Edge AI Market Size, Share & Industry Analysis, By Component (Hardware, Network, Edge Cloud Infrastructure, Software, and Support Services), By Industry (Automotive, Manufacturing, Healthcare, Energy & Utility, Retail & Consumer Goods, IT & Telecom, and Others), and Regional Forecast, 2026 – 2034

(Offer valid till 15th Aug 2026)

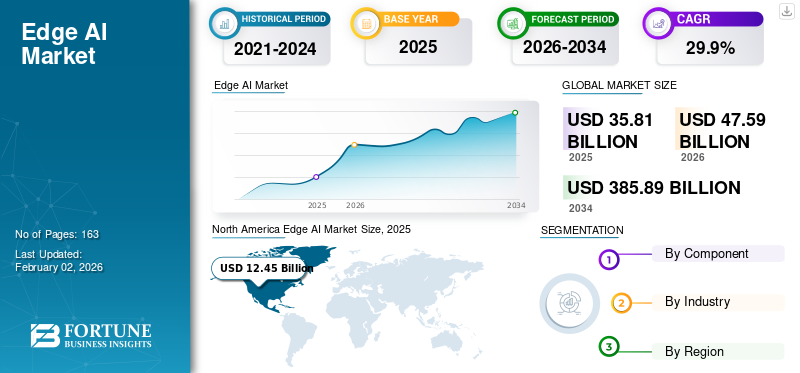

Edge AI Market Size

The global edge AI market size was valued at USD 35.60 billion in 2025. The market is projected to grow from USD 46.96 billion in 2026 to USD 445.75 billion by 2034, exhibiting a CAGR of 32.5% during the forecast period. North America dominated the edge AI market with a market share of 35.11% in 2025.

Edge AI integrates the world of artificial intelligence (AI) with edge computing, enabling AI algorithms to be executed on local devices that have an edge computing capability for important applications. These solutions enable data processing at local devices in real time and do not require internet connectivity. Additionally, the technology helps create local devices that provide fast insight, fast computing power, and much greater data security. The market growth is driven by the rising demand for real time data processing and decision-making at the source, enabling organizations to reduce latency, improve operational efficiency, enhance data privacy, and minimize dependence on centralized cloud infrastructure.

Key players operating in the market comprise NVIDIA Corporation, Intel Corporation, Microsoft Corporation, Alphabet, Inc., and Amazon.com, Inc. These companies are focusing on forming partnerships with semiconductor firms, cloud providers, automotive companies, device manufacturers, and industrial automation players.

Download Free sample to learn more about this report.

EDGE AI MARKET TRENDS

Shift from Passive Surveillance to AI-Powered Video Analytics to Strengthen Product Adoption

The adoption of AI-enabled smart camera systems and real-time video analytic tools are becoming a popular trend in many different applications such as security traffic management, retail environments, industrial inspection processes, and monitoring of smart cities. Unlike traditional video surveillance systems, which simply recorded events and relied on sending data to remote cloud or central server locations for analysis, modern smart cameras equipped with edge AI can process video directly at the location being monitored. They can also provide real-time analysis of what is happening based on the presence of objects, people, vehicles, safety issues, anomalies, license plates, crowd movements and suspicious behavior. For instance,

- In February 2026, Mumbai’s Civic Body announced plans to deploy 1,150 AI-powered CCTV cameras, including 650 new installations and 500 upgraded cameras. The announcement would enable real-time alerts for incidents such as fire, smoke, tree falls, waterlogging, illegal dumping, and encroachments.

Therefore, the increasing product use in smart cameras and video analytics is emerging as a major market trend, as enterprises and public authorities shift from passive video recording toward intelligent, real-time, and automated visual monitoring systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Adoption of IoT and Connected Devices to Drive the Market

Industries are deploying connected sensors, connected cameras, connected machines, connected vehicles, connected gateways, connected smart meters, connected wearables, and connected consumers to gather real-time operational data at an unprecedented rate. There is currently a very rapid increase in the number of endpoints connected through the Internet, creating large amounts of data at the edge of the network, reducing the need for sending this data back to the cloud for processing.

