Automotive Test Equipment Market Size, Share & Industry Analysis, By Location (Production Testing and Service Testing), By Propulsion (ICE and EV), By Vehicle Type (Passenger Cars and Commercial Vehicles), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

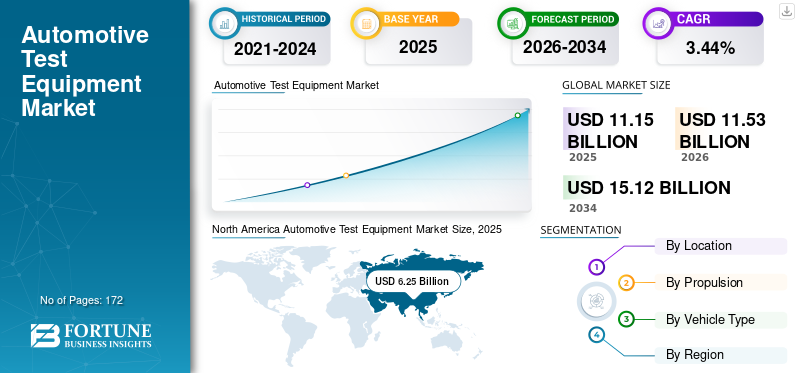

The global automotive test equipment market size was estimated at USD 11.15 billion in 2025 and is projected to reach USD 11.53 billion in 2026 to USD 15.12 billion by 2034, growing at a CAGR of 3.44% from 2026 to 2034. Asia Pacific dominated the automotive test equipment market with a market share of 56.09% in 2025. The industry growth is driven by vehicle electrification expansion, stringent emission regulations, ADAS validation requirements, digital diagnostics integration, and the increasing complexity of automotive electronic systems.

Automotive test equipment assesses the performance of various vehicle components, including engines, transmissions, suspension systems, steering systems, and braking systems. This equipment is used to assess the quality and consistency of components, subassemblies, and finished vehicles. This ensures that vehicles meet strict quality standards before reaching consumers, reducing defects and recalls.

Modern vehicles are equipped with a multitude of electronic components and systems, including Engine Control Units (ECUs), infotainment systems, navigation systems, sensors, and more. These electronic systems require comprehensive testing to ensure that they function correctly and reliably. Test equipment also optimizes vehicle design and performance characteristics. Moreover, safety is a top priority in the automotive industry. Test equipment is used to evaluate the effectiveness of safety systems, including airbags, seat belts, anti-lock brakes, and electronic stability control, to ensure they function correctly in various driving conditions and collision scenarios.

Automotive test equipment market size expansion is closely aligned with the growth of electric vehicles (EVs), hybrid systems, and high-voltage architectures. Traditional mechanical diagnostics are progressively complemented by electronic control unit validation, battery management system calibration, and power electronics testing. This transition is expanding capital expenditure requirements across original equipment manufacturers and independent service networks.

Automotive test equipment market share remains concentrated among global suppliers specializing in emission testing systems, dynamometers, electrical diagnostic platforms, and advanced software-driven calibration tools. However, digitalization and cloud-enabled diagnostics are redefining competitive positioning. Vendors capable of delivering integrated hardware-software ecosystems are strengthening their market presence.

Automotive test equipment market trends include automation of production-line validation, increased use of simulation-based testing, and adoption of artificial intelligence-driven fault detection. Electrified vehicle platforms require high-voltage safety testing, battery cell validation, and inverter performance assessment. These emerging requirements are reshaping product portfolios.

Automotive test equipment market growth is projected to remain stable through 2034. Regulatory emission compliance, rising vehicle production complexity, and growing aftermarket diagnostic sophistication will sustain demand. While cost pressures persist in emerging markets, technological advancement and electrification are reinforcing long-term structural expansion across the automotive test equipment industry globally.

Download Free sample to learn more about this report.

