Regenerative Medicine Market Size, Share & Industry Analysis, By Product (Cell Therapy {Cellular Immunotherapy, Mesenchymal Stem Cell Therapy, Fibroblast Cell Therapy, Hematopoietic Stem Cell Therapy, and Others}, Gene Therapy, Tissue Engineering, and Platelet Rich Plasma), By Application (Orthopedics, Wound Care, Oncology, Rare Diseases, and Others), By End User (Hospitals, Clinics, and Others), and Regional Forecast, 2026-2034

(Offer valid till 31st Jul 2026)

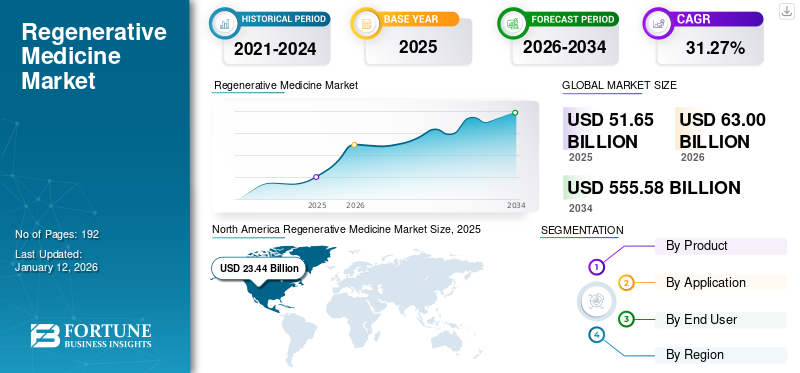

Regenerative Medicine Market Size and Future Outlook

The global regenerative medicine market size was valued at USD 48.17 billion in 2025. The market is projected to grow from USD 58.40 billion in 2026 to USD 360.84 billion by 2034, exhibiting a CAGR of 25.56% during the forecast period. North America dominated the regenerative medicine market with a market share of 43.01% in 2025.

Regenerative medicine utilizes cell therapy, gene therapy, tissue engineering, biomaterials, and biologics to restore, replace, or regenerate damaged tissues and organ function. The global market is expanding due to the increasing clinical adoption of cell and gene therapies, broader investment in stem cell and tissue-engineering platforms, rising demand for regenerative solutions in various applications, and continued progress in scalable manufacturing, cryopreservation, gene-editing, and 3D bio printing technologies. Market growth is also being supported by a rising number of approved cellular and gene therapy products, stronger translational research pipelines, and improving regulatory and reimbursement pathways in major healthcare markets.

Key companies include Novartis AG, Gilead Sciences, Inc., Astellas Pharma Inc., Smith+Nephew plc, Integra LifeSciences Corporation, and others. These firms are concentrating on cell-based therapeutics, gene-modified therapies, tissue-engineered constructs, wound-healing and orthopedic regeneration products, to support commercialization, therapy delivery, and expansion across hospital, specialty clinic, and research settings.

Download Free sample to learn more about this report.

Regenerative Medicine Market Trends

Dynamic Acquisitions by Key Market Players to Upscale R&D Capabilities in Regenerative Field

Dynamic acquisitions are emerging as a notable trend in the sector as firms aim to rapidly enhance their R&D capabilities, clinical pipelines, and manufacturing expertise. Rather than developing all capabilities in-house, major companies are buying innovative firms that possess specialized technologies in cell therapy, gene therapy, tissue engineering, or biomaterials. This allows them to reduce development timelines, enhance platform depth, and venture into valuable regenerative indications. These purchases also provide buyers with access to scientific expertise, unique delivery systems, and advanced-stage assets that can enhance commercialization opportunities. With increasing competition, inorganic expansion is becoming a crucial method for rapidly scaling regenerative portfolios. This trend is particularly pronounced in advanced therapy fields where technical intricacy and regulatory demands render established skills extremely valuable. In general, acquisitions assist market players in expanding their product lines while enhancing their capacity for long-term innovation. These factors are supporting the overall global regenerative medicine market growth.

