Welding Market Size, Share & Industry Analysis, By Product Type (Equipment and Consumables), By Welding Type (Arc, Resistance, Oxy-Acetylene Gas, Solid State, and Others (Electron Beam)), By Application (Automotive, Building & Construction, Heavy Engineering, Railway & Shipbuilding, Oil & Gas, and Others (Aerospace)), and Regional Forecast, 2026-2034

Welding Market

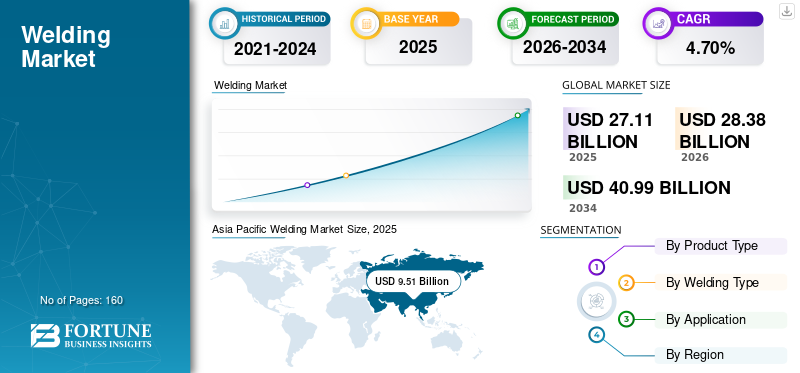

The global welding market size was valued at USD 27.11 billion in 2025 and is estimated to increase from USD 28.38 billion in 2026 to USD 40.99 billion by 2034, demonstrating a CAGR of 4.70% between 2026-2034. The welding market in the U.S. is projected to grow significantly, reaching an estimated value of USD 8.95 billion by 2032, driven by the extensive installation Of pipelines to improve energy infrastructure across regions. Asia Pacific dominated the welding market with a market share of 35.10% in 2025.

The welding industry has witnessed significant technological advancements in recent years, including the development of new techniques and equipment such as robotic and laser welding. It is one of the most crucial sectors of the manufacturing and construction industries. Moreover, increased demand from various industries, such as automotive, heavy engineering, and construction, has led to the growth of the industry. However, in recent times, there has been a shortage of skilled welders across the globe.

As the global population continues to grow and construction activities increase, the demand for fabrication is anticipated to remain strong over the forecast period.

Download Free sample to learn more about this report.

Global Welding Market Overview

Market Size & Share:

- 2025 Market Value: USD 27.11 billion

- 2026 Estimate: USD 28.38 billion

- 2034 Forecast: USD 40.99 billion

- CAGR (2026–2034): 4.7%

- Top Region: North America – driven by infrastructure and pipeline development

- Top Product: Consumables – high usage of stick electrodes and solid wires

- Top Welding Type: Arc welding – widespread use in automotive and general fabrication

Key Trends and Drivers:

- Tech integration: Augmented reality (AR), robotic systems, and simulators boost training and productivity

- Automotive & aerospace growth: Increased demand for advanced joining processes like FSW and laser welding

- Infrastructure push: Global rise in construction and energy infrastructure elevates welding demand

- Advanced materials: Use of High-Strength Low-Alloy (HSLA) steels and dissimilar material joining fuels innovation

Market Challenges:

- Skilled labor shortage: Aging workforce and low new entrant rate widen the talent gap globally

- COVID-19 impact: Temporary shutdowns and supply chain disruptions lowered output and profitability

Market Opportunities:

- Education tech adoption: AR/VR welding simulators improve training efficiency and attract new talent

- Automation demand: Rising use of automated welding equipment in automotive and heavy industries

- Emerging economies: Rapid industrialization and urban expansion in Asia and Latin America drive long-term demand

Welding Market LATEST TRENDS

Download Free sample to learn more about this report.

Iteration of Advanced Technologies and Equipment in Joining Processes to Propel Market Growth

The increasing trend of augmented reality (AR) applications in the industry is enhancing the quality of the fabrication and increasing the feasibility of accessing and evaluating the soldering quality before initiating the actual operations. Augmented reality is anticipated to play a major role in the fabrication industry for offering training to technicians or students—for instance, Miller Electric Mfg. LLC has a complete Augmented Reality Weld System that offers highly realistic multi-process simulation solutions for classroom training. Also, Fronius International GmbH offers weld education solutions via simulators, thus supporting practical training through videos, scripts, and posters that help students convey theoretical training knowledge. Fronius does offer mobile and standup simulators for easy access to the solutions as per the students’ requirements.

