Unmanned Aerial Vehicle (UAV) Market Size, Share, Industry Analysis and Russia-Ukraine War Impact Analysis, By UAV Class (Micro, Mini, & Small UAVs, and Tactical UAVs), By Operational Mode (Fully & Semi-Autonomous, Remotely-Operated), By Fully Autonomous (Individual Autonomous System & Drone-in-a-Box), By Solution (Aerostructures & Mechanism, Securing System, Operating Software, Tethering Cord), By Application (Perimeter Security & Border Management, Combat & Combat Support Missions), By End-User (Government & Defense, Energy, Power, Oil & Gas), Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

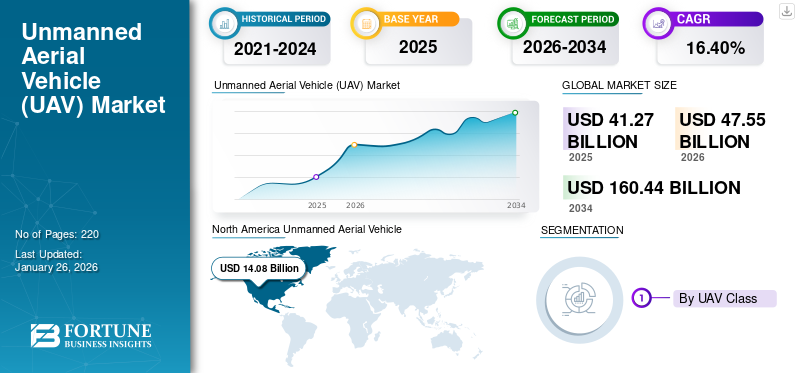

The global Unmanned Aerial Vehicle (UAV) market size was valued at USD 41.27 billion in 2025. The market is projected to grow from USD 47.55 billion in 2026 to USD 160.44 billion by 2034, exhibiting a CAGR of 16.40% during the forecast period. North America dominated the unmanned aerial vehicle market with a market share of 34.12% in 2025.

The important parts of the UAV, commonly known as drones, are the onboard computers controlled remotely by ground-based controllers. UAVs have aerodynamic structures designed to carry out several functions with the appropriate navigation system. The technology was initially developed for high-risk military missions to eliminate the potential for human casualties in various military applications. Military UAVs are equipped with missiles to hit specific targets that are operated at high altitudes. Military-operated UAVs have modified propulsion systems that use liquid hydrogen fuel for long-range operations against enemy troops.

Consumer drones are mainly used in cinematography, surveys, and aerial mapping. However, the use of consumer drones has rapidly grown in numerous applications, such as business, science, recreation, and other services. Giant companies such as Google, Amazon, DHL, Uber, Boeing, and Airbus have invested in research and development in this technology for the past few years due to lucrative opportunities in this market.

Key market participants are concentrating on the development of sophisticated UAVs (Drones) that can perform a variety of operations across different industries. Notable companies in the UAV sector include General Atomics Aeronautical Systems (GA-ASI) from the U.S., Teledyne FLIR LLC from the U.S., Northrop Grumman Corporation from the U.S., EHang from China, Parrot from France, SZ DJI Technology Co., Ltd from China, Israel Aerospace Industries Ltd. (IAI) from Israel, AeroVironment, Inc. from the U.S., and Lockheed Martin Corporation from the U.S., among others.

The COVID-19 pandemic in 2020 postively impacted the market growth. Despite social distancing norms and other restrictions in effect, this industry managed to stay afloat during the pandemic. With the travel bans in effect, autonomous UAVs, or drones, were used for door-to-door delivery of essential supplies, such as groceries, medicines, and others. Many countries, such as the U.S., the U.K., Singapore, China, Ghana, Chile, and others, used drones to deliver such items. Many unmanned aerial vehicle and drone operators capitalized on the opportunity and expanded into newer regions.

