Data Center Cooling Market Size, Share & Industry Analysis, By Product (Air Conditioners, Precision Air Conditioners, Liquid Cooling, Air Handling Unit, Chillers, and Others (Air Economizers, Heat Rejection)), By Data Center Type (Large Scale, Medium Scale, and Small Scale), By Cooling Technique (Room Based Cooling, Rack Based Cooling, and Row Based Cooling) and By Industry (BFSI, IT and Telecom, Manufacturing, Retail, Healthcare, Energy and Utilities, and Others (Government & Defense, Education)), and Regional Forecast, 2026–2034

Data Center Cooling Market Size and Future Outlook

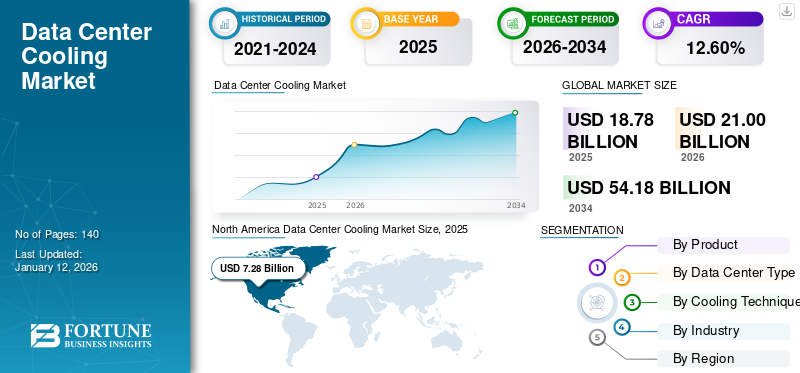

The global data center cooling market size was valued at USD 18.8 billion in 2025. The market is projected to grow from USD 21.0 billion in 2026 to USD 54.4 billion by 2034, exhibiting a CAGR of 12.6% during the forecast period.North America dominated the data center cooling market with a market share of 38.72% in 2025.

Data center cooling comprises specialized thermal management technologies and infrastructure designed to regulate temperature, humidity, and heat dissipation within data center environments to ensure reliable operation of servers, storage systems, networking equipment, and high-performance computing infrastructure. These solutions support the integration of air-based cooling systems, liquid cooling technology, chillers, heat exchangers, cooling towers, containment systems, environmental monitoring platforms, and AI-enabled thermal optimization tools to improve energy efficiency, equipment reliability, rack density, and operational continuity. Data center cooling enables operators to reduce power consumption, achieve energy savings, maintain uptime, support sustainability objectives, improve power usage effectiveness (PUE), and optimize total cost of ownership across enterprise, colocation, hyperscale, and edge data centers.

Growing investments in artificial intelligence (AI) infrastructure, cloud computing platforms, hyperscale facilities, and high-density computing environments are accelerating demand for advanced cooling systems globally. The increasing adoption of liquid cooling, immersion cooling, and free cooling technologies is further improving cooling efficiency, enabling higher rack power densities and supporting data center decarbonization initiatives. Major players operating in the market continue to invest in innovative thermal management solutions to address the growing cooling requirements of next-generation AI and cloud infrastructure.

- April 2025: Vertiv launched the Vertiv™ CoolLoop Trim Cooler, a thermal management solution designed to support AI and high-density computing applications while reducing annual cooling energy consumption in data centers.

Vertiv Holdings Co., Schneider Electric SE, Johnson Controls International plc, STULZ GmbH, and Rittal GmbH & Co. KG are among the major companies operating in the market.

Download Free sample to learn more about this report.

Data Center Cooling Market Key Takeaways

- 2025 Market Size: USD 18.8 billion

- 2026 Market Size: USD 21.0 billion

- 2034 Forecast Market Size: USD 54.4 billion

- CAGR: 12.6% from 2026–2034

- North America dominated the data center cooling market with a market share of 38.72% in 2025.

- The liquid cooling segment is expected to witness the highest growth rate, with a CAGR of 15.1% over the forecast period.

