Smart Grid Market Size, Share & Industry Analysis, By End-user (Utility, Industrial, Residential, and Commercial), By Component (Software, Hardware, and Services), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

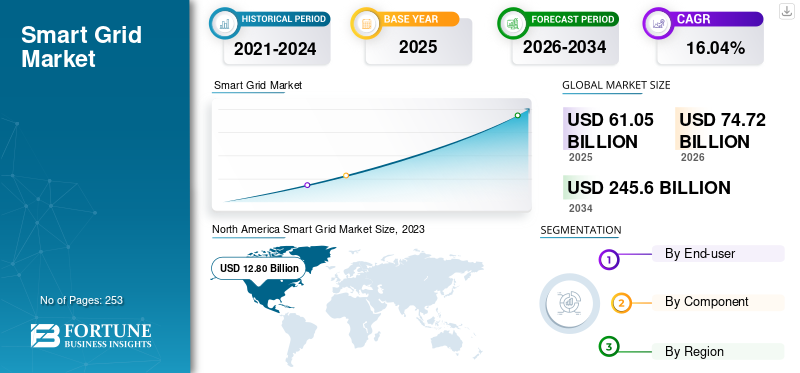

The global smart grid market size was USD 61.05 billion in 2025. The market is projected to grow from USD 74.72 billion in 2026 to USD 245.60 billion by 2034 at a CAGR of 16.04% during the forecast period. North America dominated the smart grid market with a market share of 30.91% in 2025.

A smart grid is an advanced electricity supply network that utilizes digital communications technology to identify the demand of electricity in real-time, react to local changes in usage, and enable the network to self-heal automatically in case of a power disturbance. It is an intelligent overlay to the existing electrical grid network with advanced feedback alternatives such as active network management (ANM) systems and demand response management systems (DRMS). The highly interconnected network uses meters, sensors, digital controls, and analytic tools to monitor, automate, and control energy flow. It further provides an efficient and reliable power supply through different advanced applications and technologies, thus offering new opportunities for the economy and the environment. The governments of emerging economies recognize such technology as the strategic infrastructural investment that can aid their long-term economic prosperity and help them achieve carbon emission targets.

Attributed to the COVID-19 pandemic, various industries and countries were left in economic turmoil. Many projects have been considerably disrupted owing to the shutdown of industrial facility chains, disturbance in supply chain analysis, and the unavailability of ample funds among customers.

Energy companies must continually develop production facilities in which complex and injury-prone business processes are automated, and control and decision-making are performed remotely. This requires social sanitation requirements in the current energy economy, which has become more complicated because of the COVID-19 crisis that has added concerns to the global energy crisis.

The substantial decline in smart meter installations in 2020 could be attributed to the economic downturn caused by COVID-19 pandemic. Moreover, the sharp recovery of the market in 2021 is a result of the investment and the economy recovery in many leading countries. In addition, investment in infrastructure increased in 2021 after the decline in 2020. The 2020 drop could be attributed to economic stagnation at the peak time of the COVID-19 pandemic, with post-pandemic investment recovery.

Download Free sample to learn more about this report.

Smart Grid Market Trends

Use of Smart Grid in Decentralization of Energy to Create New Demand for the Product

A decentralized energy system is characterized by placing energy production facilities closer to the place of energy consumption. This system allows optimal use of renewable energy and the combined use of electricity and heat, reduces the use of fossil fuels, and increases eco-efficiency. The distributed energy system is a relatively new approach in most countries' energy industries. Traditionally, energy generation is carried out by the development of large central power plants and the transfer of generation load via long transmission and distribution lines to regional consumers. The goal of distributed energy systems is to bring energy sources closer to the end user. End users are spread across different regions, so providing electricity generation that is properly distributed can reduce transmission and distribution inefficiencies and associated financial and environmental costs.

This type of grid can have millions or even billions of possible connections, from microgrid generators to smart meters. Storing such huge data sets comes with its own set of challenges. Some of them include dependence on Internet-based technology, such as the Internet of Things and smart grid-connected devices that can make power grids prone to hacking and cyber-attacks. This challenge became apparent in May 2021 when the Colonial Pipeline fell into the hands of hackers demanding a ransom, cutting off fuel from half of the U.S. East Coast.

Download Free sample to learn more about this report.