Automotive Test Equipment Market Key Takeaways

- 2025 Market Size: USD 11.15 billion

- 2026 Market Size: USD 11.53 billion

- 2034 Forecast Market Size: USD 15.12 billion

- CAGR: 3.44% from 2026–2034

- Asia Pacific dominated the automotive test equipment market with a 56.09% share in 2025.

- ICE propulsion segment accounted for 89.12% market share in 2022.

- Service testing segment held 8.05% market share in 2022.

North America

North America maintained strong growth due to electrification investments and strict emission standards.

Asia Pacific

Asia Pacific led the market with USD 6.25 billion valuation in 2025.

Europe

Europe witnessed stable expansion driven by EV adoption and carbon reduction regulations.

U.S.

Market growth driven by manufacturing automation, EV expansion, and advanced diagnostics integration.

Japan

Strong market growth supported by hybrid vehicle production and advanced powertrain innovation.

Read More

Market Trends

Rising Demand for More Reliable and Efficient Testing Solutions

Automakers are constantly investing in R&D activities to improve the efficiency and reliability of their testing processes. This is driving the development of new testing equipment technologies that can provide faster, more accurate, and more reliable test results. For instance, there is a growing demand for integrated testing solutions that can combine multiple tests into a single test sequence. In October 2022, AVL opened an indoor laboratory for the validation and verification of sensors for driver assistance systems in Roding, Bavaria. In the 1600 square meter test area, safety-relevant functions can be tested under adverse weather conditions, irrespective of real outdoor conditions, thus ensuring the safety of vehicles in semi-autonomous operation.

Similarly, in March 2023, automotive testing supplier A.B. Dynamics introduced a new, highly maneuverable target platform to test ADAS and A.V. technology. The test system is designed to help replicate challenging urban test scenarios specifically. The LaunchPad Spin simulates dynamic movements, can carry a variety of vulnerable road user targets, and has a top speed of 30km/h (20mph).

Automation of production-line testing is a dominant automotive test equipment market trend. Manufacturers deploy robotic validation systems to enhance quality control and reduce human error. Inline diagnostics improve manufacturing efficiency.

Digital twin simulation tools are gaining prominence. Virtual validation environments allow early detection of design issues. Simulation reduces physical testing cycles and development costs. Cloud-connected diagnostic platforms are expanding. Remote software updates and centralized data analytics improve fault detection accuracy. This supports scalable service network integration.

Artificial intelligence-based predictive maintenance tools are emerging. Data-driven analytics identify potential component failures before occurrence. Electrified vehicle testing requirements are intensifying. High-voltage battery validation, thermal management testing, and inverter calibration demand specialized equipment.

Download Free sample to learn more about this report.

Market Drivers

Increasing Demand for Electric Vehicles (EVs) and Autonomous Vehicles (AVs) is Expected to Increase the Demand for the Market Significantly

Testing of the equipment is crucial for evaluating the performance of electric and hybrid vehicles, including battery systems, electric motors, charging infrastructure, and powertrain integration. Electric vehicles rely on batteries for power. Testing of automotive equipment is essential for evaluating the performance, capacity, and safety of batteries. This includes tests for battery range, charging efficiency, thermal management, and durability.

The rapid increase in battery technology for electric vehicles requires constant evolution of the equipment needed to test them. Original Equipment Manufacturers (OEMs) are launching turnkey solutions to test powerful batteries. For instance, in September 2023, E.A. Elektro launched a compact automated battery cycler and test system to enhance the testing of higher-power EV batteries. The test system can control an environmental chamber and communicate with a battery management system through the CAN bus interface, and drag-and-drop software is all included.

Vehicle electrification represents the primary driver of the automotive test equipment market. Battery electric vehicles and hybrid platforms introduce high-voltage systems requiring specialized validation tools. Testing battery packs, inverters, and electric drivetrains demands advanced diagnostic infrastructure.