Unmanned Aerial Vehicle (UAV) Market Snapshot & Highlights

Market Size & Forecast

- 2025 Market Size: USD 41.26 billion

- 2026 Market Size: USD 47.55 billion

- 2034 Forecast Market Size: USD 160.44 billion

- CAGR: 16.40% from 2026–2034

Market Share

- North America dominated the UAV market with a 34.12% share in 2025, driven by high defense budgets, widespread adoption of drone technology for surveillance and logistics, and the presence of major players like General Atomics, Northrop Grumman, and Teledyne FLIR. The region continues to lead innovation in tactical UAVs, autonomous systems, and drone-in-a-box (DiaB) technology.

- By UAV class, tactical UAVs (MALE & HALE) are witnessing the fastest growth due to their applications in ISR (Intelligence, Surveillance, Reconnaissance) and combat missions.

Key Country Highlights

- North America (U.S., Canada): Largest market driven by defense applications, drone deliveries (Walmart, Amazon), and homeland security initiatives.

- Asia Pacific (China, India, Japan): Fastest-growing region due to heavy adoption in commercial sectors (agriculture, logistics) and government-led defense programs.

- Europe (France, Germany, U.K.): Focus on R&D and urban mobility drone technologies; strong presence of Parrot and Terra Drone.

- Middle East & Africa: Rising UAV use in defense and oil & gas sectors; countries like Turkey and Israel exporting drones widely.

- Latin America: Growing adoption for border security, agriculture, and law enforcement, with increasing U.S. collaboration.

RUSSIA-UKRAINE WAR IMPACT

Unmanned Aerial Vehicle Demand has Risen Globally Due to Russia-Ukraine War

The Russia-Ukraine War started in early 2022 and has been going on for more than a year now. The war has witnessed extensive military investments from both sides and has been heavily sided toward electronic equipment than pure gun firepower. This electronic nature of the war has experienced a growing deployment of drones and UAVs on the battlefield. UAVs provide enhanced situational awareness, owing to their capability of intelligence, surveillance, reconnaissance (ISR), and communication. Both the countries involved have been increasing their usage of drones in order to increase their offense while guaranteeing the safety of their personnel.

- For instance, in June 2023, a report published by the Royal United Services Institute (RUSI), a British firm specializing in defence issues, stated that the Ukrainian army was losing over 10,000 drones a month, or over 300 drones, in a single day.

Not only in the Russia and Ukraine but the demand for drones has been created outside Europe as well. The influx of military supplies to Ukraine from N.A.T.O. nations, such as the U.S. and U.K., has increased the production of drones in these countries. In the Middle East, countries such as Iran and Turkey have been providing drones that are being used in day-to-day activities on the battlefield.

Turkey provided Ukraine with the Bayraktar TB-2 drones manufactured by Turkish firm Baykar. These drones have been consistently used for their stealth, surveillance, and reconnaissance capabilities, in addition to their favorable attributes such as low-cost and long-endurance flight capability. Russia has also been using Chinese DJI drones for surveillance and reconnaissance. These instances create demand outside the areas of war as well.

- For instance, in March 2023, a third-party data provider released official Russian customs data, which indicated that the Chinese government had supplied drones worth more than USD 12 million to Russia since the start of the war. The shipments contained a mix of DJI drones and an array of smaller companies.

Such an increased supply of drones has also boosted the research and development of the technology. Drones and UAVs, which were earlier very expensive and sophisticated to manufacture, are now being produced in masses. The war has solidified the need for simple, efficient, and cost-effective drones that can be manufactured rapidly to replenish depleting stocks, thereby propelling the market during the forecast period.

UNMANNED AERIAL VEHICLE (UAV) MARKET TRENDS

Emergence of Drone-in-a-Box (DiaB) Technology and Commercial Applications of Drones to Accentuate Market Growth

The Drone-in-a-Box (DiaB) technology includes a drone with the capability to fly and return from a point and start self-charging upon return from the mission. This has many use cases in a wide range of industries, as it minimizes the need for human intervention. The technology has found applications in industries such as telecom, maritime, space, and others. In the telecom industry, drone-in-a-box technology can be used to provide a faster and more efficient network of communication.

- North America witnessed Unmanned Aerial Vehicle (UAV) market growth from USD 10.97 Billion in 2023 to USD 12.51 Billion in 2024.