Smart Grid Market Growth Factors

Encouragement By Government To Install Smart Meters Is Boosting The Market Growth

Several governments have made smart meters a central part of national energy policies. Most of them are designed to improve energy efficiency and reduce CO2 emissions. Some governments have required nationwide deployment (e.g., the U.K.). Some governments have also encouraged green technologies, including the introduction of smart meters, in the hope that they will create jobs and offset the global recession. With the support of smart meters, utility companies can reduce the amount of non-technical transmission and distribution losses (T&D) (electricity theft, billing errors, and others). In developing countries, protection offered by the smart meters can be a determining factor for its adoption as the loss of electricity due to theft is high.

On November 14th, 2023, the Biden-Harris administration announced that up to USD 3.9 billion is available for fiscal years 2024 and 2025 through the second round of the Grid Resilience and Innovation Partnerships (GRIP) funding opportunity. Successful projects use federal funding to maximize deployment for grid infrastructure at scale and leverage private sector and non-federal public capital to advance deployment goals.

On October 18th, 2023, the U.S. Department of Energy announced investments of up to USD 3.46 billion in 58 projects in 44 states under the GRIP (Grid Resilience and Innovation Partnerships) program to strengthen the resilience and reliability of the electric grid throughout America. This program includes 34 projects selected through Smart Grid Grants.

Rise Of Renewable Energy Production Promotes The Installation Of Smart Grid Systems

Smart grid infrastructure is essential in the transition to a low-carbon electricity grid that includes intermittent renewable energy production, such as solar, wind, and smaller DER grids. As more governments demand decarbonization of the energy sector, utilities are turning to the product to ensure net-zero targets.

For example, Canada, through the Department of Natural Resources, launched its Renewable Energy and Electrification Pathways (SREP), a four-year, USD 795 million program to support the deployment of smart grid technologies. The aim is to expand its range of renewable energy sources to reduce and modernize carbon dioxide emissions. The program enables the introduction of next-generation and smart goods. Canada's natural resources minister, Seamus O'Regan Jr. commented on the development that the new SREP program will increase the renewable capacity of the country's grid and improve its reliability and sustainability. This means a cleaner and more reliable electricity supply for Canadians. Moreover, Canada's goal is to achieve net zero by 2050.

RESTRAINING FACTORS

High Development Costs And Need For Extensive Worker Training May Hinder the Market Growth

Replacing the existing metering infrastructure is expensive. To date, the most successful deployments have occurred in countries where utilities have survived grid loss and theft (e.g., Italy) and thus benefited from immediate, measurable retrofits and in countries with relatively small and wealthy population (e.g., Sweden). Electric companies face a number of challenges related to consumers' ability to switch suppliers. Power plants that do not have smart meters installed often do not have instructions on how to use advanced meters when a customer changes to a competitor's service. Regulators are stepping up efforts to provide more detailed guidance to electrical retailers. In the U.K., for example, Ofgem considers it acceptable for smart meters to return to mute mode when changing suppliers. Consumers are not even encouraged to install smart meters and smart grid facilities in their residential and commercial premises due to high costs. These factors are expected to hamper the smart grid market growth in the coming years.

Smart Grid Market Segmentation Analysis

By End-user Analysis

Utility Segment to Dominate the Market Owing to Increased Deployment of Grid Technologies During the Forecast Period

Based on end-user, the smart grid market is categorized into utility, industrial, residential, and commercial.

The utility segment is expected to dominate the market during the forecast period due to the global deployment of grid technologies. The utility segment is projected to dominate the market with a share of 48.75% in 2026. In addition, the governments of underdeveloped and emerging countries recognize these technologies as strategic infrastructural investments, which will help achieve the carbon emission targets. The growing population, industrialization, and rising concern over the environment due to fossil power stations push the governments to plan regulatory standards regarding carbon emissions.

Furthermore, the industrial segment is expected to grow significantly during the forecast period due to the government's favorable policies and fiscal incentives. In addition, a rise in the number of electric vehicles positively enhances the growth of this sector.

The residential segment is estimated to grow due to the increase in awareness regarding the benefits of these technologies, including reduced energy consumption and money-saving across various end-users.

The commercial segment is expanding due to the growing demand for uninterrupted, efficient, and reliable electricity sources.

To know how our report can help streamline your business, Speak to Analyst

By Component Analysis

Software Segment to Dominate the Market Driven by the Efforts for the Modernization of Electric Grids

Based on component, the market is classified into software, hardware, and services.

The software segment is expected to dominate the global smart grid market share during the forecast period, owing to the increase in the efforts to modernize the electricity grid and reduce T&D losses. In addition, an increase in investments by the government in advanced metering infrastructure (AMI) is expected to propel global smart grid market growth. For instance, in the U.S., the government passed the Energy Independence and Security Act of 2007 to develop and deploy smart grid technologies. This segment is likely to document a considerable CAGR of 22.41% during the forecast period (2026-2034).