Stringent emission regulations further support market growth. Governments enforce compliance through standardized testing protocols for internal combustion engine vehicles. Production testing and certification processes increase demand for advanced emission analyzers and dynamometers. Growing electronic complexity within vehicles accelerates testing requirements. Modern vehicles integrate numerous electronic control units that require validation and calibration. Advanced driver assistance systems require sensor alignment and software verification.

Aftermarket service network expansion also contributes. Independent service centers increasingly require sophisticated diagnostic tools capable of interfacing with proprietary vehicle software architectures. Digital transformation within manufacturing supports automated production testing. Inline quality assurance systems reduce defect rates and improve compliance efficiency.

Market Restraints

High Cost of Automotive Test Equipment to Restrain the Market Growth

The testing of automotive equipment can be very expensive, which can be a barrier to entry for small and medium-sized businesses. This is a very complex process. It needs to be tested on a wide range of components and systems in a variety of conditions. This complexity requires the use of advanced technologies and materials, which drives up the cost of the equipment.

Moreover, it also needs to be able to measure and record data with a high degree of accuracy. This precision requires the use of high-quality components and assembly techniques, which also drives up the overall production cost of automotive test equipment. All these factors are hampering the automotive test equipment market growth.

High capital investment represents a key restraint within the automotive test equipment market. Advanced testing systems require significant upfront expenditure, limiting adoption among smaller service providers. Rapid technological evolution creates obsolescence risk. Diagnostic platforms must continuously update software compatibility to match evolving vehicle architectures. Continuous upgrades increase lifecycle costs.

Standardization challenges also affect market stability. Different regulatory frameworks across regions complicate product development and certification alignment. Cost sensitivity in emerging markets restricts the penetration of high-end diagnostic tools. Independent workshops may rely on lower-cost alternatives with limited functionality. Complex integration requirements further constrain deployment. High-voltage testing environments require safety compliance and trained technicians. Workforce skill gaps can limit effective implementation. Supply chain volatility impacts electronic component availability. Semiconductor shortages may delay equipment production and increase pricing pressure.

Market Opportunities

Expansion of electric vehicle production offers a substantial opportunity within the automotive test equipment market. Dedicated EV production lines require specialized high-voltage validation and battery testing infrastructure. Growing adoption of advanced driver assistance systems presents an incremental opportunity. Sensor calibration equipment and radar alignment tools are in high demand.

Emerging markets' modernizing emission compliance frameworks provide growth potential. As regulatory enforcement strengthens, advanced emission testing systems gain traction. Aftermarket digitalization represents additional expansion potential. Subscription-based diagnostic software platforms can generate recurring revenue streams.

Autonomous vehicle development requires simulation and validation environments. Test equipment supporting artificial intelligence and sensor fusion evaluation will experience rising demand. Commercial vehicle fleet electrification strengthens the opportunity. Fleet operators require large-scale maintenance diagnostics and powertrain validation tools.

SEGMENTATION ANALYSIS

By Location Analysis

Production Testing To Hold the Largest Market Size Due to Its Wide Usage Among Automotive Component Manufacturers

On the basis of location, the market is bifurcated into production testing and service testing.

Production Testing

The production testing segment is the largest shareholder in the global market and is expected to maintain its dominance over the forecast period. Production testing is the testing of vehicles and components during the manufacturing process to ensure that they comply with regulations and quality standards. Automotive OEM facilities, research & development centers, and automotive component manufacturers carry out the testing. Production testing represents the largest revenue contributor within the automotive test equipment market. It includes end-of-line testing, component validation, emission verification, and electronic system calibration conducted during vehicle manufacturing.

Electrification significantly increases production testing complexity. Battery electric vehicles require high-voltage insulation testing, battery pack validation, inverter performance verification, and thermal management assessment. Each electric drivetrain component must undergo rigorous validation before vehicle release. This has expanded capital expenditure in advanced diagnostic benches and automated test cells.

