Digital Payment Market Size, Share & Industry Analysis, By Payment Type (Mobile Payment, Online Banking, Point of Sale, Digital Wallet), By Industry (Media & Entertainment, Retail, BFSI, Automotive, Medical & Healthcare, Transportation, Consumer Electronics, Others), and Regional Forecast Report, 2026-2034

Digital Payment Market Size & Industry Analysis

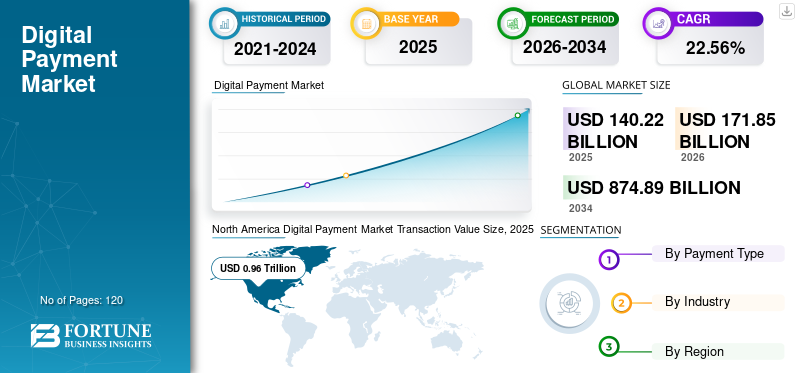

The global digital payment market size was valued at USD 140.22 billion in 2025. The market is projected to grow from USD 171.85 billion in 2026 to USD 874.89 billion by 2034, exhibiting a CAGR of 22.56% during the forecast period. North America dominated the digital payment market, accounting for a 27.2% market share in 2025.

The digital payment market represents a central pillar of the global financial infrastructure, spanning consumer, enterprise, and government transactions. At present, the market reflects broad-based adoption across developed and developing regions, supported by deep integration into retail, banking, transportation, and digital services ecosystems. North America and Europe exhibit high penetration across card-based, wallet-driven, and account-to-account payment models, while Asia-Pacific demonstrates accelerated adoption driven by mobile-first platforms and platform-based commerce.

Historically, the market evolved from card-centric electronic payments toward multi-rail digital ecosystems. Early growth was driven by online banking and point-of-sale digitization. Over time, mobile payments, digital wallets, and real-time transfers shifted the market into a scaling phase, marked by rapid user acquisition and infrastructure expansion. In several regions, the market now approaches structural saturation in basic use cases, while still expanding through value-added services.

Mid-term growth is shaped by deeper penetration into underbanked segments and industry-specific workflows. Long-term momentum depends on interoperability, cross-border efficiency, and embedded finance integration. Inflection points increasingly align with regulatory harmonization, platform convergence, and trust-driven adoption dynamics.

Digital payment refers to the transfer of funds through electronic media such as mobile phones, tablets, laptops, and other devices. This technology has been continuously advancing throughout the past few years. Many new payment options have been added to the digital payment system, starting from online transactions, swiping cards, tapping NFC cards, and scanning codes. This continuous upgradation and various payment options are boosting the adoption of digital payments. Also, the growth of internet connections in every possible place is boosting the demand for digital payment. The penetration of smartphones is also encouraging users to go for digital marketing.

Mobile payment adoption is likely to witness tremendous growth in the market, followed by digital wallets and point of sale. Technologies such as Near Field Communication (NFC) and Quick Response (QR) codes are trending in the market. A digital wallet offers direct transfer from one account to another, which can be prepaid or through a bank account. Point of sale payment is made at the purchasing counter. Recently, many companies have invested in providing NFC through cards, which offer instant transfer of funds from the prepaid account. These various payment options are boosting the digital payment market growth.

Download Free sample to learn more about this report.

Digital payment has enabled businesses to communicate with customers on various channels. For instance, a customer can shift from an omnichannel retail store and purchase & pay through any medium, such as a card or a digital wallet. Thus, providing all the payment gateways to the customer is essential for the retailers. The retailer also offers rewards, loyalty points, and cashback for using gateways during payment. Thus, the customer is present on most of the available channels. All this is creating various opportunities for the providers and the businesses in the digital payment market.

Download Free sample to learn more about this report.

What major trends and transformations are redefining the industry?

