Telemedicine Market Size, Share & Industry Analysis, By Type (Products and Services), By Modality (Store-and-forward (Asynchronous), Real-time (Synchronous), and Others), By Application (Teleradiology, Telepathology, Teledermatology, Telecardiology, Telepsychiatry, and Others), By End-User (Healthcare Facilities, Homecare, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

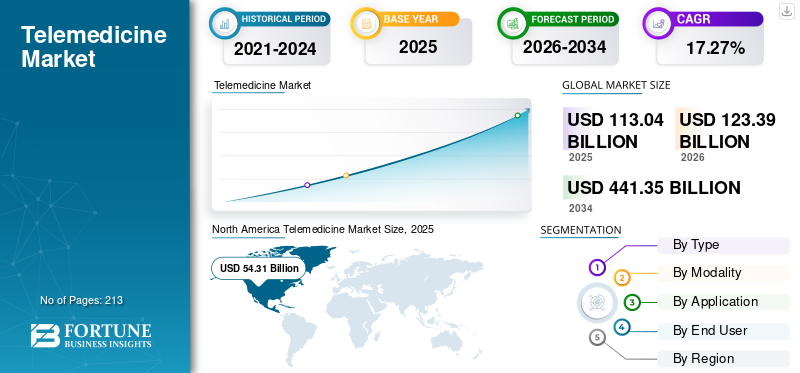

Telemedicine Market Size and Future Outlook

The global telemedicine market size was valued at USD 113.04 billion in 2025. The market is projected to be worth USD 123.39 billion in 2026 and reach USD 441.35 billion by 2034, recording a CAGR of 17.27% during the forecast period. North America dominated the telemedicine market with a market share of 48.04% in 2025.

Telemedicine involves the remote provision of healthcare services such as consultations, exams, and monitoring through technology, including video calls, smartphones, and secure messaging. It allows patients to engage with providers from home, improving access for rural regions and chronic care management while saving time and lowering travel expenses. Telemedicine adoption accelerated during and after the COVID-19 pandemic. The market shows strong growth driven by reimbursement reforms, increasing digital health infrastructure, and demand for remote care access. Additionally, the increased prevalence of chronic diseases also boosts market growth.

- For instance, the WHO also reports a significant rise in the prevalence of chronic diseases, with non-communicable diseases such as cardiovascular diseases, cancer, respiratory diseases, and diabetes responsible for over 74% of all deaths globally.

Moreover, the market shows a highly fragmented structure with companies such as Teladoc Health, Inc., American Well, Included Health, Inc. (Doctor On Demand), and others offering advanced services and product offerings.

Download Free sample to learn more about this report.

TELEMEDICINE MARKET TRENDS

Increasing Investment in Digital Health Platforms and Remote-Monitoring Devices Identified as Prominent Trend

In recent years, the investment in digital health platforms is rising as telemedicine is shifting from video visits to longitudinal, data-driven care, which needs stronger platforms, integrations, and always-on monitoring. Payers and providers are backing digital health tools that can reduce avoidable visits and admissions by detecting deterioration earlier through connected devices and analytics. This is pushing capital into enterprise-grade virtual care platforms and into remote monitoring ecosystems. In addition, funding is also concentrating on solutions with clear ROI and scalable deployments, especially chronic care pathways. Furthermore, alongside software, device-side innovation is accelerating as monitoring hardware becomes more clinical-grade, improving signal quality and expanding reimbursable use-cases (e.g., cardiac monitoring). As these investments mature, telemedicine providers can offer higher-acuity virtual care, boosting adoption and revenue per patient beyond single consults.

- For instance, in February 2025, VitalConnect reported a USD 100 million investment to expand its patient monitoring products, reflecting rising capital flows into remote-monitoring devices that underpin telemedicine-at-scale.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Technological Advancements and New Product Launches in Telemedicine Services to Bolster Market Growth

Technological progress in telemedicine services is expected to greatly enhance market expansion during the forecast timeline. Cutting-edge technologies enable patients to connect with healthcare providers who can offer assessments, therapies, diagnoses, and guidance from the comfort of their homes. Moreover, the existence of numerous established and new competitors, along with the introduction of innovative telemedicine services for issues including rare diseases, epilepsy, mental health, and weight control. These offerings are more focused on patients and flexible to the needs of various populations and are anticipated to boost market growth.

- For instance, in January 2026, Amazon One Medical introduced its Health AI assistant within the One Medical app to offer 24/7 tailored health guidance, assist users with lab results/medications, and facilitate appointment and prescription processes.