- The large scale segment is expected to witness the highest growth rate, with a CAGR of 13.4% in the coming years.

North America

The regional market generated over USD 7.28 billion in 2025, supported by expanding hyperscale data centers, AI infrastructure, and strong adoption of advanced liquid cooling technologies.

Europe

The market is expected to witness substantial growth, driven by investments in sustainable data centers, AI computing infrastructure, and energy-efficient cooling solutions across major European countries.

Asia Pacific

The market was valued at USD 3.64 billion in 2025, supported by rapid digitalization, growing cloud capacity, AI deployments, and increasing investments in high-density data center infrastructure.

U.S.

The market is estimated to reach about USD 5.26 billion in 2026, driven by continued expansion of hyperscale data centers, AI-focused computing facilities, and cloud infrastructure investments.

Japan

The Japanese market in 2026 is estimated at around USD 0.92 billion, accounting for roughly 4.2% of the global sales.

Read More

DATA CENTER COOLING MARKET TRENDS

Increased Preference for Water Conservation and Low-Water Cooling Technologies is a Key Market Trend

The market is witnessing a growing shift toward water-efficient thermal management solutions as operators seek to reduce freshwater consumption while meeting increasingly stringent sustainability and environmental objectives. Data center operators are increasingly adopting closed-loop liquid cooling systems, indirect evaporative cooling, refrigerant-based cooling, and free cooling technologies that minimize water usage without compromising cooling performance. The market is also experiencing rising integration of water recycling systems, intelligent water management platforms, and advanced heat rejection technologies to improve resource utilization and operational efficiency.

- For instance, in June 2025, LiquidStack unveiled the GigaModular™ Coolant Distribution Unit (CDU), the industry’s first modular and scalable CDU platform offering up to 10 MW of cooling capacity for high-density AI and hyperscale data center environments, enabling operators to expand liquid cooling infrastructure through a pay-as-you-grow approach.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Rack Power Densities and Next-Generation Chip Architectures are Driving Market Growth

The data center cooling market growth is increasingly being driven by the rapid increase in rack power densities resulting from the deployment of advanced GPUs, AI accelerators, high-performance processors, and next-generation server architectures. As conventional air-cooling approaches become insufficient for managing the higher thermal loads generated by modern computing infrastructure, data center operators are investing in advanced data center cooling solutions capable of delivering greater heat dissipation, improved thermal stability, and continuous system availability. The transition toward servers exceeding 30–100 kW per rack is accelerating demand for precision cooling, liquid cooling, rear-door heat exchangers, and hybrid thermal management systems that support reliable operation while improving energy efficiency. Growing adoption of high-density computing environments across hyperscale, enterprise, and colocation facilities continues to strengthen demand for innovative cooling technologies capable of supporting future computing requirements and optimizing data center performance.

- For instance, in September 2025, Vertiv introduced the Vertiv™ CoolChip CDU family, a liquid cooling coolant distribution platform designed to support high-density AI and accelerated computing environments by efficiently managing increasing rack heat loads.

MARKET RESTRAINTS

High Capital Costs and Infrastructure Challenges are Limiting Market Expansion

The growth of the market is constrained by the high capital investment requirements associated with advanced cooling infrastructure, particularly liquid cooling, immersion cooling, and high-capacity thermal management systems. Deployment of next-generation cooling solutions often requires significant modifications to existing data center layouts, power distribution systems, piping networks, and facility infrastructure, creating challenges for operators seeking to upgrade legacy facilities. The increasing complexity of AI workloads and high-density server environments has further expanded cooling requirements, leading to higher installation, maintenance, and operational costs. In addition, concerns regarding coolant management, infrastructure compatibility, water availability, and integration with existing data center architectures can delay project implementation and increase deployment risks. Budget limitations, longer return-on-investment timelines, and the shortage of specialized thermal management expertise continue to create challenges for operators seeking large-scale adoption of advanced data center cooling solutions across enterprise, colocation, hyperscale, and edge data center environments.

