Over The Counter Drugs Market Size, Share & Industry Analysis, By Product Type (Analgesics, Cold & Cough Remedies, Digestives & Intestinal Remedies, Skin Treatment, Vitamins & Minerals, and Others), By Distribution Channel (Drug Stores & Retail Pharmacies, Hospital Pharmacies, and Online Pharmacies), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

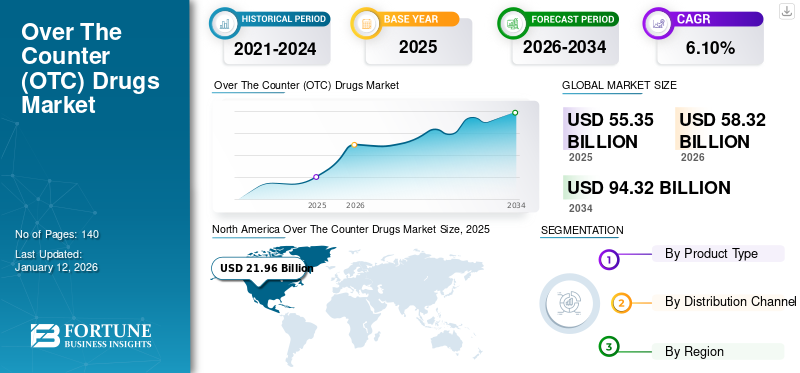

The global over the counter drugs market size was valued at USD 55.35 billion in 2025. The market is projected to grow from USD 58.32 billion in 2026 to USD 94.32 billion by 2034, exhibiting a CAGR of 6.10% during the forecast period. North america dominated the over the counter drugs market with a market share of 39.70% in 2025.

OTC or over the counter drugs are pharmaceutical products that are considered safe to buy without the requirement of a prescription from a medical professional. These products are available in hospital pharmacies, medical stores, and sometimes even grocery shops, and are sold legally without any prescription. OTC medicines are used to treat some common symptoms, which include the common cold, body pain, allergies and flu, heartburn, acne, and other basic health problems.

One of the key factors contributing to the market growth during the forecast period is the increasing use of self-medication. Furthermore, the switch from prescription drugs (Rx) to OTC, citing lower costs, and rising product launches for OTC drugs to boost immunity are driving market growth.

- For instance, in January 2021, Hamdard launched 12 OTC drugs that boosted immunity.

Additionally, the availability and cost-effectiveness of OTC products are driving the growth of the market. For instance, according to the National Center for Biotechnology Information (NCBI) publication, it was reported that in the U.S. every year, over the counter drugs account for approximately USD 100.0 billion in savings. The above-mentioned factors are anticipated to augment market growth for over the counter drugs during the forecast period.

Over The Counter Drugs Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 55.35 billion

- 2026 Market Size: USD 58.32 billion

- 2034 Forecast Market Size: USD 94.32 billion

- CAGR: 6.10% from 2026–2034

Market Share:

- North America dominated the over the counter drugs market with a 39.70% share in 2025, driven by high consumer awareness, a well-established retail pharmacy infrastructure, and strong preference for self-medication. Additionally, cost savings from OTC use and the rapid Rx-to-OTC switch contribute to regional growth.

- By product type, Cold & Cough Remedies held the largest market share in 2024, owing to seasonal variation, rising cases of respiratory infections, and growing pediatric and geriatric populations. Analgesics followed as the second-largest segment due to growing demand for pain relief among elderly populations and increased product launches. Vitamins & Minerals ranked third, fueled by rising health-conscious consumers and growing adoption of preventive self-care.

Key Country Highlights:

- Japan: Growth is fueled by an aging population and the expanding availability of OTC products through drugstores and e-commerce. Regulatory support for Rx-to-OTC switches and self-medication practices further strengthens the market.

- United States: Rising healthcare costs and consumer preference for affordable, non-prescription treatments are major drivers. OTC categories such as analgesics, allergy relief, and vitamins experienced strong growth, with major players like Johnson & Johnson and Perrigo expanding their product lines.

- China: A rapidly growing middle class, increased awareness of self-care, and rising internet penetration are boosting online OTC drug sales. Domestic players like The Himalaya Drug Company and international firms like GlaxoSmithKline are expanding their presence.

- Europe: The region benefits from a strong pharmaceutical manufacturing base, high health literacy, and increasing demand for self-medication. Countries like Germany and the U.K. are investing in expanding private-label OTC lines and improving retail pharmacy reach.