The digital payment market is undergoing a structural transformation driven by automation, platform convergence, and evolving consumer expectations. Digital-first operating models are replacing legacy payment infrastructure, enabling faster transaction processing, real-time settlement, and improved system resilience. Automation across fraud detection, reconciliation, and dispute management is reducing operational friction while improving scalability.

Platform and ecosystem consolidation is reshaping competitive dynamics. Payment providers increasingly position themselves as multi-service platforms, integrating payments with lending, analytics, loyalty, and merchant services. Subscription-based pricing and bundled offerings are gaining traction, particularly among SMEs seeking predictable costs and simplified vendor relationships.

Artificial intelligence and data-driven capabilities are redefining risk management and personalization. Advanced analytics enhance fraud prevention, credit assessment, and transaction monitoring without compromising user experience. At the same time, data privacy expectations are influencing platform design, driving investments in secure data architecture and consent-based data usage models.

Customer behavior continues to shift toward seamless, invisible payments. Demand for frictionless checkout, embedded payments, and omnichannel consistency is rising across industries. Consumers increasingly expect speed, transparency, and control, pushing providers to prioritize user-centric design and continuous service innovation within the digital payment market.

What are the strongest growth drivers shaping this market today?

“Growing E-Commerce and Technology-led Initiatives to Augment Market Growth”

The emergence of e-commerce and technology-led initiatives is a key factor that is fueling the digital payment market trends. In recent years, Samsung Pay, Google, Alipay, and Apple have emerged as the top players in the digital payment market. These players have made massive investments in advanced technologies and have expanded their businesses into digital payment services. For instance, Alibaba, a China-based e-commerce company, created Alipay to facilitate payment services between sellers and customers to enhance their operations and improve customer engagement.

Moreover, the adoption of Distributed Ledger Technology (DLT) offers several benefits, such as scalable and decentralized business continuity. For instance, Civic, a provider of the e-KYC platform, offers a secure digital identity at reduced cost. Similarly, cloud technology has also driven the research and development in digital payment offerings. For instance, Paygilant is a cloud-based service that identifies fraud at the time of payment using an innovative mobile-based payment application. All these advancements in technology are likely to drive the digital payment market growth.

The digital payment market is shaped by a combination of structural demand shifts, enabling supply-side capabilities, and external catalysts that reinforce long-term adoption. On the demand side, consumer expectations have shifted decisively toward speed, convenience, and frictionless transactions. Digital-native consumers increasingly prefer mobile payments, digital wallets, and contactless solutions across daily use cases. Businesses are responding by embedding digital payment functionality into e-commerce platforms, subscription models, and service delivery workflows.

From a supply-side perspective, advances in payment infrastructure have lowered entry barriers and improved scalability. Cloud-native payment platforms, application programming interfaces, and modular payment gateways allow providers to deploy services rapidly across geographies. Improved data analytics and fraud detection capabilities have strengthened transaction security, reinforcing trust among merchants and end users. Access to venture capital and strategic investment continues to support innovation across payment orchestration, settlement optimization, and embedded finance models.

“Increasing Adoption of Digital Payment Among Generation Z to Contribute to the Growth of the Market”

Consumers are rapidly adopting non-cash payment methods, which offer a simpler and convenient way to transfer money across bank accounts. With this, lower-cost terminals and asset-lite modes such as QR codes are expected to see prominent growth in the coming years.

This rising digital payment trend is mainly due to the rapid adoption of digital payment services by millennials. Generation Z is naturally more inclined towards the adoption of digitized services. Online banking is the most frequently used banking channel among youth. There is a growing demand from Generation Z for more personalized, flexible, and highly relevant consumer experiences. Additionally, growing demand for enhanced user experience is also a key factor driving business growth. As payment services evolve, providing a better customer experience becomes more competitive. With these services, providers are able to connect with their customers. This is one of the growing trends in the digital payment industry.

Several market players offer rewards on digital payment transactions, which happens to be a recent market trend. Banks and retailers are making significant investments in offering reward points to digital payment users. For instance, Amazon offers a fair discount on the total purchasing amount if the money is paid through net banking or a specific credit card. The trend is likely to create intense competition and significant market opportunities for the digital payment market players.