- For instance, in May 2023, Nokia announced that the firm had signed a deal with Belgium-based telecom operator Citymesh for the supply of 70 drone-in-a-box units. These units will be used to cover Belgium with a 5G automated drone grid, which will help speed up resource mobilizations in emergency events.

Furthermore, this technology can be used in agriculture as well. Drones fitted with various sensors and cameras can be used for monitoring crop health and managing crop growth. The increasing use of these systems in construction, mapping, agriculture, and other applications creates significant opportunities for drone solutions. The rise in demand for advanced and autonomous drones in commercial industries is driving the global Unmanned Aerial Vehicle (UAV) market.

- For instance, in 2021, Poland's autonomous drone startup, Dronehub, announced to work with Europe's property monitoring company RSCR Engineering to develop a security system, especially for detecting drones and surveillance technology. Further, the new RCS breach detection software integration will make autonomous drones available to respond to any invasion incidents and reduce human security costs.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Procurement of Drones in the Military Sector to Boost Market Growth

Military warfare today is shifting from the conventional notion that better firepower provides an edge on the battlefield to which side has the better Intelligence, Surveillance, and Reconnaissance (ISR) capabilities. This phase of electronic warfare has created a huge demand for using UAVs in the military sector.

UAVs do not need a crew onboard for flight and can be autonomous or remotely controlled by human personnel from a safe distance. Aside from ISR, UAVs are also employed for offenses. UAVs as big as small aircraft can carry missiles into the battlefield, while autonomous UAVs, also called drones, can be the size of a bird's wingspan and are used for kamikaze warfare. Such capabilities make drones a must-have for any military, allowing for major push-back to the enemy from the safety of the ground stations.

- For instance, in April 2023, the Romanian government signed a deal worth USD 321 million with Turkey to procure 18 Turkish Bayraktar B2 drones. These drones provide enhanced intelligence and offensive capabilities.

The ongoing Russia-Ukraine war has projected the capability and reliability of UAVs to the world. Both sides have been stockpiling drones, hoping to get an advantage on the ground over the enemy. Ukraine has primarily been outsourcing drones from the U.S. and Turkey. The Turkish Bayraktar B2 drone has been extensively used in Ukraine’s counter-offensives, while U.S.-provided kamikaze drones have proved capable of flushing out soldiers from dangerous areas.

On the other hand, Russia has started importing kamikaze drones from Iran, adding them to its arsenal of indigenous drones. Both nations have also used commercial drones such as the Chinese-made DJI Mavic drones. Such extensive use of drones has created demand in Europe, North America, and Asia Pacific. The increasing complexity of electronic warfare also favors the advancements in unmanned aerial vehicle technology.

- For instance, in March 2023, Ukraine announced that it procured over 300 DJI Mavic 3T UAVs and sent them on the front lines. These UAVs’ thermal and zoom capabilities make them ideal for gathering intelligence on ground zero.

Growing Demand for UAVs to Support Commercial Applications to Drive Market Growth

UAVs and drones are rapidly being deployed in commercial applications. Many organizations see drones as an economical and more efficient mode for product delivery. Drones avoid traffic on the road and, thus, provide faster delivery. Drone flying is gaining popularity as a leisure activity in many countries.

Drones with high-quality cameras and axis stabilization are used in the film-making and videography industries. These allow for aerial shots, which would not have been possible, with great ease and accuracy. Drones can also be used in the healthcare industry for delivering medicines, carrying test samples, and many other activities. Many countries have started implementing drones in the healthcare industry.

- For instance, in June 2023, commercial unmanned aerial vehicle and drone operator Zipline celebrated its 4th year of operating in Ghana. Zipline has revolutionized the medical distribution centers of the country, delivering more than 370,000 medical supplies to people in different areas of the country. The operation proved useful in improving the lives of the people of Ghana, as UAVs were able to deliver goods even in the most remote parts of the country.

Furthermore, UAVs can be used for remote sensing and Earth observation operations. UAVs can be built to fly at high altitudes and, when equipped with sensors, can provide climatic and other information about a large area. They can provide insights about undiscovered areas, including potential stores for new ores and mines. They can even be used for site inspections in many industries, such as oil, energy, solar, and others. UAVs and drones can also be used in agriculture to manage crop growth and monitor crop health.