Furthermore, the hardware segment is expected to grow during the forecast period owing to the initiatives taken by the governments of various countries across the globe for the installation of smart electricity meters in their countries. For example, in December 2020, the Australian Energy Market Commission planned to install electricity meters in the country. It launched an independent review of electricity meter rules to discover new opportunities for boosting deployment. The segment is anticipated to hold a dominant market share of 48.75% in 2026.

The services segment provides applications, including installation and integration of various modules of utility smart grid operations. Hence, enterprises opt for these services to smooth the integration and deployment process and reduce costs.

REGIONAL INSIGHTS

The market has been analyzed geographically across five major regions: Asia Pacific, North America, Latin America, Europe, and the Middle East & Africa.

North America

North America Smart Grid Market Size, 2023 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 18.87 billion, contributing 30.91% to global market revenue, and is projected to grow to USD 22.8 billion in 2026. U.S.’s economy, national security, and even the health and safety of citizens depend on a reliable supply of electricity. The U.S. electric grid is a technological marvel, with more than 9,200 electricity generating facilities over a million megawatts of producing capacity connected by more than 600,000 miles of transmission lines. The government is also supporting renewable energy projects with various initiatives and incentives due to the increased environmental concerns. U.S. is highly adopting clean energy which is anticipated to develop demand for smart grid solutions in order to integrate renewable sources with existing power grids. The U.S. market is likely to reach USD 19.13 billion in 2026.

Europe

The Europe market accounted for USD 15.02 billion in 2025, representing 24.61% of the global industry, and is expected to reach USD 18.44 billion in 2026. Europe is the leading region in the upgradation of electricity grid systems to smart grid in many countries, with the help of the European Union investment in the market. According to the EU Agency for the Cooperation of Energy Regulators (ACER) Market Monitoring Report (energy retail and consumer protection volume), 54% of European households had an electricity smart meter at the end of 2021, while in 13 EU countries, the penetration rate was over 80% at the end of 2022. The U.K. market continues to expand, projected to reach a market value of USD 2.92 billion in 2025. The governments in the region are highly focused on implementing solutions that can help in achieving energy efficiency and reliability owing to the obstacles such as energy crisis faced in the region due to effects of Russia-Ukraine War. With correct use of technology such as smart grid, utilities can optimize the distribution network. Thus, this aspect is anticipated to drive the market growth. Germany is estimated to hold USD 3.45 billion in 2025, while France is foreseen to reach USD 1.89 billion in the same year.

Asia Pacific

Asia Pacific recorded a market size of USD 19.29 billion in 2025, capturing 31.60% of the global market share, and is projected to reach USD 24.06 billion in 2026. Home to more than half the world's population and some the fastest-growing economies, the Asia Pacific region plays a central role in the world's energy transition. Smart meters are the first step toward digitizing the grid, which increases the flexibility, efficiency, and sustainability of the network. In addition, several countries in the region have set zero carbon emission targets for 2050-60.

Increasing focus of governments in the region on adopting smart solutions for improving energy usage and distribution is also anticipated to benefit the growth of smart grid market in the region. The Chinese market is expected to reach a valuation of USD 7.7 billion in 2026. The energy demand of region is high and ever growing due to rapid urbanization and industrialization. Here, implementation of smart grid technologies could help the region in maintaining grid stability and reliability. India is likely to be valued at USD 5.22 billion in 2026, while Japan is estimated to gain USD 3.86 billion in the same year.

Latin America

Latin America accounted for USD 2.84 billion in 2025, representing 4.65% of the global market share, and is projected to reach USD 3.37 billion in 2026. Due to its size and rapid growth, Latin America is an important emerging market for these solutions. The region has a common need to improve technical and commercial energy losses and enhance service reliability and quality. This will help create these products and take advanced metering infrastructure and grid automation technologies to the spotlight.

Middle East & Africa

The Middle East & Africa market generated USD 5.03 billion in 2025, representing 8.24% of the global market landscape, and is expected to reach USD 6.05 billion in 2026. The Middle East & Africa is estimated to grow notably in the coming years owing to the rising construction of smart cities in the countries such as the UAE and Saudi Arabia. Additionally, the GCC countries in the region are highly inclined towards accelerating digital economy and adopting smart technologies, which is expected to have a positive impact on the market. The GCC market is projected to hit USD 2.61 billion in 2025.