COVID-19 IMPACT

Vitamins & Minerals Segment in the Market Witnessed an Increased Demand amid the COVID-19 Pandemic

The COVID-19 pandemic had caused disruption in the import and export of healthcare products globally. However, some of the key players, such as Johnson & Johnson Services Inc., Reckitt Benckiser Group PLC, and others, reported growth in revenue for their OTC or consumer health segment in 2020.

- For instance, Johnson & Johnson Services Inc., stated in its 2020 annual report, that there was an increase in demand for TYLENOL, one of its OTC analgesic medicines.

The impact of COVID-19 varied for different OTC products. For instance, the pandemic had raised awareness about the importance of self-care and accelerated the growth of categories such as vitamins & minerals or nutritional supplements. At the same time, the growing precautions and hygiene measures resulted in a drop in sales for cough and cold products reported by most manufacturing companies. Also, skin treatment products and digestive & intestinal remedies experienced a decline in sales. Analgesics are pain-relieving products that were in high demand during the pandemic.

The most common OTC drugs during the pandemic were antipyretics, antihistamines, cough suppressants, and vitamins. However, the market witnessed a decline and slow growth in 2020 and 2021 respectively. In 2024, the market for over the counter drugs was poised for steady growth and is projected to grow at a significant CAGR over the forecast period.

Over The Counter Drugs Market Trends

Increasing Shift from Rx to OTC and Growth in Private Label OTC Products are Vital Trends

One of the prominent trends in the market is the shift of manufacturers from prescription drugs to OTC. Many manufacturing companies are switching their products from Rx to OTC. For instance, Bayer AG states in their 2019 annual report that, as part of its strategy, the company will change some of its prescriptive products suitable for self-care to OTC. This is anticipated to lead to a higher availability of these drugs for various disease conditions in emerging and developed countries.

Other trends in the market include the increasing number of private-label OTC products. The rise in online sales of the OTC products and tie-ups between private label manufacturers and e-commerce companies are developing new trends in the market. For instance, In September 2019, Dr. Reddy’s Laboratories Ltd. announced the launch of an OTC Omeprazole Delayed-Release tablet in the U.S. market. These upcoming new trends will diversify market growth during the forecast period.

Download Free sample to learn more about this report.

- North America witnessed a growth from USD 19.68 Billion in 2023 to USD 20.78 Billion in 2024.

Over The Counter Drugs Market Growth Factors

Strong Focus of Key Players in the Development and Launch of New OTC Products to Boost Market Growth

There are a large number of companies operating in this market, which include Johnson & Johnson Services Inc., Bayer AG, Novartis AG, Sanofi S.A., Dr. Reddy’s Laboratories Ltd., Pfizer, and many more. These key industry players are involved in R&D to develop and market new OTC drugs for various health conditions.

- For instance, in September 2020, Dr. Reddy’s Laboratories Ltd. announced the launch of an OTC eye allergy drop, Olopatadine Hydrochloride Ophthalmic Solution.

Such an increase in the number of product launches in the OTC product category will enhance the over the counter drugs market growth.

Accessibility and Affordability of OTC Products to Surge Market Growth

One of the critical factors that are expected to grow the market during the forecast period is accessibility, affordability, and the presence of a large number of retail stores offering OTC products. In developed and emerging countries, the increasing investment by the private sector to improve the supply chain through retail stores and other distribution outlets is leading to market growth. According to the data published by NCBI, in 2020, countries such as the U.S., Japan, Germany, and the U.K. contribute maximally to OTC sales globally.

Additionally, the increasing approvals from regulatory bodies for switching prescription drugs to OTC drugs are fuelling market growth. As the majority of prescription allergy medicines have changed to OTC, there has been a clear shift toward these more convenient and affordable options. For instance, according to the Consumer Healthcare Products Association (CHPA), in 2022, numerous prescription allergy medicines have changed to OTC, and there has been a shift toward these drugs owing to their lower costs.

RESTRAINING FACTORS

Wrong Medications due to Incorrect Self-diagnosis and Side Effects of OTC Drugs May Hinder Market Growth

Some limiting factors that are expected to restrain the global over the counter drugs market growth in the forecast period are incorrect self-diagnosis leading to the consumption of the wrong medicines. Many OTC cough and cold products have led to medication errors and adverse effects on the patient’s body. Additionally, drug abuse and drug addiction practices also pull down the market growth. Cough medicines, diarrhea medicines, and pain relief medicines are some of the common OTC medicines that are used for drug-abuse. According to the Addiction Center and a study published by the Substance Abuse and Mental Health Services Administration (SAMHSA), in 2020, in the U.S., around 1.6 million young people between the ages of 12 and 25 have misused OTC medications (cold and cough medication). Furthermore, the use of traditional medicines also acts as a substitute or alternative for this market.