- For instance, in October 2022, Bayer, a global healthcare and agriculture enterprise, announced that it had started using drones in agriculture. Drone services are to be provided for crop protection across a wide range of crops in a phased manner.

MARKET RESTRAINTS

Stringent Government Rules and Regulations for UAVs to Hamper Market Growth

The usage of UAVs and drones differs in different nations. Each region has its policy on the commercial and military applications of UAVs. Unregulated usage of these poses a risk to national security. Countries have applied regulations to the weight of the UAV, the height up to which it can fly, the regions where unmanned aerial vehicle or drone flight is allowed, and many more.

Manufacturers also need to make their products according to these regulations and adhere to different guidelines laid for the production of drones. This development limits the number of UAVs eligible for commercial usage. UAVs must remain in the Visual Line-of-Sight (VLOS) of the operator, and the operator needs to have a license in many countries to fly the product.

- For instance, in June 2023, the Chinese government issued the Interim Regulation for Managing Uncrewed Aerial Flights. The rules include registering drones of all sizes and activities, such as using drones for surveying land or being labeled as punishable offenses for a non-Chinese drone pilot.

Growing geopolitical tensions globally also add to the deceleration of unmanned aerial vehicle (UAV) market growth. Most UAVs and drones used commercially are fitted with cameras, making them vulnerable to cyber-attacks. These features also raise the suspicion of snooping through the network, which further poses a risk to national security. Following these reasons, many countries have started restricting products from a specific manufacturer to a country, slowing down market growth.

- For instance, in May 2023, two U.S. states banned using Chinese firm DJI’s drones for any activity. The move comes after the U.S. Department of Defense and other agencies blacklisted the company on suspicion of suspected data leaks through the network of drones.

MARKET CHALLENGES

Technological limitations, Public Perception, and Ethical Considerations are Challenging the Market Growth

The UAV market, while experiencing significant growth, faces a complex web of challenges. Regulatory hurdles remain a major constraint. Varying regulations across regions, slow implementation, and the need for comprehensive frameworks addressing airspace management, safety protocols, and privacy concerns impede widespread adoption, particularly in commercial applications.

Technological limitations also pose a significant obstacle. Battery life remains a critical issue, restricting flight duration and operational range. Developing more efficient and reliable power sources is crucial. Moreover, ensuring robust and secure communication links, especially in challenging environments, is paramount to maintaining operational control and preventing unauthorized access.

Public perception and ethical considerations are increasingly important. Concerns surrounding privacy, security, and the potential for misuse fuel public apprehension. Addressing these concerns through transparent operational practices, robust data security measures and clear ethical guidelines is essential for building public trust and acceptance.

Additionally, competition and commoditization are impacting profitability. The influx of lower-cost drones is putting pressure on manufacturers to innovate and differentiate their products. Developing specialized capabilities and focusing on niche applications will be crucial for sustained success in an increasingly competitive market. Overcoming these challenges is vital for realizing the full potential of the UAV market.

MARKET OPPORTUNITIES

Advancements in Technology, Decreasing Costs, and Expanding Applications Has Created Ample Amount of Opportunities in the Market

The Unmanned Aerial Vehicle (UAV) or drone market is experiencing a period of rapid growth and diversification, presenting a significant and multifaceted opportunity for businesses and investors. Fueled by advancements in technology, decreasing costs, and expanding applications, the global UAV market is projected to reach staggering figures in the coming years. This is not just a niche market but it is a transformative technology impacting various sectors, creating a wealth of opportunities for innovation and profit.

The core opportunity lies in the diverse range of applications. Beyond the consumer drone market focused on recreational use and aerial photography, the commercial segment is rapidly expanding. Industries such as agriculture utilize UAVs for crop monitoring, precision spraying, and yield optimization. Infrastructure inspection companies employ drones to assess bridges, power lines, and pipelines, increasing safety and reducing costs. Logistics companies are exploring drone delivery for faster and more efficient last-mile services. Furthermore, security and surveillance agencies are leveraging UAVs for enhanced monitoring and border control.