External catalysts further accelerate digital payment market growth. Regulatory initiatives promoting cashless economies and financial inclusion have expanded access to digital payment systems, particularly in emerging markets. Open banking frameworks and real-time payment mandates encourage interoperability and competition. At the same time, macroeconomic volatility and shifts toward digital commerce increase reliance on resilient, auditable payment channels. Innovation waves tied to mobile connectivity, platform economies, and digital identity systems continue to reshape transaction behavior.

Collectively, these drivers reinforce sustained digital payment market growth by aligning consumer demand with scalable infrastructure and supportive policy environments. The result is a market that continues to expand in scope, complexity, and strategic importance across global financial ecosystems.

What are the key constraints and structural challenges?

Despite strong digital payment market growth, the industry faces several structural constraints that influence scalability and long-term profitability. Barriers to entry remain high for new participants due to licensing requirements, capital intensity, and the need for secure transaction infrastructure. Achieving scale requires extensive integration with banks, merchants, and regulatory bodies, which can slow market entry and expansion timelines.

Regulatory and compliance complexity represents a persistent challenge. Digital payment providers must navigate fragmented regulatory frameworks across regions, including data protection, anti-money laundering, and know-your-customer obligations. Regulatory changes can alter operating models quickly, increasing compliance costs and operational uncertainty. Cross-border payment services face additional scrutiny, limiting seamless international expansion.

Technology and operational risks also affect market stability. Cybersecurity threats, fraud sophistication, and system outages pose reputational and financial risks. Maintaining secure, always-on platforms demands continuous investment in infrastructure, talent, and risk management capabilities. Talent shortages in cybersecurity, data engineering, and regulatory compliance further strain operational resilience.

Market saturation and margin pressure are emerging concerns in developed regions. Intense competition among payment service providers compresses transaction fees and increases customer acquisition costs. As differentiation narrows, providers must balance innovation spending against profitability, creating pressure on long-term return profiles within the digital payment market.

SEGMENTATION

The digital payment market is segmented across payment types and end-use industries, reflecting varied adoption drivers, monetization models, and value creation pathways. Each segment exhibits distinct growth dynamics shaped by consumer behavior, infrastructure readiness, regulatory alignment, and competitive intensity.

By Payment Type Analysis

“Mobile Payment and Digital Wallet Segments to Generate the Maximum Revenue during the Forecast Period”

The payment type segment is categorized into mobile payment, online banking, point of sale (POS), and digital wallet.

Among these segments, the mobile payment segment is further categorized into proximity payment and remote payment, while the point of sale (POS) segment is sub-segmented into debit card at POS, credit card at POS, and near field communication through the card at POS.

Mobile payment solutions represent one of the most dynamic segments within the digital payment market. Adoption is driven by smartphone penetration, app-based ecosystems, and the convenience of device-centric transactions. Value creation is strongest where mobile payments integrate identity, loyalty, and contextual services. Providers benefit from high transaction frequency and data-driven monetization opportunities, although margins remain sensitive to customer acquisition costs and platform fees.

Mobile payment is the transaction of money through mobile devices using application-based payment solutions. Mobile payment technology adoption is increasing mainly due to the proliferating smartphone adoption and the rising purchasing power of users. The penetration of internet facilities, along with high-speed mobile networks, is shifting users to adopt mobile payment solutions. With technological advancements, advanced mobile payment services are offered in the payment market. In mobile payment technology, proximity payment is expected to gain the highest growth during the forecasted period.

Similarly, QR code is mostly used for peer-to-peer transactions in which the money is transferred directly to the bank account of the service provider. There is a significant adoption of QR codes in the retail sector. The other type of proximity payment is Near Field Communication (NFC) payment. In this payment process, the user can pay through card swipe, tapping, or waving the card.

To know how our report can help streamline your business, Speak to Analyst

A digital wallet enables the user to perform online transactions by using electronic devices. Digital wallets can be accessed through mobile phones, laptops, tablets, and computers. In digital wallets, users can store debit or credit card details and directly pay through them. For example, Samsung Pay, Google Pay, and Apple Pay enable the user to pay through their card linked to their wallets. In addition, peer-to-peer transactions can also be done using digital wallets. For instance, Samsung offers cash back or rewards to the user for purchasing Samsung products via their digital wallet.