Over The Counter Drugs Market Segmentation Analysis

By Product Type Analysis

Cold & Cough Remedies Segment to Dominate Due to Increasing Prevalence of Common Colds and Coughs

On the basis of product type, the market can be segmented into analgesics, cold & cough remedies, digestives & intestinal remedies, skin treatment, vitamins & minerals, and others.

The cold & cough remedies segment is anticipated to dominate the market with a share of 23.99% in 2026, owing to the increasing occurrence of common colds and coughs among the population due to seasonal variation. According to the Centers for Disease Control and Prevention, cold and cough are the most common conditions in children below the age of 10 years and in geriatric populations above 65 years, which is leading to an increasing demand for therapeutic products.

Analgesics accounted for the second-largest market share in 2024. This is primarily due to the increasing geriatric population, the surging demand for pain relief drugs, and the launch of new pain-relieving OTC products in the market. For instance, in September 2020, Dr. Reddy’s Laboratories Ltd. announced the launch of OTC Diclofenac Sodium topical gel in the U.S. market.

Followed by analgesics, the vitamins & minerals segment is projected to be the third-largest market. The high demand from sports athletes and working professionals for energy products and weight management supplements is driving segmental growth. According to a survey conducted by the Council for Responsible Nutrition (CRN) in 2019, it was found that vitamins & minerals are the most commonly consumed supplement category, and around 76.0% of Americans consume these products to improve their health.

The digestives & intestinal remedies, skin treatment, and others segments are growing at a steady rate. The rising skin problems, such as acne, sunburn, severe allergic skin reactions, and skin infections due to fungi or bacteria, would surge the segmental growth. The others segment includes sleeping aids, weight loss/Diet, and OTC oral care products.

- The Cold & Cough Remedies segment is expected to hold a 23.9% share in 2024.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel Analysis

Drug Stores & Retail Pharmacies Segment to Dominate Owing to Rising Patient Preference

Based on distribution channel, the market is segmented into drug stores & retail pharmacies, hospital pharmacies, and online pharmacies. The drug stores & retail pharmacies segment is projected to 45.56% market share in 2026, owing to the increasing number of retail pharmacies offering OTC products and the rising patient preference for stores & retail pharmacies for these products. The hospital pharmacies segment accounts for the second-largest market share owing to increasing access to OTC drugs and the availability of different products.

Online pharmacies would grow at a lucrative CAGR owing to the internet penetration in the emerging market and the discounts offered by online pharmacies.

REGIONAL INSIGHTS

On the basis of region, the global market can be segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Over The Counter Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

By region, North America dominated the market with a valuation of USD 21.96 billion in 2025 and USD 23.24 billion in 2026. The dominance of the region is attributed to the increasing preference for OTC products compared to prescription products. The U.S. market is projected to reach USD 21.53 billion by 2026.

Europe is expected to be the second-largest market in the forecast period owing to the high adoption of self-medication and the presence of a large number of OTC drug manufacturing companies in this region. Also, the rising awareness among the population about OTC products is driving market growth in this region. The UK market is projected to reach USD 1.87 billion by 2026, while the Germany market is projected to reach USD 4.41 billion by 2026.

Asia Pacific market is anticipated to be the fastest-growing market, showcasing the highest CAGR during the forecast period due to the shift in consumer attitude toward self-medication, a rise in the geriatric population, the rapid shift from Rx to OTC, and the affordability of OTC medicines. In India, 76.0% of the adult population preferred OTC pharmaceutical products over prescribed medicines. The increasing preference for OTC products is enhancing market growth. Also, the presence of pharmaceutical companies such as Cipla Inc., GlaxoSmithKline plc, The Himalaya Drug Company, Procter & Gamble, and TajPharma, with their strong product portfolios and robust distributional channels are contributing to market over the counter drugs growth.

The Japan market is projected to reach USD 2.95 billion by 2026, the China market is projected to reach USD 4.25 billion by 2026, and the India market is projected to reach USD 2.19 billion by 2026.

Latin America and the Middle East & Africa accounted for a comparatively lower market share in 2024. In Brazil, despite a variety of national regulations, antimicrobials are used without prescription very frequently. The increasing preference for over-the-counter medications citing lower costs and the rising number of players entering these lucrative industries are poised to fuel the market's growth during the forecast period.