Within smart cities, connected devices such as smart cameras, traffic lights, smart meters, and environmental sensors use AI to provide immediate alerts while also lightening the load on the associated network. In case of wearable devices and smart devices in the healthcare and consumer electronics sectors, these products typically use AI to perform in-device monitoring, personalization, voice recognition and privacy-centric processing. For instance,

- In November, 2025, ASUS IoT unveiled the PE3000N, a rugged edge AI platform powered by NVIDIA Jetson Thor for robotics and automation in harsh environments.

MARKET RESTRAINTS

Power Efficiency Challenges and Thermal Limitations to Restrain Market Growth

The edge AI market growth is restrained by the significant amount of power AI workloads demand, especially when it comes to deploying sophisticated inference models onto smaller edge devices. While the expectation is that most devices will be capable of processing data locally and in real time, a number of use cases (video analytics, autonomous robots, intelligent cameras, medical monitoring equipment, drones, and industrial inspection systems) require real-time data processing and have extremely strict limitations associated with battery life, heat output, and size.

In addition to the power requirements of AI workloads, another reason slowing the growth of the market is the need for executing the engineering work before deploying AI at the edge. This additional engineering typically includes things such as model compression, quantization, workload scheduling, dedicated AI chips, and thermal management. All of this additional engineering increases the overall cost of implementing edge AI and will further delay its commercialization.

MARKET OPPORTUNITIES

Expansion of Edge AI in Autonomous Vehicles, ADAS, and Mobility Systems to Create Significant Growth Opportunities

The implementation of numerous autonomous vehicles and ADAS and the rise of connected mobility platforms are generating major growth opportunities for industry players in the vehicle sector. Today’s vehicles use real-time data from multiple sensors, including cameras, radar, LiDAR, ultrasonic, GPS, and in-cabin systems, to enable safety-critical functions such as automatic emergency brake assist, lane keeping assist, pedestrian detection, collision avoidance, autonomous parking, driver monitoring and vehicle-to-everything communication. For instance,

- In September 2025, Qualcomm and BMW introduced the Snapdragon Ride Pilot automated driving system for the BMW iX3. The system has been validated across 60 countries and is planned to expand availability to more than 100 countries by 2026.

Therefore, the expansion of autonomous vehicles, ADAS, and connected mobility systems is expected to create significant opportunities for industry participants across automotive-grade processors, AI accelerators, embedded computing platforms, sensor fusion software, and real-time operating systems.

Segmentation Analysis

By Component

Rising Deployment of AI-Enabled Edge Devices to Drive Hardware Segment Dominance

Based on component, the market is categorized into hardware, network, edge cloud infrastructure, software, and support services.

The hardware segment is anticipated to account for the largest edge AI market share. This is owing to the massive uptake of AI-powered products including AI PCs, smartphones, smart cameras, edge servers, industrial robots, sensors, gateways and automotive AI processors that create edge AI solutions. There has also been a significant increase in AI chip, NPU, GPU, embedded processing & edge computing device investments in the manufacturing, automotive, healthcare, retail and telecom industries resulting in a further strengthening of the hardware demand and revenues during 2025.

The edge cloud infrastructure segment is anticipated to grow at the highest CAGR of 35.2% over the forecast period. This is owing to enterprises increasingly shifting from standalone devices to distributed compute, storage, orchestration, and cloud-edge management platforms for scaling real-time AI workloads across multiple locations.

By Industry

To know how our report can help streamline your business, Speak to Analyst

Rising Adoption of In-Vehicle Intelligence to Propel Automotive Segment Dominance

Based on industry, the market is classified into automotive, manufacturing, healthcare, energy & utility, retail & consumer goods, IT & telecom, and others.

The automotive segment captured a dominating market share in 2025 and is expected to grow at the highest CAGR of 36.0% over the analysis period. This is owing to the increased use of edge AI applications in in-vehicle communications and driving systems. These include ADAS, autonomous driving, cabin monitoring, sensor fusion, predictive diagnostics, and connected vehicle systems. The demand for low latency, real-time AI processing in automotive vehicles and manufacturing facilities is driving the product demand across this sector, as automotive edge AI provides support in safety, automation, quality control, and operational efficiency.