Digital wallets are emerging as high-value aggregation platforms within the digital payment market. These solutions consolidate payment instruments, identities, and rewards into unified interfaces. Value creation is driven by ecosystem lock-in, cross-selling, and data monetization. Competitive differentiation increasingly depends on interoperability, security architecture, and partnerships rather than standalone payment functionality.

In the digital payment market report, the online banking segment covers payment through digital platforms, along with banks such as internet banking, National Electronic Funds Transfer (NEFT), and Real-Time Gross Settlement (RTGS), among others, for transferring funds. The point-of-sale payment type offers money transfer during in-store purchases. In this, credit or debit cards can be swiped at the purchasing counter. The NFC card is now available in the market, which can be tapped, waved, or swiped at the desk for payment. The NFC at POS is expected to gain maximum traction in the POS payment type market.

Online banking-based payments form the structural backbone of digital financial ecosystems. This segment emphasizes account-to-account transfers, bill payments, and digital fund management. Value creation centers on trust, security, and regulatory compliance rather than rapid innovation. While growth is steadier compared to mobile-first solutions, online banking maintains strategic importance due to its role in large-value transactions and institutional use cases.

Digital point-of-sale payments continue to expand as physical commerce integrates with digital infrastructure. This segment benefits from contactless technologies, terminal upgrades, and software-enabled checkout systems. Value is increasingly created through integrated merchant services such as inventory analytics, customer insights, and financing options. Profitability varies by geography and merchant scale, with higher margins achieved through value-added services rather than transaction fees alone.

By Industry Analysis

“Industries Such as BFSI and Retail to Exhibit a Significant CAGR during the Forecast Period”

The industries covered in digital payment are media & entertainment, retail, BFSI, automotive, medical & healthcare, transportation, consumer electronics, and others (education, IT & telecom, etc.).

Retail remains one of the largest contributors to the digital payment market share. Omnichannel retail strategies demand consistent payment experiences across physical and digital touchpoints. Value creation is driven by checkout optimization, loyalty integration, and data analytics. Margins depend on transaction volume and the ability to upsell ancillary services such as marketing tools or embedded financing.

The digitalization of payments is creating a vast scope in the retail industry. The retail sector is the early adopter of digital payment. In the early stages of digital payment, the payment through debit and credit cards was mostly used in retail. At present, the retailers have upgraded their payment devices with advancements in the payment industry. With the rising adoption of mobile payments and digital wallets, retailers also offer a payment option at the request of customers. Moreover, vendors are offering NFC-compatible payment devices, QR code scanners, and cards at POS systems.

Moreover, the expenditure on upgrading the payment devices and system is not very high. The new payment types, such as proximity payment and payment at POS, are compatible with the earlier versions of card swipe machines. This high adoption of various digital payment technologies is mainly for creating customer relationships during the payment process. Providing a good customer experience is one of the major objectives of retailers. Offering a personalized payment system used by the customer will not only create a positive impact on the transaction, but it will also make the payment process easy and fast. Vendors can analyze the geographical data and buying patterns of the customer through digital payments. This data can be used to provide a better customer experience.

The banking, financial services, and insurance sector leverages digital payments as a core operational capability rather than a standalone product. Value is generated through efficiency gains, customer retention, and ecosystem expansion. This segment prioritizes compliance, scalability, and system resilience, resulting in longer sales cycles but higher contract stability.

Digital payments in BFSI started with the emergence of online banking tools such as NEFT or RTGS. Traditional users find online banking more secure than any other, mostly due to familiarity with the process. With online banking payment, the user can transfer funds, pay fees or bills, manage accounts, or even apply for savings options, investment plans, and insurance policies. For mobile payment types, banks are offering a partnership with other banks for direct transactions through bank accounts. With this facility, users are able to complete the transaction in less time. This has led to the significant adoption of online payments for purchasing, online shopping, or in-store, and paying bills, among others, according to the digital payment market analysis.

The media and entertainment sector exhibits strong alignment with digital payment adoption due to subscription models, microtransactions, and global audience reach. Payment platforms create value by enabling recurring billing, cross-border transactions, and frictionless user experiences. Revenue stability is high, though churn management and fraud risks require continuous optimization.