MARKET OPPORTUNITIES

Deployment of AI Data Centers in Water-Stressed Regions Creates Significant Opportunities for Next-Generation Cooling

A major opportunity emerging within the market is the increasing deployment of hyperscale and AI data centers in regions facing water scarcity, rising ambient temperatures, and stringent environmental regulations. These developments are driving demand for advanced data center cooling solutions capable of minimizing freshwater consumption while maintaining high cooling performance and operational reliability. Cooling technology providers are increasingly focusing on closed-loop liquid cooling systems, dry cooling, indirect evaporative cooling, refrigerant-based cooling, and intelligent water management solutions that improve thermal efficiency with lower water dependency. The opportunity is particularly strong across the Middle East, the Southwestern U.S., Australia, and other water-constrained regions where operators are prioritizing sustainable cooling infrastructure to comply with environmental regulations, improve power usage effectiveness (PUE), and support long-term AI infrastructure expansion.

- For instance, in September 2024, CoolIT Systems announced the launch of its CHx2000 liquid cooling coolant distribution unit (CDU), designed to support high-density AI and HPC deployments with cooling capacities of up to 2 MW per unit.

MARKET CHALLENGES

Increasing Rack Power Densities and Infrastructure Modernization Requirements are Challenging Market Growth

One of the major challenges affecting the market is the rapid increase in rack power densities driven by artificial intelligence, machine learning, and high-performance computing applications. Modern data centers require significantly greater cooling capacity than traditional facilities, creating challenges for operators seeking to manage heat loads while maintaining energy efficiency and sustainability targets. At the same time, many existing data centers were designed around conventional air-cooling architectures, making the transition to liquid cooling technologies complex and capital-intensive. Growing requirements for power availability, water management, cooling infrastructure upgrades, and integration with existing facility systems further increase deployment complexity. These factors create operational challenges for data center operators and cooling solution providers seeking to balance performance, cost efficiency, scalability, and environmental objectives across hyperscale, colocation, enterprise, and edge data center environments.

Segmentation Analysis

By Product

Air Handling Unit Segment Led Market Owing to Its Extensive Deployment Across Hyperscale, Colocation, and Enterprise Data Centers

By product, the market is segmented into air conditioners, precision air conditioners, liquid cooling, air handling unit, chillers, and others.

The air handling unit segment held the largest market share in 2025, as it remains a critical component of data center cooling infrastructure across enterprise, colocation, hyperscale, and edge facilities. Air Handling Units (AHUs) are extensively utilized to regulate airflow, temperature, humidity, and indoor air quality within white space environments, ensuring reliable operation of servers, storage systems, and networking equipment. Compared with other cooling products, AHUs offer broad applicability across both new-build and retrofit data center projects. They can be integrated with chilled water systems, economizers, containment solutions, and building management platforms. Their ability to support large-scale cooling operations, optimize airflow distribution, and improve thermal efficiency makes them one of the most widely deployed cooling solutions within the market. The increasing development of hyperscale facilities, cloud infrastructure, and digital transformation projects continues to reinforce demand for advanced air handling systems globally.

- For instance, in May 2025, STULZ introduced the CyberAir Mini DX series, an energy-efficient precision cooling solution designed for edge computing and small-to-medium-sized data center applications, further expanding its thermal management portfolio.

The liquid cooling segment is expected to witness the highest growth rate, with a CAGR of 15.1%, over the forecast period, driven by increasing adoption of AI infrastructure, high-performance computing (HPC), and high-density GPU deployments requiring superior heat dissipation capabilities. Growing demand for direct-to-chip cooling, immersion cooling, and advanced coolant distribution systems is accelerating the adoption of liquid cooling technologies across hyperscale and AI-ready data centers, enabling operators to improve energy efficiency, support higher rack power densities, and meet sustainability objectives.

To know how our report can help streamline your business, Speak to Analyst

By Data Center Type

Small Scale Segment Led Market Owing to Growing Deployment of Edge Computing and Enterprise IT Infrastructure

By data center type, the market is segmented into large scale, medium scale, and small scale.

