstitial Lung Disease who do not respond to the combination of steroids and first-line immunosuppressant drugs. Furthermore, companies seek approval for various plasma-derived medicinal products to treat pulmonology disorders.

- For instance, in May 2023, Kamada Pharmaceuticals received the market authorization for Glassia, a plasma-derived Alpha-1 Proteinase Inhibitor from Swissmedic. Alpha-1 antitrypsin (AAT) deficiency is a condition that increases the risk of developing lung diseases.

The hematology segment held a substantial market share in 2023 due to advancements in several hemostasis technologies, leading to its global adoption and growth of the hematology segment. Furthermore, the prevalence of congenital bleeding disorders positively drives market growth. The growing number of trauma cases and accidents across the globe led to the surge in demand for plasma-derived products, such as coagulation factors in the critical care segment, thus driving the growth in the segment’s revenue.

By End-user Analysis

Strong Demand for Plasma Products in Hospitals & Clinics Enable Them to Be in a Leading Position

In terms of end-user, the market is categorized into hospitals & clinics, clinical research laboratories, and others.

The hospitals & clinics segment generated the highest revenue in the global market. The segment's growth is attributed to the increasing number of people opting for plasma-derived therapies across the globe. Various private hospitals with improved infrastructure and technology have adopted plasma-derived therapies and are prescribing their patients suffering from rare immunodeficiency diseases. For example, in June 2023, Grifols, S.A. and the National Service Projects Organization (NSPO) of Egypt announced the availability of the first plasma-derived medicines for administration among Egyptian patients in hospitals.

The clinical research laboratories segment is expected to grow at the highest CAGR during the forecast period. The growth is due to the increasing demand for plasma therapy in rare diseases and growing R&D initiatives to develop more PDMP products for clinical applications.

The others segment constitutes organizations, such as academic institutes and is expected to grow at a significant CAGR over the forecast period. Currently, plasma samples are preferred over serum samples as they contain higher concentrations of blood components and thus are often used in proteomic and metabolic studies. Moreover, plasma retains clotting factors, unlike serum, which makes it an ideal sample for analyzing blood clotting diseases and developing anticoagulant therapies. Thus, the factors mentioned above are augmenting the segment’s growth.

REGIONAL INSIGHTS

The market is analyzed across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

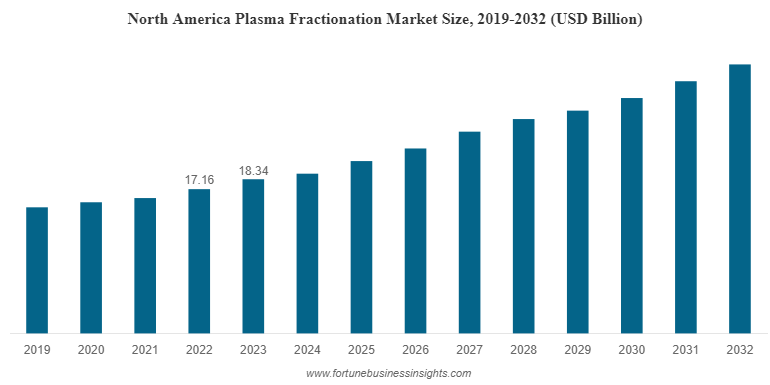

North America stood at USD 18.34 billion in 2023 and is estimated to dominate the global market during the forecast period. The highest plasma fractionation market share of this region is attributed to several factors. Some factors include the presence of major companies developing and launching technologically advanced plasma-derived therapies and products, contributing positively to the region’s growth. Furthermore, key players expanding their geographical presence in the region to cater to the rising demand for plasma-derived medicinal products is also promoting market growth.

- For instance, in January 2022, Grifols S.A. acquired a plasma donation center, Prometic Plasma Resources Inc., located in Canada to increase the availability of plasma-based medicines in the country.

Europe, on the other hand, secured the second position in terms of market share and will continue with its position in the coming years. This is due to the rising prevalence of immunodeficiency and bleeding disorders in the region, and increasing investments in establishing new plasma centers are a few factors augmenting the market growth in the region. For example, according to a 2021 article published by the NCBI, Common Variable Immunodeficiency (CVID) affects approximately 1 in 25,000 individuals, with a higher prevalence in northern Europe.

Increased expenditure on pharmaceutical products and evolving healthcare research infrastructure in India and China led to increasing demand for plasma-derived products, thus driving Asia Pacific plasma fractionation market growth. Furthermore, the growing prevalence of hemophilia in Asian countries is expected to positively affect the market growth in Asia Pacific. For instance, according to a press release published by Grifols in 2020, the per capita consumption of albumin in China is 325 grams per 1,000 population and ranks 8th globally.

Latin America and the Middle East & Africa are estimated to register comparatively slower growth during the forecast period. However, the prevalence of autoimmune diseases in these regions contributes positively to market growth. For example, as per a study published by the National Library of Medicine in 2019, the prevalence of autoimmune diseases in regions of Brazil was 673.6 cases per 100,000 inhabitants, with the highest prevalence for Hashimoto’s thyroiditis at 140.6 cases per 100,000, followed by Vitiligo 132.4 cases per 100,000, and rheumatoid arthritis 105.9 cases per 100,000.