In media and entertainment, providers are opting for various payment channels to reach users. The media and entertainment industry offers digital payment technologies such as credit cards, debit cards, digital wallets, and mobile payments, among others. For instance, users can apply for and do top-ups of their subscription to the video-on-demand content through different digital wallets. For purchasing music, different music apps have collaborated with several payment channels to improve user engagement. This offers instant ease of process to the user and thus boosts the digital payment market demand. The other industry adopting digital payment technologies is the gaming industry. With the availability of various online games, users can directly purchase the online game on a mobile, laptop, or tablet.

REGIONAL ANALYSIS

Asia-Pacific

Asia-Pacific exhibits the strongest structural momentum within the digital payment market, driven by mobile-first consumer behavior and rapid platform scaling. Several markets bypassed traditional card infrastructure, accelerating the adoption of mobile payments and super-app ecosystems. Competitive dynamics favor vertically integrated platforms combining payments with commerce, social, and financial services. Regulatory environments vary widely, influencing cross-border scalability. Growth is supported by urbanization, digital inclusion initiatives, and rising transaction density.

Asia-Pacific is anticipated to lead the digital payment market, with India and Japan set to gain more traction during the forecast period. In APAC, the adoption of mobile payments and digital wallets is likely to be higher compared to other regions. India and China, being high-population countries, have high smartphone penetration, which creates lucrative opportunities for the digital payment market.

Japan

Japan’s digital payment market balances advanced technology capabilities with entrenched cash usage patterns. Adoption has accelerated through government-led digitization initiatives and increased acceptance of mobile wallets. Value creation focuses on interoperability, merchant enablement, and integration with transportation and retail ecosystems. Consumer trust and reliability remain critical differentiators, leading to conservative innovation cycles but stable long-term demand.

China

China represents a structurally distinct digital payment environment dominated by platform-centric ecosystems. Payments function as embedded utilities within broader digital services, including commerce, messaging, and financial management. Value creation is driven by data integration, ecosystem lock-in, and scale efficiencies. Regulatory oversight strongly shapes platform behavior, influencing innovation pathways and cross-border expansion strategies. Competitive barriers are high due to entrenched network effects.

India and Emerging Asia

In emerging Asian markets, digital payment market growth is fueled by financial inclusion, government-backed payment infrastructure, and smartphone adoption. Real-time payment systems and low-cost transaction models underpin widespread usage. Value creation emphasizes scale, cost efficiency, and ecosystem partnerships. Margins are thinner, but volume potential remains substantial. Regulatory clarity and infrastructure investment continue to shape market evolution.

India has shifted towards mobile payment and digital wallet after demonetization in 2016. Indian government initiatives such as Digital India are expected to further boost the digital payment market revenue in the coming years. Revenue generated through the e-commerce giant, Alibaba Ltd., is expected to create more than 50% of the online transactions in China.

North America Digital Payment Market Transaction Value Size, 2025 (USD Trillion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America represents a structurally advanced digital payment market with high penetration across consumer and enterprise use cases. Card-based digital payments, digital wallets, and real-time payment rails coexist within a mature financial ecosystem. Growth is driven less by first-time adoption and more by replacement cycles, feature enhancement, and embedded finance integration. Competitive intensity is high, with strong incumbent platforms and well-capitalized challengers. Regulatory oversight emphasizes consumer protection, data security, and interoperability, shaping product design and compliance costs.

North America is expected to witness the second-highest market share in the global digital payment market. The preferred payment mode in this region is cash or debit/credit cards. The region consists of some of the best financial institutions in the world. The user also prefers online banking owing to its security and policy. With different strategies being applied by the digital payment providers, the growth of digital wallets is likely to increase in the forecast period.

Europe

Europe’s digital payment market reflects regulatory harmonization alongside fragmented consumer preferences. Account-to-account payments and open banking frameworks play a central role in regional differentiation. Adoption is supported by policy-driven standardization and strong cross-border commerce requirements. However, varied national regulations and legacy banking structures influence deployment speed. Value creation increasingly concentrates around compliance-enabled platforms, identity-linked payments, and infrastructure providers rather than consumer-facing wallets alone.

Europe has a mature mobile and banking industry. In Europe, the majority of the population has bank accounts and, therefore, digital wallets are likely to have maximum growth till 2026. As various companies, such as Telefonica and Vodafone, are investing in NFC services through mobile and cards, primarily in the UK and Germany, the technology is expected to expand the market size in the region.