This broad applicability translates to several key avenues for businesses to explore. Firstly, manufacturing and hardware development remain crucial. Focus areas include developing more robust, longer-lasting, and specialized UAVs tailored to specific industry needs. This extends to the development of advanced sensors, payloads, and communication systems that enhance drone capabilities.

Secondly, software and data analytics represent a significant growth area. The vast amounts of data collected by UAVs require sophisticated software platforms for processing, analysis, and actionable insights. This includes developing algorithms for image recognition, predictive maintenance, and autonomous navigation.

SEGMENTATION ANALYSIS

By UAV Class

Increased Demand for Tactical UAVs (MALE & HALE) for Defense and Law Enforcement Applications to Aid Segment Growth

By UAV class, the market is segmented into micro UAVs (below 2 Kg), mini UAVs (2-20 Kg), small UAVs (20-50 Kg), and tactical UAVs (MALE & HALE).

Tactical UAVs (Medium Altitude Long Endurance (MALE) and High Altitude Long Endurance (HALE)) is expected to be the fastest-growing segment during the forecast period. They provide real-time data and visuals outside the enemy’s front lines without compromising a soldier’s life. In tactical UAVs, Live Electro-Optical and Infrared (LEO/IR) videos are used. Growing demand for tactical UAVs by major countries, such as China, India, Japan, and Australia, is projected to boost market growth.

- The small UAVs (20-50 Kg) segment is expected to hold a 43.51% share in 2026.

- For instance, in December 2022, Elbit Systems Ltd. awarded a framework contract worth up to USD 410 million for supplying up to seven ‘Watchkeeper X’ tactical unmanned aircraft systems to the Ministry of National Defense for five years.

To know how our report can help streamline your business, Speak to Analyst

By Operational Mode

Remotely-Operated Segment Dominated due to Increased Popularity of Drone Technology in Several Applications

By operational mode, the market is classified into fully autonomous, semi-autonomous, and remotely-operated.

The remotely-operated segment dominated the market share of 57.07% in 2026. A UAV does not have a crew or passengers on board. UAVs can be automated ‘drones’ or Remotely Piloted Vehicles (RPVs). UAVs can fly for extended flight time at low altitudes. The demand for remotely operated UAVs has increased in many countries in recent years due to the growing popularity of drone technology and its various applications.

- For instance, in July 2023, India announced to procure 31 MQ-9B RPAS of approximately USD 3.07 billion through the U.S. government’s FOREIGN MILITARY SALES (FMS) program, which will enhance Indian Armed Forces’ intelligence, surveillance, and reconnaissance capabilities.

Fully autonomous is anticipated to be the fastest-growing segment during the forecast period of 2025-2032. It includes the Command Delivery System (CDS) and the Flight Planning System (FPS), where the flight path and radius are determined before the operation. The unmanned aerial vehicle has complete control without any external guidance from the operator on the ground. Mission Based High Payload UAVs (MBHPPs) are UAVs that are specially designed for specific missions in the U.S., China, Russia, and Israel.

- For instance, in May 2023, SSCI awarded a multi-million dollar, five-year prime contract to the U.S. Army Combat Capability Development Command (DEVCOM) C5ISR Center for the development, demonstration and fielding of autonomous UAVs.

By Fully Autonomous

Individual Autonomous System Segment Leads Owing to its High Demand

By fully autonomous, the market is classified into individual autonomous system and Drone-in-a-Box (DiaB).

The individual autonomous system segment dominated the market share of 22.87% in 2026. The system is controlled by software and requires a complete system to operate. Due to the self-ability of performing tasks and missions, the demand for individual autonomous systems is high.

- For instance, in May 2023, Near Earth Autonomy announced that the US Air Force's AFWERX program selected Near Earth to work on a Reliability Standard for Autonomous Aerial Transport as part of Autonomy Prime. This collaboration highlights Near Earth's commitment to driving autonomous aircraft development to new heights.

Drone-in-a-Box (DiaB) is anticipated to exhibit the fastest growth during the forecast period. The drone-in-a-box supports the operation of a facility by capturing aerial images and providing real-time information to users. Designed tasks can help detect human/vehicle activity, alert facility users to gas/water leaks, and monitor other maintenance issues.