- Similarly, in November 2025, Doc.com revealed the launch of its telemedicine platform and services in the U.S., focusing on an AI-driven experience and enhanced accessibility.

- Also, in November 2025, TytoCare revealed a collaboration with Teladoc Health to enhance virtual primary and urgent care through in-home, clinical-quality remote physical exams, increasing diagnostic assurance beyond video-only services.

MARKET RESTRAINTS

Uncertainty in Long-Term Reimbursement Levels in Some Markets after Pandemic-Era Flexibilities Expire to Hinder Growth Prospects

Long-term reimbursement uncertainty acts as a constraint on the market when temporary pandemic-era payment flexibilities are extended multiple times with shifting deadlines. Providers and telehealth platforms cannot accurately predict visit volumes, unit economics, and clinician capacity if payers might revoke coverage, limit eligible services, or lower payment parity. This causes health systems to be wary of expanding virtual-first care pathways and deters investment in new specialties or rural/home-based models. It increases contracting friction, as payers might be reluctant to agree to multi-year telehealth rates while regulations are still uncertain. Consequently, businesses frequently postpone growth, restrict reimbursable services, or move additional offerings to cash-only, hindering widespread acceptance. The effect is more pronounced in markets where reimbursement policies vary significantly between states/payers and where eligibility can shift suddenly.

- For instance, in October 2025, ATA Action issued a press release warning that the expiration of Medicare telehealth flexibilities during the government shutdown was creating a ripple effect on telehealth reimbursement and patient-care disruptions.

Such scenarios hinder the adoption of telemedicine services, thereby restricting the telemedicine market growth.

MARKET OPPORTUNITIES

Integration of Advanced Technologies to Contribute to Future Growth Prospects

The incorporation of cutting-edge technologies presents a market opportunity as it enhances virtual care’s accuracy, scalability, and clinical-grade standards beyond mere virtual consultations. Artificial intelligence can streamline triage, documentation, and risk assessment, enabling clinicians to manage more patients while maintaining high-quality care. Additionally, remote patient monitoring (RPM) and linked devices provide continuous streams of vital signs and symptoms, allowing for earlier interventions and improved outcomes in chronic care. Also, cloud-native platforms combined with interoperability decrease workflow barriers, allowing telemedicine to integrate seamlessly into standard care processes and hospital command operations. Collectively, these technological components elevate telemedicine from one-time consultations to continuous, results-oriented care models.

- For instance, in October 2025, Teladoc Health announced a new workplace safety capability added to its AI-enabled Clarity monitoring solution for hospitals, using video/audio cues and AI to detect escalating risk and alert care teams.

MARKET CHALLENGES

Data Security and Privacy Concerns to Limit the Adoption

Concerns regarding data security and the privacy act as barriers hindering the broad implementation of telemedicine. With healthcare progressively moving to digital platforms, safeguarding sensitive patient information is of the highest importance. Patients might be concerned about the risk of data breaches, unauthorized access to their health records, and the misuse of their information, potentially resulting in identity theft and other privacy infringements.

- For example, in February 2025, the HIPAA Journal reported that the Department of Health and Human Services (HHS) Office for Civil Rights (OCR) noted an average of 61 healthcare data breaches per month in 2024, with 66 breaches recorded in January 2025 alone. In total, there were 729 data breaches affecting 185,798,538 individuals in the U.S. in 2024.

Such a significant number is affecting the individual's trust in the adoption of digital healthcare and thus hampering the overall market growth.

SEGMENTATION ANALYSIS

By Type

Product Launches for Seamless Service Offering to Bolster Services Segment Growth

Based on type, the market is divided into services and products.

The services segment is expected to account for 62.19% of the market in 2026. The leading portion of the segment is primarily attributed to the growing number of care centers offering telehealth services, expanding government initiatives for reimbursement, and the rising trend of outsourcing services such as teleradiology in developing countries. In addition, the market is experiencing significant growth in low-friction care approaches, including asynchronous consultations, digital intake, and AI-driven triage, which lessen clinician burden and decrease time-to-care, enhancing the cost-efficiency proposition for payers and employers.

- For instance, in September 2024, Cigna Healthcare / MDLIVE launched an “E-Treatment” option that provides urgent care without live phone/video, improving speed and lowering operational effort for simple cases.

The products segment is anticipated to rise with a CAGR of 16.64% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Modality

Growing Demand for Store-and-Forward (Asynchronous) Teleconsultations to Boost Segment Growth

On the basis of modality, the market is segmented into store-and-forward (asynchronous), real-time (synchronous), and others.