The retail & consumer goods segment is anticipated to grow at a prominent CAGR of 34.4% during the forecast period. This is owing to the steady product adoption in smart stores, inventory analytics, AI-enabled consumer devices, and loss prevention systems. However, the growth remains comparatively balanced due to already high penetration of smartphones, PCs, and connected retail technologies.

Edge AI Market Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America Edge AI Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest market share in 2024, valuing at USD 9.74 billion, and also maintained the leading share in 2025, with USD 12.50 billion. The market in North America is expected to increase owing to the high rates of adoption of AI-powered endpoint devices, enterprise AI infrastructure, industrial automation, and cloud-edge platforms. Additionally, the presence of some of the world’s largest technology companies and chip manufacturers, hyperscalers, and AI software suppliers will help accelerate product commercialization in hardware, software, and edge cloud infrastructure, fueling market growth. For instance,

- In May 2025, Microsoft introduced Copilot+PCs, a new category of Windows PCs designed for AI workloads. The launch aimed at supporting the growth of on-device AI and local inference capabilities in consumer and enterprise devices.

U.S. Edge AI Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 12.32 billion in 2026, accounting for roughly 26.2% of global sales.

To know how our report can help streamline your business, Speak to Analyst

Europe

The Europe market is projected to reach a valuation of USD 11.55 billion by 2026 and record a growth rate of 30.9% over the forecast period. The regional market is growing as more enterprises increase their use of AI technologies and invest in industrial automation, automotive intelligence, health care digitalization, energy switching, and necessary trusted AI infrastructure. The region is likely to benefit from its high levels of manufacturing, automotive, healthcare, energy, and public sector technology use. For instance,

- In February 2025, the European Commission launched InvestAI, an initiative to mobilize USD 210 billion for AI investment, including a USD 21 billion fund for AI gigafactories.

U.K. Edge AI Market

The U.K. market is estimated to touch around USD 2.02 billion in 2026, representing roughly 4.3% of global revenues.

Germany Edge AI Market

The Germany market is projected to reach approximately USD 2.59 billion in 2026, equivalent to around 5.5% of global sales.

Asia Pacific

The Asia Pacific region is estimated to reach USD 13.24 billion in 2026 and is expected to grow at the highest CAGR of 36.7% during the forecast period. This is owing to its diverse electronics manufacturing base, semiconductor ecosystem, digital device production, automotive electronics, telecom scale, smart factories, AI enabled cameras, and large consumer tech market in the Asia Pacific region. Key countries driving the growth of the regional market include China, Japan, Korea, India, and ASEAN. For instance,

- In March 2024, the Government of India approved the IndiaAI Mission with an outlay of USD 1,250 million, including public AI compute infrastructure of 10,000 or more GPUs, supporting India’s AI ecosystem development.

China Edge AI Market

The China market is projected to be one of the largest worldwide, with 2026 revenues estimated to touch around USD 4.54 billion, representing roughly 9.7% of global sales. This is owing to its strong electronics and semiconductor manufacturing ecosystem, rapid deployment of smart factories and smart city projects, and the increasing adoption of AI-powered cameras, industrial automation, connected vehicles, and edge computing infrastructure across industries.

Japan Edge AI Market

The Japan market is estimated to reach a value of around USD 2.51 billion in 2026, accounting for roughly 5.3% of global revenues.

India Edge AI Market

The India market is estimated to touch a valuation of around USD 1.58 billion in 2026, accounting for roughly 3.4% of global revenues.

South America

The South America market is expected to reach a valuation of USD 2.47 billion in 2026 and witness moderate growth during the forecast period. This is owing to the expansion of telecom infrastructure, digital government, cloud services, IoT, AI, and edge computing adoption. Brazil remains the key regional market due to its large digital economy, retail base, telecom ecosystem, industrial sector, and public-sector digital transformation initiatives.