Advanced driver assistance systems (ADAS) integration further drives production testing demand. Radar, camera, and LiDAR calibration systems are increasingly embedded within assembly lines. Automated optical alignment tools ensure sensor precision and regulatory compliance.

To avoid any issues with product malfunction or customer dissatisfaction, production testing has become crucial. In larger applications, product defects have the potential to cause serious injury. To protect users, it is important to minimize the risk of defects by thoroughly testing products before they are sold. The increasing complexity of vehicles with more electronics and components has led to a growing demand for production testing equipment.

Service Testing

Growing concerns of consumers to ensure the safety and reliability of their vehicles is one of the major reasons driving the service testing segmental growth. OEMS, such as PHINIA, provide aftermarket test equipment services such as fuel management & care, chassis, ignition, and power electronics for EV and HEV drivetrains, among others, to its customers.

Moreover, service testing held a market share of 8.05% in 2022 and is estimated to register a CAGR of 2.8% over the forecast period. Automotive garages or repair & maintenance centers offer service testing at a very low price compared to production testing.

Service testing encompasses diagnostic and maintenance validation conducted within dealerships, independent workshops, and fleet maintenance facilities. It represents a structurally expanding segment within the automotive test equipment market. Increasing vehicle electronic complexity has elevated diagnostic sophistication requirements. Modern vehicles integrate dozens of electronic control units, requiring advanced scan tools capable of real-time communication with proprietary systems.

Electric vehicles introduce new service testing needs. High-voltage safety testing equipment, battery health diagnostics, and inverter troubleshooting systems are increasingly deployed within authorized service networks. Connected vehicle architectures enable remote diagnostics and over-the-air updates. Cloud-integrated platforms allow service providers to access centralized databases for fault detection and software calibration.

Independent workshops are progressively upgrading diagnostic platforms to remain competitive. However, cost sensitivity influences purchasing behavior. Subscription-based software licensing models are becoming common, allowing incremental investment rather than large capital outlay. Fleet operators also contribute to service testing demand. Commercial vehicle operators require preventive maintenance diagnostics to reduce downtime and operational risk.

By Propulsion Analysis

EV is anticipated to Register the Highest Growth Rate due to its Growing Popularity.

The market is categorized into ICE and EV based on propulsion.

Internal Combustion Engine (ICE)

ICE segment occupied a lion’s share of 89.12% in 2022. The ICE propulsion segment is anticipated to witness slow growth over the forecast period owing to the strict environmental regulations to curb emission levels and government initiatives to phase out ICE-powered vehicles in the coming years. However, growing demand for hybrid and high-performance vehicles is driving the demand for ICE vehicle testing equipment. Sports cars and luxury cars are equipped with powerful engines. These engines require specialized testing equipment to ensure they perform efficiently and smoothly.

Internal combustion engine vehicles continue to represent a significant portion of the automotive test equipment market. Despite electrification trends, global ICE vehicle production remains substantial. Emission testing systems form a core demand driver. Governments mandate periodic emission validation to ensure compliance with environmental standards. Engine dynamometers, exhaust analyzers, and fuel efficiency testing systems remain essential tools.

Fuel injection calibration, transmission diagnostics, and combustion performance analysis also sustain ICE testing demand. Hybrid vehicles incorporating ICE engines require combined powertrain validation, further expanding complexity. However, ICE-related automotive test equipment market growth may moderate over time as electrification accelerates. Investment priorities among manufacturers are gradually shifting toward electric powertrain validation infrastructure.

Electric Vehicle (EV)

The electric vehicle is estimated to register the highest CAGR during the forecast period, owing to the high growth rate, which is attributed to the supportive government initiatives along with the growing popularity of EVs in recent years. The U.S. government announced plans to reduce carbon emission levels 50-52% below 2005 levels by 2030. Besides stringent regulations to curb the rising emission levels, the government is taking various initiatives to promote the electrification of vehicles.