KEY INDUSTRY PLAYERS

Siemens is Expanding its Grid infrastructure to Fortify its Market Position

Redesigning the electricity grid is necessary to meet the growing energy demands. Several government regulations and policies across developing countries positively enhance the expansion of grid infrastructure. In addition, to increase transmission capacity, a qualitative grid expansion is essential to deliver efficient and intelligent operations as compared to the existing infrastructure. As the growing investment in renewable energy capacity needs to be matched with the equivalent investment in grid capacity expansion, the industry participants emphasize expanding their grid infrastructure to enhance customer reach.

Siemens, a technology company focused on industry, infrastructure, transport, and healthcare, is one of the largest industrial manufacturing companies in Europe. In April 2021, the German multinational conglomerate announced the first high-voltage direct current (HVDC) link featuring voltage-sourced converter (VSC) technology in India. The 2,000 megawatts (MW) electricity transmission system consists of two links, Thrissur in Kerala and Pugalur in Tamil Nadu, supporting the Power Grid Corporation of India Ltd.

List of Top Smart Grid Companies:

- ABB (Switzerland)

- Siemens (Germany)

- Schneider Electric (France)

- S&C Electric Company (U.S.)

- Eaton (Ireland)

- GE (U.S.)

- IBM (U.S.)

- Wipro Limited (India)

- Honeywell (U.S.)

- Cisco (U.S.)

- Aclara (U.S.)

- Landis+Gyr (Switzerland)

- Oracle (U.S.)

- Itron (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In October 2023, Prolec and Ubicquia have collaborated to create and market a new fully integrated smart transformer. This transformer integrates Ubicquia's UbiGrid platform for real-time monitoring and grid analytics into Prolec's single-phase pad mount transformers. Units are now being shipped to North American utilities for field trials after testing and certification at Prolec's facility in Monterrey, Mexico.

- In June 2023, Siemens presented its newly developed software for low-voltage networks. The LV Insights X software, part of the Siemens Xcelerator portfolio, enables distribution network operators (DSOs) to address their most pressing challenge: the need to significantly increase grid capacity even when grids are already strained by rapid growth in the distribution renewable energy input and additional consumers such as electric car chargers or heat pumps.

- In March 2023, Oregon utility Portland General Electric announced that it is testing Utilidata's recently announced artificial intelligence distributed smart grid platform. A smart grid based on the NVIDIA Jetson platform is proposed to be deployed with electricity meters that integrate distributed energy resources (DERs), including solar, battery storage, and electric vehicles (EVs).

- In March 2023, for a recent development project, Eaton unveiled that it is using its data center as a Grid approach to reimagine the role of the data center as an active player in the energy transition, making critical infrastructure work in new ways to create new revenue streams, improve flexibility, and reduce carbon emissions. This application is a key part of Eaton's "Everything as a Network" approach, which helps transform existing systems and enables data centers to work harder, smarter, and more sustainably.

- In January 2023, ABB invested in Danish start-up OKTO GRID to advance the development of technology for the digitization and extension of the life of aging electrical equipment to meet the growing demand for reliable and stable power generation. OKTO GRID has developed a pilot solution that digitizes the electrical infrastructure and enables real-time remote monitoring of conditions and performance to extend their service life by another 40 years. As part of the collaboration, ABB brings its electrification, digitalization, and industrial expertise to enhance the development of the OKTO GRID solution and accelerate technology and commercial readiness.

REPORT COVERAGE

The market research report offers an in-depth analysis of the industry. It further provides details on the adoption of these technologies across several regions. Information on the growth of the market trends, drivers, opportunities, threats, and restraints of the market can further help stakeholders gain valuable insights into the market. The report offers a detailed competitive landscape by presenting information on key players, along with their strategies in the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 16.04% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By End-User

|

|

By Component

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 61.05 billion in 2025 and is projected to reach USD 245.60 billion by 2034 with a growth rate of about 16.04%.

In 2025, the region stood at USD 18.87 billion.

Registering a CAGR of 16.04%, the market is expected to exhibit staggering growth during the forecast period.

The utility segment is projected to dominate the market during the forecast period.

Improved grid reliability, efficient outage response, growing demand for integration of renewable energy sources, and supportive government initiatives and regulations are some of the major factors driving the market growth.

ABB, Siemens, Schneider Electric, S&C Electric Company, and Eaton are among the key players operating across the industry.

The high investment cost associated with the setup of new advanced grid systems is expected to restrict the market growth during the forecast period.

North America dominated the smart grid market with a market share of 30.91% in 2025.

Several governments across the globe are progressively investing in these technologies as it is expected to help them achieve their carbon emission reduction targets and enable long-term economic prosperity.

- 2021-2034

- 2025

- 2021-2024

- 253

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us