Additionally, increasing plasma collection capacity and rising collaborations among manufacturers are likely to augment market growth in both regions.

- For instance, in July 2023, GC Biopharma Corp. entered into a supply contract agreement with Blau Farmacêutica, a Brazilian pharmaceutical firm, for IVIG-SN 5.0% blood product. The deal is worth USD 90.48 million for five years.

List of Key Companies in Plasma Fractionation Market

Significant Efforts by CSL and Grifols, S.A. to Launch New Products to Strengthen its Global Market Position

Companies, such as CSL and Grifols, S.A. held the majority of the global plasma fractionation market share. High expenditure in research and development, a growing focus on establishing new plasma collection centers, and an increasing emphasis on collaborations and partnerships to strengthen brand presence are a few factors contributing to their high share.

- For instance, in December 2022, CSL established a plasma manufacturing facility in Victoria, Australia. The new facility can process up to 9.2 million plasma equivalent liters per year, increasing the current capacity by ninefold. The company aimed to meet the rising demand for plasma-based products globally through this investment.

Other major players in the global plasma fractionation industry are Baxter, Kedrion S.p.A., and Takeda Pharmaceutical Company Limited, among others. Continuous efforts to launch advanced products and investments in RD are attributable to the increased market presence of these companies in the global market.

- For instance, in April 2023, Takeda Pharmaceutical Company Limited received FDA approval for the expanded use of HYQVIA (immunoglobulin infusion) to treat primary immunodeficiency disorder in children.

LIST OF KEY COMPANIES PROFILED:

- CSL (U.S.)

- Grifols, S.A (Spain)

- Takeda Pharmaceutical Company Limited (Japan)

- Kedrion S.p.A (Italy)

- Octapharma (Switzerland)

- Bio Products Laboratory Ltd. (U.K.)

- Biotest AG (Germany)

- LFB (France)

KEY INDUSTRY DEVELOPMENTS:

- December 2023 – Octapharma AG received extended approval from the U.S. FDA for its plasma-based product, wilate (von Willebrand Factor/Coagulation Factor VIII Complex). The new extended approval label comprises routine prophylaxis aimed to reduce the frequency of bleeding episodes in adults and children aged six years and above.

- November 2023 – Grifols, S.A. received the U.S. FDA approval for its new immunoglobulin (Ig) purification and filling facility in North Carolina. Through this facility, the company was able to manufacture an additional 16 million grams of plasma therapy annually.

- March 2023 – Grifols, S.A. established a manufacturing facility in Marburg, Germany, with an expanded manufacturing capacity for human plasma therapies.

- March 2023 – Takeda Pharmaceutical Company Limited invested USD 764.6 million to build a new plasma-derived therapy production site in Osaka, Japan. The facility will be operational by 2030 and will expand the company’s manufacturing capacity in Japan fivefold.

- January 2022 – Octapharma AG announced that the European Union (EU) expanded the indication for cutaquig, a human immunoglobulin administered subcutaneously. The expansion would provide more flexible treatment options to patients with acquired immune deficiencies.

REPORT COVERAGE

The global market report provides detailed market analysis and focuses on key aspects, such as the overview of the types of plasma fractionation products, regulatory scenario by key countries, reimbursement scenario by key countries, pipeline analysis, number of plasma collection centers for key countries, prevalence of chronic diseases by key countries, pricing analysis of plasma products, regional distribution of plasma fractionation throughput, and distribution of the product (volume) by region. Additionally, it includes an overview of new product launches/approvals, global market forecast, and the impact of COVID-19 on the global market. Besides these, the report offers insights into market trends and highlights key strategies by market players. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market in recent years.

Report Scope & Segmentation

ATTRIBUTE |

DETAILS |

Study Period |

2019-2032 |

Base Year |

2023 |

Estimated Year |

2024 |

Forecast Period |

2024-2032 |

Historical Period |

2019-2022 |

Growth Rate |

CAGR of 7.5% from 2024-2032 |

Unit |

Value (USD Billion) |

Segmentation

|

By Product

|

By Application

|

|

By End-user

|

|

By Region

|

Frequently Asked Questions

How much is the global Plasma Fractionation market worth?

Fortune Business Insights says that the global market size was USD 32.83 billion in 2023 and is projected to reach USD 62.83 billion by 2032.

What was the value of the plasma fractionation market for plasma fractionation in North America in 2023?

In 2023, North America stood at USD 18.34 billion.

At what CAGR is the market projected to grow over the forecast period (2024-2032)?

Registering a CAGR of 7.5%, the market will exhibit steady growth during the forecast period (2024-2032).

Based on product, which is the leading segment in the market?

The immunoglobulin segment is expected to be the leading segment in this market during the forecast period.

What is the key factor driving the market?

Growing incidences of immunodeficiency disorders propel the growth of the market.

Who are the major players in this market?

CSL and Grifols, S.A. are the major players in the global market.

Which region held the highest share of the market?

North America dominated the market share in 2023.

Which factor is expected to drive the adoption of such products?

The introduction of advanced therapies by market players is expected to drive product adoption in the global market.

- Global

- 2023

- 2019-2022

- 182