The test equipment in EVs is primarily used for testing the interior system and components, including EV battery & charger testing, power electronics testing, and motor & engine dynamometers, to check the overall vehicle performance. For instance, motor testing equipment is used to check the torque or electric signal at high speeds of the electric vehicle through sensors, voltage probes, and other software.

Electric vehicle testing represents the fastest-growing propulsion segment within the automotive test equipment market. EV platforms require specialized high-voltage validation, battery management system calibration, and power electronics testing. Battery pack validation includes thermal runaway assessment, capacity measurement, and lifecycle durability testing. These requirements significantly expand the automotive test equipment market size within electrified production lines.

Inverter testing, motor performance validation, and regenerative braking calibration also demand advanced diagnostic infrastructure. EVs require insulation monitoring and electrical safety validation procedures not present in ICE vehicles. Software-defined vehicle architecture introduces additional testing layers. Over-the-air update validation and cybersecurity assessment are becoming integral components of EV testing ecosystems. The The

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type Analysis

Passenger Cars Segment Holds the Highest Market Size Owing to Rising Car Ownership Globally

Based on vehicle type, the market is segmented into passenger cars and commercial vehicles.

Passenger Cars

The passenger cars segment is currently the largest shareholder and is anticipated to continue doing so in the global automotive test equipment industry. The dominance can be attributed to various factors, including the increasing urban population and its commuting needs. Furthermore, electric cars are preferred over IC engine-powered vehicles due to their low operating costs, making them the preferred choice for the end-users. In addition, the growing concern over the increasing environmental pollution due to the propulsion of ICE vehicles in developed countries of Europe and North America is expected to drive the demand for electric passenger cars.

Passenger cars account for the largest share of the automotive test equipment market. High production volumes and rapid technological integration drive demand for both production and service testing solutions. Advanced driver assistance systems, infotainment integration, and connectivity features increase electronic validation requirements. Passenger car electrification amplifies demand for battery testing and high-voltage validation systems.

Regulatory safety mandates also support continuous testing investment. Crash avoidance technologies require sensor calibration and performance validation prior to vehicle delivery. Consumer expectations for reliability and safety influence manufacturer quality control strategies. Automated production testing platforms enhance defect detection and compliance efficiency. Aftermarket diagnostics within passenger car service networks further expand the automotive test equipment market size. Independent workshops require advanced tools to maintain compatibility with evolving vehicle software architectures.

Commercial Vehicles

The commercial vehicle segment is broadening in terms of sales and product range. Moreover, in countries such as China and the U.S., commercial vehicles powered by batteries are now becoming a part of the transport industry owing to the booming logistics sector. They are expected to replace conventional trucks during the forecast period. Hence, commercial vehicles are significantly contributing to the growth of the market.

Commercial vehicles represent a strategically important segment within the automotive test equipment market. Light commercial vehicles and heavy commercial vehicles require specialized validation due to load capacity and operational intensity. Fleet electrification programs significantly influence testing demand. Electric buses and delivery trucks require high-capacity battery validation systems and heavy-duty inverter testing platforms.

Durability and endurance testing are critical in commercial vehicle validation. Dynamometers and brake testing systems assess performance under sustained load conditions. Emission compliance remains central for diesel-powered commercial fleets. Periodic inspection frameworks reinforce service testing demand. Fleet operators prioritize predictive maintenance tools to minimize downtime. Advanced telematics-integrated diagnostic systems enhance operational efficiency.

Commercial vehicle testing demand is expected to grow in alignment with logistics sector expansion and electrification initiatives. Suppliers capable of delivering scalable heavy-duty validation platforms are well-positioned to capture the expanding automotive test equipment market share.