- For instance, in February 2026, gene therapy company Bluebird bio was acquired by a consortium of private equity firms such as the Carlyle Group and SK Capital Partners, in a deal that was potentially valued at USD 96.0 million. This will provide Bluebird with the primary capital to provide commercial delivery of therapies for patients with sickle cell disease, β-thalassemia, and cerebral adrenoleukodystrophy.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Investments in Inorganic Initiatives by Industry Players to Augment Market Growth

Rising investments in inorganic initiatives are driving the market as companies’ leverage acquisitions, partnerships, and licensing agreements to accelerate growth in cell therapy, gene therapy, tissue engineering, and associated platforms. These agreements enable companies to tap into new technologies, pipeline resources, distribution methods, and specialized scientific expertise without needing to begin anew. Consequently, the timelines for product development may be reduced and the productivity of R&D can enhance. Inorganic investments assist companies in exploring new therapeutic fields, enhancing manufacturing preparedness, and boosting their capacity to advance regenerative candidates into clinical development. This is particularly crucial in regenerative medicine, where the complexity of technology and the demands for scaling up are significant. With the increasing adoption of external agreements by companies to enhance their capabilities, the market experiences swifter innovation, expanded pipelines, and enhanced commercialization opportunities. This trend is facilitating long-term market growth by making more sophisticated regenerative therapies more accessible to patients.

- For instance, in February 2026, Gilead Sciences, Inc., announced its plans to acquire Arcellx, to expand upon the two companies’ successful 2022 collaboration for the co-development and co-commercialization of Arcellx’s lead pipeline candidate of anitocabtagene autoleucel (anito-cel), an investigational BCMA-directed CAR T-cell therapy for patients with multiple myeloma.

Download Free sample to learn more about this report.

MARKET RESTRAINT

High Treatment Costs and Inadequate Reimbursement Policies to Hinder Market Growth

High treatment expenses and restricted reimbursement continue to be significant barriers in the regenerative medicine sector, as numerous cell, gene, and tissue-based therapies necessitate intricate production, specialized management, and precisely regulated delivery environments, consequently increasing the total cost of care. This complicates the widespread adoption of these therapies by hospitals, payers, and patients. When reimbursement options are vague or inconsistent, providers might be reluctant to suggest treatment, and patients could experience delays in access. The difficulty is greater in advanced therapies, where the costs for single treatments can be quite steep, and payers are still evaluating their long-term value. Consequently, even regenerative products with clinical promise may experience sluggish market adoption. This restricts patient access, hinders revenue transparency for developers, and may postpone wider market growth.

- As per an article published by DVC Stem in September 2025, stem cell therapy costs between USD 5,000 – USD 50,000, and the cost varies depending upon multiple factors such as the type of stem cells administered, number of cells administered, the quality of cells, source of stem cells and many more.

MARKET OPPORTUNITIES

Advances in Tissue Engineering to Offer Lucrative Growth Opportunities

Improvements in tissue engineering are generating significant growth prospects in the sector as they enhance the repair or reconstruction of damaged skin, bone, cartilage, cornea, and soft tissues. Improved scaffold designs, extracellular matrix innovations, biomaterials, and bioactive delivery systems are aiding developers in producing products that promote more efficient tissue regeneration. These enhancements are also rendering regenerative solutions more focused and applicable in clinical settings for wound care, orthopedics, dental uses, and ophthalmology. With the advancement of tissue-engineered products, healing results can enhance, complications may decrease, and a larger group of patients could gain from regenerative therapies. This is fostering increased product development, enhanced clinical activity, and wider commercialization initiatives throughout the market. It is additionally creating chances for businesses to develop unique portfolios in high-burden chronic and degenerative diseases. In general, ongoing advancements in tissue engineering are broadening the commercial potential of regenerative medicine and facilitating sustained market growth. All these factors would drive the market growth in the coming years.

- For instance, in February 2026, StimLabs announced the U.S. FDA 510(k) clearance for DermaForm, a collagen scaffold particulate wound care device. It strengthened the company’s portfolio of regenerative solutions for chronic and acute wounds.

MARKET CHALLENGES

Manufacturing Complexity to Challenge Market Growth

Manufacturing complexity remains a major challenge in the market as many cell, gene, and tissue-based therapies involve living materials, patient-specific processing, cold-chain handling, and highly controlled clean-room production. These steps make scale-up difficult and increase the risk of batch variability, quality deviations, and supply delays. Compared with conventional drugs, regenerative products often need more complex release testing, stricter process validation, and tighter coordination across collection, manufacturing, and treatment sites. This slows commercialization and raises production costs. It also makes it harder for companies to move from small clinical batches to reliable large-scale supply. All the factors cumulatively affect the market growth.