The store-and-forward (asynchronous) segment dominated the market in 2025 as it removes the live scheduling constraint and lets clinicians review cases in batches, boosting throughput and lowering cost per consult. It also fits high-volume, image/data-driven use cases where the patient does not need to be present in real time. Moreover, it works reliably in low-bandwidth settings, expanding reach in rural/remote areas and among patients with limited connectivity. Thus, providers prefer it for workflow efficiency as it integrates cleanly with EHR messaging, triage queues, and documentation. It also scales better for specialists, who can respond when available while maintaining SLAs. Furthermore, the teleradiology segment is anticipated to hold a dominant market share of 89.69% in 2026.

- For instance, In December 2025, BrainCheck announced an NIH SBIR Phase I grant to advance its eConsult platform, where specialists review cases asynchronously and provide written recommendations through a secure interface.

The real-time (synchronous) segment is anticipated to rise with a CAGR of 17.57% over the forecast period.

By Application

Persistent Radiologist Shortages Boosted Adoption of Teleradiology Services

Based on application, the market is divided into teleradiology, telepathology, teledermatology, telecardiology, telepsychiatry, and others.

The teleradiology segment dominated the market in 2025 and is anticipated to maintain its dominance throughout the forecast period. This can be attributed to persistent radiologist shortages and uneven subspecialty availability, and demand for rapid decisions in cases of emergency. It also enables continuous coverage and faster turnaround times, which improves patient flow and reduces length of stay. Additionally, increasing strategic initiatives by operating players also supported the segment growth. Furthermore, the segment is set to hold a 36.7% share in 2026.

- For instance, in October 2025, VSee Health highlighted the rapid scale-up of its teleradiology business with 100,000+ radiology reads within months of launch.

The telepsychiatry segment is anticipated to rise with a CAGR of 18.10% over the forecast period.

By End-User

Increasing Adoption of Telemedicine among Healthcare Facilities Supported Their Leading Position

In terms of end-user, the market is segmented into homecare, healthcare facilities, and others.

The healthcare facilities segment held the dominant global market share in 2025. Primary factors attributed to the growth of the segment include increasing adoption of telemedicine in routine capacity management such as virtual wards, specialist advice pathways, remote monitoring programs and others. In addition, facilities are investing in virtual nursing/command-center models to reduce bedside workload and improve patient throughput, expanding telemedicine beyond outpatient visits. Furthermore, the segment is set to hold a 55.8% share in 2026.

- For instance, in September 2025, Henry Ford Jackson Hospital launched a virtual nursing model, reporting large task volumes handled by virtual nurses in early operations.

The homecare segment is expected to grow at the fastest CAGR of 18.10% over the forecast period.

TELEMEDICINE MARKET REGIONAL OUTLOOK

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Telemedicine Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 53.81 billion in 2025, capturing 48.05% of global revenue, and is estimated to reach USD 59.39 billion in 2026. The regional dominance is driven by strong reimbursement frameworks, the presence of advanced healthcare facilities with the integration of digital health, and the presence of major players offering innovative products & services.

U.S. Telemedicine Market

The U.S. held a significant share of the North America region and is expected to maintain its dominance during the forecast period. The U.S. market size is projected to be USD 54.26 billion in 2026, accounting for roughly 44.0% of the global market.

Europe

In 2025, Europe held 25.52% of the global market, reaching a valuation of USD 28.58 billion, and is projected to grow to USD 31.36 billion in 2026. The market in Europe is anticipated to grow at a 16.27% CAGR during the forecast period. The region is anticipated to account for the second-highest. The European market is majorly driven by new service launches and strategic activities among the key native players, and the implementation of supportive government guidelines for using digital health.

U.K. Telemedicine Market

The U.K. market in 2026 is estimated at around USD 5.46 billion, representing roughly 4.4% of global revenues.

Germany Telemedicine Market

Germany's market size is projected to reach approximately USD 7.54 billion in 2026, equivalent to 6.1% of global sales.

Asia Pacific

The market in Asia Pacific reached USD 20.07 billion in 2025, representing 17.92% of total market revenue, and is projected to reach USD 22.99 billion in 2026. The region is expected to grow with the highest CAGR during the forecast period. Prominent factors supporting market growth include rising investments in digital infrastructure, increasing demand for virtual care and remote patient monitoring, and others.