Middle East and Africa

The Middle East and Africa market is estimated to reach USD 3.63 billion in 2026 and is expected to grow at the second highest CAGR during the analysis period. This is owing to the presence of major demand centers such as the GCC and Israel. The regional market growth is supported by smart cities, oil and gas digitization, telecom edge infrastructure, surveillance, energy asset monitoring, public safety, sovereign AI investment, and national digital transformation programs. In the Middle East & Africa, the GCC is set to reach a value of USD 1.56 billion in 2026. For instance,

- In May 2025, HUMAIN, a Public Investment Fund-backed AI company in Saudi Arabia, announced a strategic partnership with NVIDIA to build AI factories and support the next wave of AI infrastructure development in the Kingdom.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Edge AI Platforms and Distributed Infrastructure by Key Players to Strengthen their Standing

The global edge AI market holds a semi-consolidated market structure, with prominent players such as NVIDIA Corporation, Intel Corporation, Microsoft Corporation, Alphabet, Inc., and Amazon.com, Inc. holding significant positions. These companies are investing in AI processors, edge servers, cloud-edge platforms, AI software frameworks, and distributed computing infrastructure to support real-time data processing, low-latency inferencing, and localized AI decision-making across automotive, manufacturing, healthcare, retail, telecom, and smart city applications.

Other notable players in the global market include Edge Impulse, Synaptics, Viso.ai, ADLINK Technology, and IBM Corporation. These companies are focusing on product innovation, AI-enabled edge devices, industrial automation platforms, strategic partnerships with cloud and telecom providers, and expansion of edge cloud infrastructure capabilities. This is expected to strengthen their competitive positioning and accelerate product adoption over the forecast period.

LIST OF KEY EDGE AI COMPANIES PROFILED

- NVIDIA Corporation (U.S.)

- IBM Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Alphabet, Inc. (U.S.)

- com, Inc. (U.S.)

- Intel Corporation (U.S.)

- Synaptics Incorporated (U.S.)

- ADLINK Technology Inc. (Taiwan)

- Edge Impulse Inc. (U.S.)

- ai (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Microsoft expanded Azure Local and Azure IoT Operations with AI-powered edge computing enhancements for hybrid, distributed, and AI-ready enterprise environments. This supports the edge AI market by helping companies run AI workloads closer to industrial sites, devices, and operational data sources.

- October 2025: Google introduced Coral NPU as a full-stack, open-source platform for edge AI targeting low-power and always-on AI devices. The solution enables local AI inference in wearables, embedded devices, and privacy-focused edge applications.

- October 2025: NVIDIA released IGX Thor for real-time physical AI at the industrial and medical edge. IGX Thor enables AI workloads such as sensor processing, robotics control, medical imaging, industrial automation, and real-time inference to run closer to machines, devices, and operational environments rather than depending fully on cloud processing.

- August 2025: NVIDIA launched Jetson AGX Thor developer kits and production modules, strengthening edge AI adoption in robotics, manufacturing, logistics, healthcare, agriculture, and retail. The platform supports local AI inference and real-time decision-making for autonomous machines and physical AI applications.

- May 2025: IBM and Lumen announced a collaboration to deploy IBM watsonx technology in Lumen’s edge data centers, enabling near-real-time AI inferencing for financial services, healthcare, manufacturing, and retail customers. This supports the market by bringing enterprise AI processing closer to business locations and data sources.

- February 2025: IBM and Qualcomm expanded their collaboration to scale enterprise-grade generative AI from edge to cloud, focusing on privacy, reliability, personalization, lower cost, and energy-efficient AI workloads. This strengthens IBM’s edge AI position by enabling enterprises to run AI workloads across connected edge devices and cloud environments.

- January 2025: AWS announced a new AWS Wavelength Zone in Casablanca in partnership with Orange. The development supports edge AI by allowing developers to build low-latency applications, including AI/ML inference, gaming, and fraud detection near end users.

REPORT COVERAGE

The global edge AI market analysis includes a comprehensive study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers, and acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 32.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Industry, and Region |

| By Component |

|

| By Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 35.60 billion in 2025 and is projected to reach USD 445.75 billion by 2034.

In 2025, the North America market value stood at USD 12.50 billion.

The market is poised to grow at a CAGR of 32.5% during the forecast period of 2026-2034.

By industry, the automotive segment led the market in 2025.

The increasing adoption of IoT and connected devices is a key factor anticipated to drive the market.

NVIDIA Corporation, Intel Corporation, Microsoft Corporation, Alphabet, Inc., and Amazon.com, Inc. are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 135

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us