REGIONAL ANALYSIS

North America Automotive Test Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia-Pacific Automotive Test Equipment Market Analysis

Asia Pacific Held a Significant Market Share owing to the Rapid Expansion of the Automotive Industry and Technological Developments

Asia Pacific dominated the market with a valuation of USD 6.25 billion in 2025 and USD 6.47 billion in 2026. Asia Pacific is a major manufacturing center for the automotive industry. The production and sales of both traditional and electric vehicles have been increasing, driving the demand for automotive testing equipment. The expansion of this sector has driven the demand for vehicle testing equipment for quality control, emissions testing, and safety evaluations.

Asia-Pacific dominates the automotive test equipment market due to large vehicle production volumes in China, Japan, and South Korea. Rapid electrification expansion drives battery and inverter validation demand. Growing manufacturing automation supports production testing infrastructure growth.

Japan Automotive Test Equipment Market

Japan’s automotive test equipment market benefits from strong hybrid vehicle production and advanced powertrain innovation. Continuous investment in quality assurance and emission testing sustains stable growth. Electrification integration supports long-term automotive test equipment market expansion.

China Automotive Test Equipment Market

China represents the largest automotive test equipment market within the Asia-Pacific. High electric vehicle production volumes drive demand for battery and high-voltage validation systems. Government emission regulations further reinforce production and service testing growth.

North America Automotive Test Equipment Market Analysis

North America held a significant market share in 2022. Stricter vehicle emissions and safety regulations in the U.S. and Canada necessitate comprehensive testing to ensure compliance. Manufacturers require sophisticated equipment to meet these regulatory requirements.

The continuing evolution of automotive technology, including automated driving systems and driver assistance technologies, has increased the importance of automotive production testing. In 2020, NHTSA launched Automated Vehicle Transparency and Engagement for Safe Testing. As part of this initiative, states and companies can voluntarily submit information about testing of automated driving systems to NHTSA, and the public can view the information using NHTSA’s interactive tool.

North America represents a technologically advanced automotive test equipment market driven by electrification investment and strict emission standards. High electric vehicle production and strong research activity support production testing demand. Service network modernization reinforces aftermarket diagnostics expansion. These factors collectively sustain the automotive test equipment market growth across manufacturing and service ecosystems.

United States Automotive Test Equipment Market

The United States automotive test equipment market benefits from electric vehicle expansion and advanced manufacturing automation. Federal emission compliance frameworks reinforce production testing investment. Independent service networks increasingly adopt cloud-connected diagnostics. Strong original equipment manufacturer presence sustains automotive test equipment market size growth nationally.

Europe Automotive Test Equipment Market Analysis

Europe contributed a considerable market share in 2022 and is anticipated to grow at a CAGR of 3.0% over the forecast period. The growing adoption of electric vehicles is on the rise in Europe. EV manufacturers require specialized testing equipment to assess battery performance, charging infrastructure compatibility, and overall vehicle safety.

Europe’s automotive test equipment market is shaped by stringent carbon regulations and aggressive electrification targets. High adoption of battery electric vehicles increases demand for high-voltage validation systems. Regulatory enforcement ensures stable emission testing activity. These dynamics support steady automotive test equipment market growth.

Germany Automotive Test Equipment Market

Germany maintains a strong automotive test equipment market share due to its advanced automotive manufacturing base. Premium vehicle electrification and powertrain research drive production testing innovation. Continuous investment in emission and drivetrain validation infrastructure sustains growth.

United Kingdom Automotive Test Equipment Market

The United Kingdom automotive test equipment market reflects steady demand linked to emission compliance and service diagnostics modernization. Electric vehicle adoption contributes incremental high-voltage testing requirements. Service network digitalization strengthens aftermarket equipment deployment.

The rest of the world is anticipated to witness the second-highest CAGR over the forecast period. Increasing awareness of vehicle safety among consumers has led to greater demand for testing equipment for safety features, including Anti-lock Braking Systems (ABS), airbags, and Electronic Stability Control (ESC). Growing industrialization and positive economic growth have led to a growing demand for passenger cars and commercial vehicles. The high market share can be attributed to increasing investment by OEMs to set up car production facilities and growing demand for passenger cars among the middle-class income group. In January 2020, Mercedes-Benz partnered with Bosch to build a state-of-the-art Vehicle Test Center in Brazil. Besides trucks and buses, it will also be possible to test passenger cars, light commercial vehicles, and motorcycles in the future.