The small scale segment held the largest market share in 2025. Small scale data centers are extensively deployed across enterprises, government institutions, healthcare facilities, educational organizations, financial institutions, and edge computing environments requiring localized data processing and storage capabilities. These facilities rely heavily on data center cooling solutions to maintain optimal operating temperatures, ensure equipment reliability, and support the continuous operation of servers and networking infrastructure. Compared with medium- and large-scale facilities, small-scale data centers account for a significantly higher number of installations globally, creating substantial demand for precision air conditioners, air handling units, in-row cooling systems, and intelligent thermal management solutions. The continued expansion of digital transformation initiatives, edge computing deployments, and enterprise IT modernization projects is further strengthening demand for cooling infrastructure across small-scale data center environments globally.

The large scale segment is expected to witness the highest growth rate, with a CAGR of 13.4% in the coming years, driven by rising investments in hyperscale cloud facilities, AI-ready data centers, high-performance computing infrastructure, and large-scale colocation campuses.

By Cooling Technique

Room Based Cooling Segment Led Market as It Offers Lower Deployment Complexity and Proven Reliability

By cooling technique, the market is segmented into room based cooling, rack based cooling, and row based cooling.

The room based cooling segment held the largest market share in 2025, as it remains the most widely deployed cooling architecture across enterprise, colocation, government, healthcare, and legacy data center environments. Room-based cooling solutions utilize Computer Room Air Conditioners (CRACs), Computer Room Air Handlers (CRAHs), and centralized airflow management systems to regulate temperature and humidity throughout the data hall. Compared with rack- and row-based approaches, room-based cooling offers lower deployment complexity, proven reliability, and broad compatibility with existing data center infrastructure, making it the preferred choice across a large installed base of facilities worldwide. The continued expansion of enterprise IT infrastructure, colocation facilities, and digital services is further strengthening demand for room-based cooling solutions within the market.

The rack based cooling segment is expected to witness the highest growth rate, with a CAGR of 13.4% in the coming years, driven by increasing adoption of AI infrastructure, high-performance computing (HPC), and high-density server deployments. Rack based cooling enables targeted heat removal at the source, improving thermal efficiency while supporting higher rack power densities than conventional cooling architectures.

By Industry

Increasing Need to Optimize Energy Efficiency Boosted IT and Telecom Segment Growth

By industry, the market is segmented into BFSI, IT and telecom, manufacturing, retail, healthcare, energy and utilities, and others (government & Defense, education).

The IT and telecom segment held the largest data center cooling market share in 2025. The sector accounts for a significant proportion of global investments in data centers, cloud infrastructure, telecommunications networks, and digital service platforms requiring advanced data center cooling solutions. IT and telecom operators increasingly utilize precision cooling systems, air handling units, liquid cooling technologies, and intelligent thermal management platforms to maintain equipment reliability, optimize energy efficiency, and ensure uninterrupted operation of servers, storage systems, and networking equipment.

The retail segment is expected to witness the highest growth rate, with a CAGR of 14.9% in the coming years, driven by increasing adoption of e-commerce platforms, digital payment systems, omnichannel retail operations, and data-intensive customer analytics applications.

Data Center Cooling Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Data Center Cooling Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America remains a dominating market, accounting for over USD 7.28 billion in revenue in 2025, supported by increasing investments in hyperscale data centers, artificial intelligence (AI) infrastructure, cloud computing platforms, colocation facilities, and edge data center deployments across the U.S. and Canada. Regional demand is strongly influenced by the rapid expansion of AI training clusters, high-performance computing (HPC) environments, and large-scale cloud infrastructure requiring advanced thermal management solutions. The region benefits from substantial capital expenditure on next-generation data center developments, digital infrastructure modernization, and sustainability initiatives that require energy-efficient cooling technologies to support rising rack power densities and operational reliability. Growing adoption of liquid cooling, immersion cooling, direct-to-chip cooling, and intelligent thermal management platforms is further strengthening demand for data center cooling solutions capable of improving energy efficiency, reducing operating costs, and supporting AI-driven workloads across mission-critical facilities.