- For instance, in February 2023, DroneMatrix and Infrabel entered a nine-year framework contract. The contract comprises four years of supply and nine years of service for procuring drone-in-a-box solutions. The client will use the drone-in-a-box solution for automated video monitoring of rail vehicle processing at Antwerp port and other areas of Belgium.

By Solution

Aerostructures & Mechanism Segment Led the Market Due to Technological Advancements

By solution, the market is classified into aerostructures & mechanisms, securing system, operating software, tethering cord, power sources & management system, payload, propulsion systems, and others.

The aerostructures & mechanism segment held the maximum share in 2024. Companies with high technical skills are expected to make significant technological advancements in the aerostructures & mechanisms of UAVs, leading to a good development cycle and significantly improving the performance of UAVs.

- For instance, in June 2023, General Atomics made a drone deal worth USD 3 billion with India. India had asked for an increase in the content of the U.S.-built MQ9B drones to be produced in India.

Securing system is projected to be the fastest-growing segment during the forecast period. Since a UAV’s payload, range, and endurance are at the top of OEMs’ and operators’ to-do lists, the advent of cyber-attacks on UAVs is expected to change the competitive landscape significantly. To cater to this problem, securing systems plays a vital role so that their demand will be high during the forecast period.

By Application

Combat and Combat Support Missions Segment Leads Due to UAVs Ability to Perform Tasks Smoothly at Hardpoints

By application, the market is classified into perimeter security & border management, combat and combat support missions, situational awareness, disaster management & first responders, surveying, mapping, & monitoring, precision agricultural management, power station management, asset & operations management, emergency medical logistics, and others.

The combat and combat support missions segment dominated the global market in 2024. These UAVs carry aircraft ordnance (missiles, antitank guided missiles (ATGMs), or bombs) at hardpoints to carry out drone strikes. Combat UAVs are typically operated in real-time under human control and have varying degrees of autonomy.

- For instance, in April 2023, the Romanian Defense Ministry awarded a TB2 drone contract worth USD 321 million to Turkish firm Baykar.

Emergency medical logistics is estimated to be the fastest-growing segment during the forecast period. It is the most promising application in drone services, where a quick response is essential to improve patient care. Medical drones became increasingly popular around the world during the pandemic. Drones were used to deliver PPE (personal protective equipment), COVID-19 tests (SARS CoV-2), laboratory specimens, and vaccines, where direct human-to-human contact was discouraged for infection control purposes.

- For instance, in January 2022, the German drone delivery leader Wingcopter and Spright announced a new commercial arrangement valued at over USD 16 million. As part of the agreement, Spright will purchase a large fleet of the new Wingcopter flagship delivery drone Wingcopter 198 to meet the growing demand for medical drone solutions nationwide.

By End-User

Government & Defense Segment Dominated Owing to Several Applications of Drones in Military Sector

By end-user, the market is classified into government & defense, energy, power, oil & gas, construction & mining, agriculture, forestry & wild life conservation, public infrastructure & homeland security, hospitals & emergency medical services, transportation & logistics, event management, and others.

The government & defense segment dominated the market in 2024. Military UAVs will continue to be in high demand due to the increasing use of UAVs by the defense and security community for various purposes, including survey, mapping, transport, combat, and monitoring.

- For instance, in January 2022, The US Navy and Boeing demonstrated air-to-air refueling operations using an Unmanned Aerial Vehicle, Boeing's proprietary MQ-25 T1 test vehicle, to refuel other aircraft. It is paving the way for future integration of UAVs for refueling in military operations.

Hospitals & emergency medical services is expected to be the fastest-growing segment during the forecast period. The pandemic prompted governments and OEMs to adopt UAVs for medical applications and emergencies, which has driven the market growth. Hence, many countries started experimenting and testing the efficiency of UAVs.

- For instance, in 2021, the FAA registered about 900,000 drones that may be deployed for various applications. For example, in May 2021, India started expanded testing of drones for the delivery of vaccines and medicinal products to BVLOS destinations.