Latin America

Latin America is an emerging market for digital payment technologies. Brazil and Mexico are likely to account for substantial e-commerce sales through mobile, according to MasterCard. Companies and governments are making substantial investments in these technologies.

Latin America's digital payment market demonstrates strong adoption momentum driven by underbanked populations and mobile connectivity. Alternative payment methods, digital wallets, and instant payment systems play a central role. Value creation is linked to replacing cash-based transactions and enabling small merchant participation. Regulatory fragmentation and macroeconomic volatility introduce operational complexity, but demand fundamentals remain resilient.

Middle East & Africa

The Middle East & Africa region presents uneven but strategically important digital payment market dynamics. Gulf economies emphasize innovation, smart infrastructure, and cross-border payment capabilities. In contrast, parts of Africa focus on mobile money systems addressing financial access gaps. Value creation differs significantly by subregion, ranging from high-end enterprise solutions to mass-market transaction platforms. Infrastructure readiness and regulatory coordination remain key constraints.

The Middle East and Africa region is expected to exhibit steady growth in the global digital payment market. Internet and mobile penetration are increasing in the region. Visa and MFS Africa Ltd., a Pan-African fintech company, have collaborated with an aim to interconnect the evolving mobile money ecosystem in Africa and the online digital payments across the world.

Across regions, high-growth markets share common characteristics: mobile-first adoption, supportive regulatory frameworks, and scalable payment infrastructure. Slower-moving regions tend to exhibit legacy system dependence, complex compliance environments, or consumer trust barriers. Competitive intensity also varies, with some regions favoring platform consolidation while others support fragmented ecosystems.

Overall, geographic differentiation within the digital payment market underscores the importance of localized strategies, regulatory fluency, and adaptable operating models. Global scale alone does not guarantee success; sustained value creation depends on aligning technology, compliance, and consumer expectations within each regional context.

How competitive is the market?

“Market Players to Focus on Providing Mobile Payment Apps to Strengthen Market Position”

Some of the key players in the mobile payment technology market are MasterCard, Visa, PayPal, Google, Amazon, and Alipay, among others. These companies are contributing significantly to this market by adopting strategies such as collaborations and partnerships to provide digital payment solutions across the regions. Furthermore, the players are highly investing in customizing their products as per the demands of the market, the digital payment market forecast states. These advancements are executed keeping in mind the current payment devices so that the cost is not high for the provider adopting the new technology.

The digital payment market is highly competitive, characterized by a layered structure of global incumbents, regional champions, fintech challengers, and infrastructure-focused specialists. Competitive positioning depends less on transaction processing alone and more on ecosystem depth, regulatory alignment, and the ability to embed payments into broader digital workflows.

At the top tier, established payment networks and large technology-enabled platforms retain strong digital payment market share through scale, brand trust, and deep merchant integration. These players focus on platform stability, fraud prevention, cross-border acceptance, and enterprise-grade reliability. Their advantage lies in network effects and long-standing relationships with banks, merchants, and regulators.

Challengers and fintech-native firms compete by targeting specific pain points such as onboarding speed, developer flexibility, pricing transparency, or vertical specialization. Many emphasize modular architectures, application programming interface–driven integration, and rapid deployment. This segment captures disproportionate digital payment market growth in underserved niches, even without broad geographic coverage.

Competition is also shaped by infrastructure providers operating behind the scenes. These firms supply payment gateways, real-time rails, identity verification, and compliance tooling. While less visible, they influence market dynamics by enabling faster innovation cycles and lowering barriers for new entrants. Their value proposition centers on scalability and interoperability rather than consumer branding.

Mergers, acquisitions, and partnerships remain central competitive tools. Larger players pursue selective acquisitions to expand capabilities in fraud analytics, cross-border settlement, or alternative payment methods. Partnerships between banks, fintech firms, and technology platforms are increasingly common, reflecting the complexity of modern payment ecosystems.

How are innovation and emerging technologies shaping future growth?

Innovation is a primary force shaping the trajectory of digital payment market growth, influencing cost structures, scalability, security, and user experience. Emerging technologies increasingly determine competitive advantage rather than incremental pricing or geographic reach.

Artificial intelligence and advanced data analytics play a central role in fraud detection, risk scoring, and transaction monitoring. Machine-learning models enable real-time anomaly detection, reducing false positives while improving security outcomes. This directly impacts merchant trust and operational efficiency, reinforcing digital payment market share among platforms with superior risk management capabilities.