U.S. Data Center Cooling Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 5.26 billion in 2026, driven by the country's extensive pipeline of hyperscale data centers, AI-focused computing facilities, cloud infrastructure developments, and colocation expansions. Demand for data center cooling remains particularly strong across facilities supporting artificial intelligence, machine learning, cloud services, financial applications, and high-performance computing environments that require advanced heat management and uninterrupted operational performance. The country continues to witness substantial investments from technology companies, cloud service providers, and colocation operators seeking to deploy high-density server infrastructure and next-generation GPU clusters. Growing emphasis on energy efficiency, sustainability targets, water conservation, and data center resilience is further accelerating the adoption of liquid cooling systems, intelligent cooling controls, and advanced thermal management technologies nationwide.

Europe

The European market is expected to witness substantial growth during the forecast period, driven by increasing investments in hyperscale data centers, cloud infrastructure, AI computing facilities, and sustainable digital infrastructure across Germany, the U.K., France, Ireland, the Netherlands, the Nordics, and other European countries. Regional demand is closely associated with growing deployment of energy-efficient data centers, stringent environmental regulations, and rising adoption of advanced cooling technologies designed to reduce power consumption and carbon emissions. Europe remains one of the most important markets for data center cooling as operators increasingly prioritize sustainability, energy performance optimization, water efficiency, and compliance with evolving environmental standards. Growing investments in liquid cooling infrastructure, AI-ready data centers, district energy integration, and green data center initiatives are creating sustained demand for advanced cooling solutions capable of supporting high-density computing environments while meeting the region's ambitious decarbonization objectives.

U.K. Data Center Cooling Market

The U.K. market in 2026 is estimated at around USD 2.10 billion, representing roughly 10.0% of global sales.

Germany Data Center Cooling Market

Germany’s market is projected to reach approximately USD 1.23 billion in 2026, equivalent to around 5.8% of global sales.

Asia Pacific

The market in Asia Pacific was valued at USD 3.64 billion in 2025 and continues to expand during the forecast period. China and Japan continue to represent major demand centers due to expanding cloud capacity, growing AI computing deployments, and increasing investments in high-density data center infrastructure. Regional market growth is strongly associated with rapid digitalization, rising internet usage, expanding colocation facilities, and growing demand for data processing capabilities. The increasing deployment of AI-ready data centers, edge computing infrastructure, and liquid cooling technologies continues to accelerate demand for advanced data center cooling solutions across the region.

China Data Center Cooling Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 1.43 billion, representing roughly 6.8% of global sales.

Japan Data Center Cooling Market

The Japanese market in 2026 is estimated at around USD 0.92 billion, accounting for roughly 4.2% of the global sales.

India Data Center Cooling Market

The Indian market in 2026 is estimated at around USD 0.90 billion, accounting for roughly 4.3% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in hyperscale data centers, cloud infrastructure, smart city programs, and digital transformation initiatives across GCC countries, South Africa, Israel, and other regional markets. Demand is closely linked to growing deployment of colocation facilities, government cloud projects, AI infrastructure, and enterprise data centers requiring advanced cooling technologies to ensure operational reliability and energy efficiency. GCC countries lead regional consumption due to significant investments in digital infrastructure, smart city developments, and large-scale data center projects. At the same time, Israel benefits from expanding technology ecosystems, cloud adoption, and increasing investments in high-performance computing facilities. Growing demand for sustainable and energy-efficient cooling solutions continues to support market expansion across the region.

GCC Data Center Cooling Market

The GCC market is projected to reach around USD 1.24 billion in 2026, representing roughly 5.9% of the global sales.

South America

The South America market is driven by increasing investments in cloud infrastructure, colocation facilities, enterprise data centers, and digital transformation initiatives across Brazil, Argentina, Chile, Colombia, and other regional markets. Market expansion is primarily driven by the growing deployment of hyperscale facilities, telecommunications infrastructure, financial services data centers, and government digitalization projects requiring reliable and energy-efficient thermal management solutions. Rising internet penetration, cloud adoption, and investments in AI-ready infrastructure are further supporting demand for advanced cooling technologies capable of improving operational efficiency, reducing energy consumption, and ensuring continuous data center performance across the region.