UNMANNED AERIAL VEHICLE (UAV) MARKET REGIONAL OUTLOOK

This Unmanned Aerial Vehicle (UAV) market is segmented into North America, Europe, Asia Pacific, the Middle East, Africa, and Latin America.

North America

North America Unmanned Aerial Vehicle (UAV) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market with a valuation of USD 14.08 billion in 2025 and USD 16.1 billion in 2026. The region is expected to hold the largest unmanned aerial vehicle market share as most UAV developers are based in the region. This growth is attributed to an increase in the Air Force defense budget, which has increased the demand for fixed-wing UAVs in the U.S. In addition, increasing Canadian exports and economic development are expected to drive market growth. The U.S. market is projected to reach USD 15.47 billion by 2026.

- For instance, in May 2022, Walmart announced the expansion plans of its drone delivery service to approximately four million prospective customers. In making the announcement, Walmart said it would expand its current drone delivery service to 34 locations across Arizona, Arkansas, Florida, Texas, Utah, and Virginia, enabling it to transport over a million orders annually. The drone service will always be available, costing USD 3.99 per package (up to 10 lbs).

Asia Pacific

Asia Pacific is anticipated to be the fastest-growing region during the projection period. This growth is attributed to the high adoption rate of heavy-duty UAVs in China's commercial and defense sectors, including combat, cargo, and other applications. Increased UAV activity in India is expected to boost market growth. The Japan market is projected to reach USD 2.01 billion by 2026, the China market is projected to reach USD 5 billion by 2026, and the India market is projected to reach USD 3.07 billion by 2026.

- For instance, in December 2022, India demonstrated a new drone hunting capability with high-resolution cameras and a highly trained black kite. The new capability is intended to enhance surveillance along India’s border with China. In addition, the drone named FX798T micro FPV camera and 5.8 GHz 40CH 25mw VTX is small and is developed in China.

Europe

The European market is highly segmented, with several players dominating the market. Some leading European market players are Azure Drones SAS, Parrot Drones, Terra Drone, Onyx Scan advanced LiDAR Systems, and AltiGator unmanned Solutions. Drone manufacturers invest heavily in improving technology and adding new features to support commercial applications. The UK market is projected to reach USD 2.43 billion by 2026, and the Germany market is projected to reach USD 1.76 billion by 2026.

- For instance, in June 2021, a European drone manufacturer, Parrot, launched its drone, ANAFI Ai. This is the first drone that uses the connectivity of ANAFI Ai as the primary data link between the drone and the operator to provide accurate control at any distance.

Middle East

The market in the Middle East is highly fragmented, with the presence of players such as SZ DJI Technology Company Co. Ltd, Parrot SA, AeroVironment Inc., BlueBird Aero Systems Ltd., and Terra Drone Corporation. The collaboration between the manufacturers and the UAV solutions companies mainly drives the technology development of the market. To increase their revenue, the UAV service providers are adapting their solution portfolio (technologically advanced UAVs) to meet the specific needs of the end-users in the region, including construction, infrastructure management, and security and surveillance.

- For instance, in February 2022, in the Middle East, UVL Robotics launched the first parcel delivery drone in the region for daily parcel service. Flying couriers can carry a payload of 6.6 pounds, and delivery drones can fly more than 25 miles.

Africa

In Africa, UAVs are increasingly used and deployed in different regions for applications such as post-delivery and agriculture. Agriculture in Africa has the highest market demand for soil scanning UAVs for monitoring nitrogen content, electrical conductivity, crop monitoring, spraying pesticides, pests, weeds, disease detection, and fish population monitoring.

- For instance, in January 2022, Morocco and Israel are preparing to build several factories specialized in manufacturing drones. Specifically, two drone farms are being built in the Northern part of Al-Aoula on the territory of the Kingdom. The project is implemented by Bluebird Aero System.

Latin America

Latin America holds a small UAV market. However, the region has significant growth potential. The U.S. is influencing the military procurement of countries such as Colombia and Mexico through many bilateral initiatives, including Plan Colombia and the Merida Initiative. These initiatives will attract more contracts to U.S.-based companies in Latin America over the coming years. Local manufacturers can compete with major foreign players by modernizing their products with cutting-edge technologies, thus increasing their regional presence.