Automation across payment processing, reconciliation, and compliance lowers unit transaction costs and supports high-volume scalability. Straight-through processing reduces manual intervention, enabling providers to serve SMEs and large enterprises with the same infrastructure. As automation deepens, margins increasingly depend on software intelligence rather than transaction volume alone.

Cloud-native architectures reshape deployment economics and speed to market. Cloud infrastructure allows rapid scaling during demand spikes, supports global redundancy, and lowers upfront capital requirements. This flexibility accelerates experimentation with new payment features, subscription billing models, and embedded finance use cases, supporting sustained digital payment market growth.

Application programming interfaces enable modular ecosystems, allowing payments to integrate seamlessly into e-commerce platforms, enterprise software, and mobile applications. This shifts value creation from standalone payment tools toward embedded payment experiences, altering buyer expectations and procurement behavior.

Emerging technologies such as tokenization, biometric authentication, and distributed ledger–based settlement improve security and transparency without disrupting user experience. These innovations reduce friction in cross-border payments and identity verification, areas historically constrained by complexity.

What are the opportunities for growth?

The digital payment market presents several structurally attractive opportunities driven by uneven adoption, evolving enterprise needs, and adjacent value pools. Growth potential increasingly concentrates where payment functionality intersects with broader financial and digital ecosystems.

Underserved segments remain a core opportunity. Small and medium-sized enterprises in emerging and semi-formal economies continue to face limited access to integrated digital payment solutions. Providers that simplify onboarding, compliance, and reconciliation for SMEs can unlock durable demand while building long-term customer relationships. Sector-specific solutions for healthcare, education, and local government also remain underpenetrated, despite rising digitization mandates.

Geographically, parts of Asia-Pacific, Latin America, the Middle East, and Africa show strong digital payment market growth potential due to expanding mobile connectivity and the formalization of commerce. In these regions, mobile-first payment platforms and agent-based distribution models offer scalable entry points. Regulatory frameworks are still evolving, creating space for early movers that align closely with local authorities.

White-space opportunities increasingly lie beyond basic transaction processing. Embedded payments within software platforms, marketplaces, and industry-specific workflows generate higher margins and lower churn. Value creation shifts toward services such as subscription management, cross-border settlement optimization, and integrated lending or insurance products.

Adjacent markets provide additional expansion paths. Identity verification, fraud prevention, and compliance-as-a-service extend naturally from payment data and infrastructure. Providers that leverage existing transaction intelligence can diversify revenue without proportional increases in customer acquisition costs.

List Of Key Companies Profiled:

- Alipay.com Co Ltd

- Amazon.com Inc.

- American Express Co.

- Facebook Inc.

- Google Inc.

- MasterCard International Inc.

- Microsoft Corporation

- PayPal Holdings Inc.

- Paytm

- Samsung Electronics Co. Ltd.

- Visa Inc.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The report provides detailed information regarding various insights into the market. Some of them are growth drivers, competitive landscape, regional analysis, and challenges. It further offers an analytical depiction of the digital payment market trends and estimations to illustrate the forthcoming investment pockets. The market is quantitatively analyzed from 2026 to 2034 to provide the financial competency of the market. The information gathered in the report has been taken from several primary and secondary sources.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Transaction Value (USD billion) |

|

Segmentation |

By Payment Type

|

|

By Industry

|

|

|

By Region

|

- .

Frequently Asked Questions

Fortune Business Insights says that the market size is projected to reach USD 874.89 million by 2034 in terms of transaction value.

In 2025, the market was valued at a transaction value of USD 140.22 million

Growing at a CAGR of 22.56%, the market will exhibit a remarkable growth in the forecast period (2026-2034)

The mobile payment technology segment is expected to be the leading segment in the payment type market during the forecast period

Availability of various payment options is driving the growth of the digital payment market

MasterCard, Visa Inc., Alipay.com Co. Ltd, Amazon Inc., PayPal Inc., and Google Inc. are some of the top players in the digital payment market

Asia-Pacific is expected to hold the highest market share in the digital payment market

The industries such as retail, BFSI, and media & entertainment are expected to gain traction in the digital payment market in the forecasted period

- 2021-2034

- 2025

- 2021-2024

- 120

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us