Japan Telemedicine Market

The Japan market in 2026 is estimated at around USD 5.55 billion, accounting for roughly 4.5% of global revenues.

China Telemedicine Market

China’s market is projected to reach revenues of around USD 4.6 billion in 2026, representing roughly 3.6% of global sales.

India Telemedicine Market

The India market in 2026 is estimated at around USD 4.91 billion, accounting for roughly 4.0% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions would grow at a relatively slower rate over the study period. In 2025, the Middle East & Africa market stood at USD 3.44 billion, representing 3.07% of global demand, and is projected to grow to USD 3.7 billion in 2026. Latin America maintained a strong presence in the global market, reaching USD 6.1 billion in 2025, accounting for 5.45% share, and is expected to reach USD 6.56 billion in 2026. These regions are expected to grow steadily as countries focus on telehealth roadmaps and digital infrastructure improvement to reach remote populations, though the adoption pace remains uneven by country.

GCC Telemedicine Market

In the Middle East & Africa region, the GCC market in 2026 is estimated at around USD 1.52 billion, accounting for roughly 1.2% of global revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Strategic Initiatives with Other Players to Strengthen Market Position of Global Players

The global telemedicine market exhibits a highly fragmented competitive environment, with no individual entity shaping the market's growth path. Key players in the market are Teladoc Health, Inc. and American Well, both of which retained a notable portion of the global market in 2025. A substantial clientele, a well-established network of general practitioners and specialists, along with strategic partnerships, are the key elements that have enabled these companies to have a strong presence in this market.

PING AN HEALTHCARE AND TECHNOLOGY COMPANY LIMITED and GlobalMed Holdings, LLC also possessed significant portions of the market. The availability of numerous services and products aimed at managing different chronic illnesses, along with strategic efforts to enhance their geographic reach, is projected to support the expansion of these businesses.

- For instance, in January 2025, American Well announced that Vida Health’s virtual cardiometabolic care is a part of the clinical programs portfolio on the Amwell platform.

LIST OF KEY TELEMEDICINE COMPANIES PROFILED

- American Well (U.S.)

- Teladoc Health, Inc. (U.S.)

- Included Health, Inc. (Doctor On Demand) (U.S.)

- The Cigna Group (MDLIVE, Inc.) (U.S.)

- Encounter Telehealth (U.S.)

- PING AN HEALTHCARE AND TECHNOLOGY COMPANY LIMITED (China)

- Push Dr (Square Health Limited) (U.K.)

- GlobalMed Holdings, LLC (U.S.)

- MeMD (Fabric Labs, Inc.) (U.S.)

- Dictum Health Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: VSee Health and DocBox announced a strategic partnership to launch an AI-enabled Virtual ICU platform for hospitals.

- October 2025: DocGo acquired SteadyMD, adding a virtual care platform to expand telehealth services across all 50 U.S. states.

- June 2025: Hims & Hers announced an agreement to acquire ZAVA, expanding its telehealth platform across the U.K. and entering Germany, France, and Ireland.

- May 2025: Equum Medical and Prime Healthcare renewed and expanded their telehealth partnership to broaden virtual services across additional Prime hospitals.

- March 2025: GlobalMed Holdings, LLC, signed a distribution agreement with ADS to improve access to care and operational efficiency.

REPORT COVERAGE

The global telemedicine market analysis report emphasizes offering an industry overview and examining the market dynamics. The market forecast report includes market analysis, analyzing the drivers, restraints, opportunities, challenges, and trends influencing the market. The report also highlights an overview of these services, technological advancements, internet users and penetration data, and key developments within the industry, as well as by major players in the market. Furthermore, the report explores the reimbursement and regulatory scenarios in different regions and the impact of the COVID-19 pandemic on the industry. It provides an overview of the market situation during this period.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 17.27% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Application, Modality, End-User, and Region |

| By Type |

|

| By Application |

|

| By Modality |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

The global market value stood at USD 113.04 billion in 2025 and is projected to reach USD 441.35 billion by 2034.

The value of the market in North America was USD 54.31 billion in 2025.

The market is projected to register a CAGR of 17.27% during the forecast period.

By type, the services segment led the global market.

A significant reduction in healthcare costs and technological advancements are the key factors driving the global market.

American Well and Teladoc Health, Inc. are some of the prominent players in the global market.

North America held the largest market share.

Increasing patient demand for convenience and access to healthcare, especially in rural areas, is expected to drive the adoption of this service.

- 2021-2034

- 2025

- 2021-2024

- 213

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us