Brazil Data Center Cooling Market

The Brazilian market is projected to reach around USD 0.58 billion in 2026, representing roughly 2.7% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Advantage Driven by Liquid Cooling Innovation, Energy Efficiency Expertise, and AI-Ready Thermal Management Capabilities

The data center cooling market is moderately fragmented, with competitive positioning shaped by capabilities in precision cooling, liquid cooling, thermal management, airflow optimization, and energy-efficient cooling technologies across hyperscale, colocation, enterprise, and edge data center environments. Leading companies, including Vertiv Holdings Co., Schneider Electric SE, Johnson Controls International plc, STULZ GmbH, and Rittal GmbH & Co. KG, maintain strong market positions through advanced cooling portfolios, global service networks, engineering expertise, and innovative thermal management solutions supporting high-density computing environments globally.

Competitive differentiation is increasingly influenced by the ability to provide liquid cooling technologies, AI-ready cooling infrastructure, intelligent thermal management platforms, energy-efficient cooling systems, and sustainable data center solutions capable of supporting rising rack power densities. Companies are continuously investing in direct-to-chip cooling, immersion cooling, AI-driven thermal analytics, modular cooling platforms, and next-generation coolant distribution technologies to improve cooling efficiency, reduce power consumption, and support expanding AI, cloud computing, and hyperscale data center deployments globally.

- For instance, in April 2025, Vertiv introduced the Vertiv™ SmartRun modular overhead infrastructure system, integrating cooling, power, networking, and containment infrastructure to accelerate deployment of AI-ready and hyperscale data center environments.

LIST OF KEY DATA CENTER COOLING COMPANIES PROFILED

- Vertiv Holdings Co. (U.S.)

- Schneider Electric SE (France)

- Johnson Controls International plc (Ireland)

- STULZ GmbH (Germany)

- Rittal GmbH & Co. KG (Germany)

- Daikin Industries, Ltd. (Japan)

- Mitsubishi Electric Corporation (Japan)

- Trane Technologies plc (Ireland)

- Munters Group AB (Sweden)

- CoolIT Systems Inc. (Canada)

KEY INDUSTRY DEVELOPMENTS

- June 2025: LiquidStack unveiled the GigaModular™ Coolant Distribution Unit (CDU), the industry’s first modular CDU platform delivering up to 10 MW of cooling capacity for AI and hyperscale data centers, enabling scalable liquid cooling deployments.

- March 2025: Munters launched the SyCool® Split indirect evaporative cooling solution for data centers, designed to improve cooling efficiency and reduce energy consumption in high-density computing environments.

- November 2024: STULZ launched the CyberCool CMU cooling management unit, designed to optimize liquid cooling operations and improve thermal efficiency in high-density AI and HPC data center environments.

- August 2024: Johnson Controls enhanced its YORK® YVAM air-cooled magnetic bearing chiller platform for mission-critical facilities, supporting improved energy efficiency and reduced cooling-related operating costs in data centers.

- July 2024: Trane Technologies introduced advanced thermal management solutions for hyperscale data centers, enabling operators to improve cooling performance while supporting sustainability and decarbonization goals.

REPORT COVERAGE

The global data center cooling market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key Industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.6% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Data Center Type, Cooling Technique, Industry, and Region |

| By Product |

|

| By Data Center Type |

|

| By Cooling Technique |

|

| By Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 18.8 billion in 2025 and is projected to reach USD 54.4 billion by 2034.

In 2025, the North America’s market value stood at USD 7.28 billion.

The market is expected to exhibit a CAGR of 12.6% during the forecast period (2026-2034).

By industry, the IT and Telecom segment led the market.

Rapid expansion of AI infrastructure and hyperscale data centers is driving market growth.

Vertiv Holdings Co., Schneider Electric SE, Johnson Controls International plc, STULZ GmbH, and Rittal GmbH & Co. KG are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us