Industry Competitive Landscape

Focus on Partnerships and Acquisitions by Market Players to Gain a Competitive Edge

Various domestic vehicle manufacturers and international players consistently develop advanced strategies for competitive advantage. Many companies are adopting several market strategies, such as new test equipment launches, setting up test centers, acquisitions, and partnership & collaboration strategies to enable market growth.

The automotive test equipment industry is characterized by established multinational suppliers, specialized diagnostic technology firms, and software-driven solution providers. Competition centers on technological capability, regulatory compliance alignment, and integration depth across electrified vehicle architectures. Leading global vendors maintain significant automotive test equipment market share through comprehensive portfolios that include emission analyzers, dynamometers, battery validation systems, and advanced diagnostic platforms. These firms benefit from long-standing relationships with original equipment manufacturers and tier-1 suppliers.

Digital transformation is reshaping competitive positioning. Vendors integrating cloud-enabled diagnostics, artificial intelligence-based fault detection, and predictive analytics are gaining a strategic advantage. Hardware-software ecosystem integration is increasingly critical. Electrification is redefining product development priorities. Suppliers investing in high-voltage validation systems, battery pack testing modules, and inverter calibration platforms are strengthening their automotive test equipment market growth prospects.

Strategic collaborations between automotive manufacturers and equipment providers are common. Partnerships support the co-development of validation frameworks aligned with next-generation powertrain platforms. Mid-sized and regional firms compete by offering cost-efficient diagnostic solutions tailored to independent workshops. However, rapid technological evolution favors companies with strong research capabilities and scalable manufacturing infrastructure.

List of Key Companies Profiled:

- HORIBA Ltd. (Japan)

- Siemens AG (Germany)

- Continental AG (Germany)

- Robert Bosch GmbH (Germany)

- ABB (Switzerland)

- PHINIA Inc. (U.S.)

- MAHA Maschinenbau Haldenwang GmbH & Co. KG (Germany)

- K.S. Engineers (Austria)

- Softing Automotive Electronics GmbH (Germany)

- Vector Informatik GmbH (Germany)

Latest Automotive Test Equipment Industry Developments:

- January 2024: AVL List GmbH introduced an advanced electric powertrain validation bench designed to enhance high-voltage battery testing accuracy and support scalable electric vehicle production.

- May 2024: Bosch Automotive Service Solutions expanded its cloud-connected diagnostic platform to improve remote vehicle fault detection and service network integration capabilities.

- September 2024: Horiba Ltd. launched a next-generation emission testing analyzer aligned with evolving global regulatory standards and improved precision measurement technologies.

- February 2025: MAHA Maschinenbau Haldenwang GmbH unveiled an automated brake and suspension testing system aimed at enhancing production-line quality assurance efficiency.

- June 2025: Continental AG introduced an integrated battery diagnostics solution focused on improving lifecycle performance monitoring and predictive maintenance capabilities in electric vehicles.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product/service types, and leading applications of the product. Besides, the report offers insights into the automotive test equipment market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.44% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Location

|

|

By Propulsion

|

|

|

By Vehicle Type

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 11.15 billion in 2025.

The market will likely grow at a CAGR of 3.44% over the forecast period (2026-2034).

The passenger cars segment is expected to lead the market due to the rising ownership of cars globally.

Increasing demand for electric vehicles and autonomous vehicles is expected to increase the demand for global market significantly.

Some of the major players in the market are HORIBA Ltd., Robert Bosch, Continental AG, and Siemens AG.

Asia Pacific dominated the market in 2025.

High cost of testing equipment may restrain market growth.

- 2021-2034

- 2025

- 2021-2024

- 172

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us