KEY INDUSTRY PLAYERS

Diversified Insurance Plans Offered by United HealthCare Services, Inc. and Centene Corporation to Support Their Dominance

The competitive landscape of the global industry has some of the dominant key players, such as Johnson and Johnson, Bayer AG, Novartis AG, Sanofi S.A., Pfizer, GlaxoSmithKline Plc, and Boehringer Ingelheim International GmbH, that account for the majority of the market share. These key players are implementing different strategic initiatives to improve their shares in the market for over the counter drugs.

Johnson and Johnson is one of the largest healthcare companies that operates at a global level. The company offers OTC products under its consumer health segment. As a key strategy, it markets its products to the general public and them on online portals and retail outlets globally. Similarly, Pfizer and GlaxoSmithKline Plc., the leading international pharmaceutical companies, entered into a partnership in August 2019 to develop a joint venture. The aim of this agreement was to create a leading consumer healthcare business and be a market leader in the global market.

Additionally, in April 2020, Takeda Pharmaceutical Company Limited announced that it would continue with the divestiture strategy with the sale of selected products in the European region. Furthermore, in July 2020, Novartis AG launched a not-for-profit portfolio of medicines for the symptomatic treatment of COVID-19. The portfolio includes 15 generic and OTC medicines from the Sandoz division to fulfill the unmet needs of patients with COVID-19 symptoms.

Other prominent players in the global market include Reckitt Benckiser Group PLC, Takeda Pharmaceutical Company Ltd., Amway Corp., Procter & Gamble Co., Herbalife Ltd., Nature’s Bounty Co., and others.

List of Top Over The Counter Drugs Companies:

- Johnson & Johnson Services Inc. (U.S.)

- Bayer AG (Germany)

- Novartis AG (Switzerland)

- Sanofi S.A. (France)

- Pfizer (U.S.)

- GlaxoSmithKline Plc (U.K.)

- Boehringer Ingelheim International GmbH (Germany)

- Reckitt Benckiser Group PLC (U.K.)

- Takeda Pharmaceutical Company Ltd. (Japan)

- Perrigo Company plc (Ireland)

KEY INDUSTRY DEVELOPMENTS:

- June 2023: MCKESSON CORPORATION, a diversified pharmaceutical company announced the launch of Foster & Thrive, a curated private brand of OTC health and wellness products in order to meet evolving patient needs and growing demand.

- July 2022 - RLG Limited, an e-commerce and digital marketing company, teamed up with AFT Pharmaceuticals, a New Zealand-based company, to launch a range of OTC drugs through the online marketplace Tmall Global.

- June 2022 - Glenmark Pharmaceuticals Ltd. acquired a portfolio of approved OTC abbreviated new drug applications (ANDAs) in the U.S. from Wockhardt. The acquired ANDAs helped the company expand its OTC portfolio in the U.S.

- March 2022 - Perrigo Company plc announced that it had received final approval for the over-the-counter use of Nasonex 24HR Allergy from the U.S. FDA. This approval has strenghened the company’s presence in the market.

- December 2020 - Soma Pharmaceuticals and Crown announced their partnership to launch Microcyn technology-based spray and gel and anti-itching over-the-counter products in the U.S. market.

REPORT COVERAGE

The report covers a detailed global over the counter drugs market analysis and overview. It focuses on key aspects such as the competitive landscape, product type, distribution channel, and region. Besides this, it offers insights into market drivers, market trends, market dynamics, COVID-19 impact on the market, and other key insights. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.10% from 2026-2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Product Type

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global over the counter drugs market size was valued at USD 55.35 billion in 2025 and is projected to grow to USD 94.32 billion by 2034.

In 2025, the North America market stood at USD 21.96 billion.

The over the counter drugs market is projected to grow at a compound annual growth rate (CAGR) of 6.0% from 2025 to 2032. This steady growth is fueled by rising demand for self-medication, affordability of OTC products, and increasing regulatory approvals for switching prescription drugs to OTC status.

The cold & cough remedies segment is set to lead the market by product type.

The increasing shift from prescription (Rx) to OTC, the surging launch of new OTC products, and rising preference for these products due to their affordability are some of the major factors driving the markets growth.

Johnson & Johnson Services Inc., Bayer AG, Novartis AG, and Sanofi S.A are the major players in the global market.

North America dominates the global over the counter drugs market, accounting for a 39.64% share in 2024. This leadership is due to high consumer preference for OTC products, widespread retail infrastructure, and strong presence of major pharmaceutical brands.

Cold & cough remedies are the most in-demand OTC products, followed by analgesics and vitamins & minerals. High seasonal illness prevalence and growing awareness of nutritional supplementation are key contributors to their dominance.

- 2021-2034

- 2025

- 2021-2024

- 140

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us