- For instance, in April 2022, The Ministry of Defense (MoD) deployed 20 small UAVs and military drones in the Arauca department to protect the civilian population, military installations, and the fight against armed criminal groups.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Development of Advance Technology by Key Market Players to Propel Market Growth

The Unmanned Aerial Vehicle (UAV) market is highly fragmented due to the presence of numerous manufacturing companies. The key market leaders have a robust product portfolio and extensive distribution networks in developed and developing countries. Currently, the leading players in the market are DJI (China), Parrot (Switzerland), and Yuneec (China). These companies accounted for a majority of the global market share in 2022. However, due to the absence of stringent entry barriers, the number of domestic players in the global market is expected to grow. The other key players include AeroVironment (U.S.), Autel Robotics (U.S.), and Boeing Company (U.S.). Some key strategies adopted by the players are introducing innovative product ranges, wide variety and size acquisition, collaboration, and partnerships.

LIST OF KEY COMPANIES PROFILED

- AeroVironment, Inc. (U.S.)

- Autel Robotics (U.S.)

- Parrot Drone S.A.S. (Switzerland)

- Yuneec (China)

- BAE Systems PLC (U.K.)

- Boeing (U.S.)

- Elbit Systems Ltd. (Israel)

- General Atomics Aeronautical Systems (U.S.)

- Hexagon AB (Sweden)

- Israel Aerospace Industries (Israel)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- SZ DJI Technology Co. Ltd. (China)

- Teledyne Technologies Inc. (U.S.)

- Textron Systems Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2025 - The Indian tech firm Tata Elxsi and CSIR-National Aerospace Laboratories (CSIR-NAL) have entered into a Memorandum of Understanding (MoU) to establish a strategic partnership focusing on Advanced Air Mobility.

- January 2025 - Acquisition, Technology & Logistics Agency (ATLA) signed a contract with Boeing Japan Co., Ltd. for the research and development of Unmanned Aerial Vehicles (UAV) designed for combat in partnership with manned aircraft.

- July 2024 - Thales entered into a Memorandum of Understanding (MoU) with Garuda Aerospace to encourage development and innovation in the drone industry in India. As per the agreement, Thales will offer expertise in Unmanned Traffic Management (UTM) solutions, UAV detection, and system integration, while Garuda will contribute its capabilities in UAV manufacturing and utilization, as well as its experience in the Indian market. The MoU seeks to establish a foundation for strategic cooperation in the development of the drone ecosystem in India.

- July 2023 - IoTechWorld Avigation Pvt Ltd, a leading agri-drone manufacturer, declared that it won a large contract from IFFCO, a cooperative major, to supply 500 drones for the spraying of nano liquid urea and DAP.

- June 2023 - The U.S. Department of Defense awarded a contract to AeroVironment to develop its high-altitude solar-powered UAV. AeroVironment plans to deploy a network of high-altitude, long-range UAVs to support global internet connectivity. The fixed-wing aircraft is expected to fly at an altitude of approximately 65,000 ft, or 19,812 m, and will carry sensors.

REPORT COVERAGE

The Unmanned Aerial Vehicle (UAV) research report provides an in-depth analysis of this market by identifying the leading companies, product types, and the leading applications in the market. It also provides market trends and key developments in this industry. In addition to the abovementioned factors, it includes several factors that contributed to the advanced market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 16.40% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By UAV Class

|

|

By Operational Mode

|

|

|

By Fully Autonomous

|

|

|

By Solution

|

|

|

By Application

|

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 47.55 billion in 2026 and is estimated to record a valuation of USD 160.44 billion by 2034.

The market will grow steadily at a CAGR of 16.40% during the projection period.

By UAV class, the tactical UAVs (MALE & HALE) segment is expected to grow at a fastest rate.

SZ DJI Technology Co. Ltd., Elbit Systems Ltd., General Atomics Aeronautical Systems, and AeroVironment Inc. are some of the leading OEMs in the market.

North America dominated the unmanned aerial vehicle market with a market share of 34.12% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

-

(Offer valid till 28th Feb 2026)

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us