- For instance, in January 2025, Atara Biotherapeutics’ EBVALLO (tabelecleucel), received the U.S. FDA Complete Response Letter solely related to inspection findings at a third-party manufacturer.

Segmentation Analysis

By Product

Cell Therapy to Gain Traction Due to Increase in Product Adoption to Treat Chronic Diseases

Based on product, the market segments includes cell therapy, gene therapy, tissue engineering, and platelet rich plasma.

In 2025, cell therapy captured the largest global market share by product. This is due to its broader use in various applications compared to many other product types. Its prevalence is further bolstered by the increasing quantity of clinical programs employing stem cells, T cells, NK cells, and various cell-based platforms to mend, substitute, or rejuvenate damaged tissues. Moreover, cell therapy has achieved greater commercial momentum as an increasing number of developers focus on scalable manufacturing, cryopreservation, and delivery technologies. These elements combined have allowed the segment to preserve its top status in the worldwide market.

- For instance, in January 2026, IREGENE announced that the U.S. FDA granted RMAT designation to NouvNeu001, its iPSC-derived cell therapy for Parkinson’s disease. The company said this was the world’s first allogeneic iPSC therapy to receive both Fast Track Designation and RMAT.

The tissue engineering segment is anticipated to rise with a CAGR of 21.07% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Rising Prevalence of Orthopedic Diseases to Fuel Product Adoption in Orthopedics

In terms of application, the global market is segmented into orthopedics, wound care, oncology, rare diseases, and others.

The orthopedics segment held the maximum global regenerative medicine market share in 2025. The factors primarily responsible for the segment’s growth are the increasing prevalence of orthopedic diseases, rising demand for tissue engineered products for bone and tissue repairs, and growing demand for innovative treatment methods to reduce the length of stay in hospitals.

- For instance, in May 2025, APEX Biologix, announced an exclusive distribution agreement with Bioventus for the XCELL PRP system throughout the U.S. for the indications of orthopedics and sports medicine.

The wound care segment is anticipated to rise with a CAGR of 24.83% over the forecast period.

By End User

Increasing Number of Surgeries to Propel Product Use across Hospitals

On the basis of end user, the global market is classified into hospitals, clinics, and others.

The hospitals segment held the maximum share of the market in 2025. The factors primarily responsible for the segmental growth are favorable government support through policy harmonization and initiatives to provide a favorable marketplace for major companies offering regenerative medicines coupled with the rising number of hospitals globally.

- For instance, according to the European Society for Blood and Marrow Transplantation (EBMT) Registry February 2026 data, 927,080 transplants have taken place in the European region and over 17,794 patients received CAR T-cell therapy in the region.

The clinic segment is projected to witness a CAGR of 25.73% over the study period.

Regenerative Medicine Market Regional Outlook

Regionally, the global market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Regenerative Medicine Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The regional growth is mainly driven by strong regulatory support for cell and gene therapies, a high number of clinical trials, large biopharma funding, and the presence of advanced manufacturing infrastructure. North America recorded a market size of USD 23.44 billion in 2025, capturing 45.38% of the global market share, and is projected to reach USD 28.72 billion in 2026.

U.S. Regenerative Medicine Market

The U.S. market led the North American region and is projected to be approximately USD 23.60 billion in 2026, representing about 40.4% of the global market.

Europe

The European market is expected to witness a growth rate of 21.62% over the forecast period. Rising Advanced Therapy Medicinal Product (ATMP) activity, stronger collaboration between regulators and industry, and expanding adoption of regenerative therapies across major healthcare systems are driving factors for the regional growth.

U.K. Regenerative Medicine Market

The U.K. market in 2026 is estimated at around USD 3.57 billion, representing roughly 6.1% of global revenues.

Germany Regenerative Medicine Market

Germany market size is projected to reach approximately USD 4.18 billion in 2026, equivalent to around 7.1% of global sales.

Asia Pacific

The Asia Pacific market size is expected to reach a valuation of USD 12.08 billion by 2026. The growth is being driven by favorable policy support in countries such as Japan, increasing public and private investment in such medicine, and rising demand for advanced therapies in aging populations.

Japan Regenerative Medicine Market

The Japan market in 2026 is estimated at around USD 3.33 billion, accounting for roughly 5.7% of global revenues.

China Regenerative Medicine Market

China’s market is projected to reach revenues of around USD 3.01 billion in 2026, representing roughly 5.2% of global sales.

India Regenerative Medicine Market

The India market in 2026 is estimated at around USD 1.89 billion, accounting for roughly 3.2% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness a slower growth over the study period. The market growth is supported by improving regulatory pathways for advanced therapy products, increasing manufacturing interest, and a rising disease burden that is creating demand for innovative cell-based treatments. The Latin America market in 2026 is estimated at around USD 3.92 billion.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 1.07 billion by 2026, representing about 1.8% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Players Generate Strong Sales Owing to New Product Launches and Approvals

Regarding the competitive environment, the market is very dispersed, with several firms controlling a larger share of the sector. Regarding cell and gene therapies, Gilead Sciences Inc. and Novartis AG are leading companies in these areas. It is due to their robust CAR T-cell therapy pipeline, expected to yield significant sales from new product launches and approvals throughout the forecast period. Additional emerging companies in the cell and gene therapy sector involve Orchard Therapeutics plc with its offerings, including Libmeldy and Strimvelis, both of which are authorized in the European Union, along with bluebird bio, Inc.

Stryker leads the global market in tissue engineering following its acquisition of Wright Medical Group N.V., resulting in a robust biologics portfolio for the company, whereas the platelet-rich plasma segment shows a divided competitive environment. Nevertheless, several major companies such as Zimmer Biomet, due to its GPS III Platelet Concentration System, and Terumo Corporation have secured their position in the market due to their robust product portfolios.

LIST OF KEY REGENERATIVE MEDICINE COMPANIES PROFILED

- Integra LifeSciences (U.S.)

- Novartis AG (Switzerland)

- Tissue Regenix (U.K.)

- Bristol-Myers Squibb Company (U.S.)

- Smith & Nephew plc (U.K.)

- MIMEDX Group, Inc. (U.S.)

- AbbVie Inc. (S.)

- Stryker (S.)

- American CryoStem Corporation (U.S.)

- EHL BIO. (South Korea)

KEY INDUSTRY DEVELOPMENTS

- March 2026: The European Commission approved Hemgenix (CSL/uniQure) as a one-time gene therapy for adults with severe or moderately severe haemophilia B (without a history of Factor IX inhibitors).

- February 2026: Cellipont Bioservices and Soter Bio announced a strategic collaboration to support integrated U.S. cell therapy manufacturing.

- February 2026: The U.S. FDA approved AUCATZYL (obecabtagene autoleucel), for adults with relapsed or refractory B-cell precursor acute lymphoblastic leukemia.

- February 2026: BioLife Solutions signed a multi-year supply agreement with Qkine Limited to expand its product portfolio into the rapidly growing cytokines market.

- January 2026: bioMérieux acquired Accellix to strengthen the pharmaceutical quality control and accelerate advanced therapies such as cell and gene therapies.

REPORT COVERAGE

The global regenerative medicine market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides understanding of essential factors, including technological progress, product innovations, the regulatory environment, and the launch of new products. Additionally, the global market report details partnerships, mergers & acquisitions, technological advancements, as well as key developments in the industry within the market. The global market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 25.56% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, End User, and Region |

| By Product |

|

| By Application |

|

|

By End User

|

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market is projected to grow from USD 48.17 billion in 2025 to USD 360.84 billion by 2034.

In 2025, the market stood at USD 20.72 billion.

Recording a CAGR of 25.56%, the market will exhibit steady growth during the forecast period.

The cell therapy segment is expected to be the leading segment based on product in this market during the forecast period.

The increasing prevalence of blood cancers and treatment initiatives for rare diseases, coupled with the rising need for personalized treatment, are some of the major factors driving the growth of the market.

Novartis AG, Stryker, and Bristol-Myers Squibb Company are the leading market players in the global market.

North America dominated the market in 2025.

The demand for cosmetic rejuvenation procedures, potential pipeline candidates, and continuous increase in R&D investment for technological advancements are expected to surge the demand for these products.

- 2021-2034

- 2025

- 2021-2024

- 167

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us