DRIVING FACTORS

Substantial Application of Joining Processes in Automotive and Aeronautic Industry to Bolster Growth

Resistance spot, resistance seam, and friction are some of the prominent soldering processes automotive manufacturers use during the fabrication of automotive vehicles. Moreover, aerospace applications have also witnessed a notable increment in fabrication applications. Over the last decade, most of the riveting operations in the industry have been replaced by joining operations to have a better, more flexible and robust structure and an enhanced framework. Additionally, the emergence of better and cost-effective joining processes provides optimistic development for the market growth. For instance, friction stir welding (FSW) and Laser techniques cement fabrication operations across the regions. The established global automotive manufacturers are making investments to establish and initiate operations from workshops established in various locations.

RESTRAINING FACTORS

Dearth of Skilled Professionals to Hamper Market Growth

Reducing the number of incoming professionals and the scarcity of skilled welders is limiting the production output of the operations and is also adversely affecting the production and development in multiple industries. The lower daily wages and inconsistent compensations outside the North American region are discouraging the development of skilled welders across multiple economies.

According to the research findings and calculated estimates by the American Welding Society (AWS), the average age of the experienced and currently operating welders have an average age of mid-fifties, and many are approaching 60 years of age, concluding their services. The substantial staff retiring from their services and relatively lower incoming of new welders is broadening the requirement to availability gap in prominent industries.

SEGMENTATION ANALYSIS

By Product Type Analysis

Consumables Segment is Dominant Due to Rising Deployment across Various Industry Verticals

Based on product type, the market is segmented into equipment and consumables.

The consumables segment holds a dominant position in this market in terms of revenue due to high demand for customized solutions for joining dissimilar and non-metallic materials, rise in steel consumption, and others. Moreover, this industry emphasizes adopting simple and cost-effective solutions to safeguard the workpiece from the external environment. In such a scenario, consumables are gaining impetus as the raw material utilized for manufacturing comprises copper, rutile, and aluminum, which possess high tensile strength and antioxidants. The consumables segment is further sub-segmented into stick electrodes, solid wires, flux-cored wires, and saw wires & fluxes, are considered.

Owing to versatility, portability, cost–effectiveness, and ease of use, stick electrodes are widely used in the industry. Therefore, they constitute the highest market share and CAGR over the forecast period.

The solid wire segment constitutes the second highest market share and has a good CAGR over the forecast period as they find their application in one of the most widely used arc types, gas metal arc. Flux-cored wires segment also holds considerable market share owing to its adoption in various industries, including heavy equipment manufacturing, construction, and shipbuilding.

Saw wires & fluxes segment finds applications in submerged arc operation, constituting a decent market share and CAGR over the forecast period.

The equipment segment is expected to show a considerable growth rate over the forecast period due to the rising trend of automated machines deployed across various industries, such as automobiles and construction, for joining thermoplastics, metals, and others.

Further, the equipment segment is further sub-segmented into welders, welding jigs and fixtures, auxiliary equipment, and others.

Under the equipment segment, the welders segment is expected to hold the highest market share. It will showcase the highest CAGR over the forecast period owing to rising demand driven by growing industrialization, infrastructure development, and technological advancements.

Welding jigs and fixtures also hold considerable market share and noteworthy CAGR as the demand for jigs and fixtures is closely related to the demand for these machines; increasing need for customization, quality control, efficiency, and productivity is further helping in increasing the demand.

Auxiliary equipment, such as tables and weld wire, are essential joining operations; thus they have a decent market share and CAGR over the forecast period.

By Welding Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Arc Type is Expected to Grow Significantly over the Forecast Period with Rising General Fabrication Industry

By welding type, the market is divided into arc, resistance, oxy-acetylene gas, solid state, and others.

The arc segment is anticipated to show significant growth in the coming years due to the rising adoption of fusion processes and the utilization of High-Strength Low-Alloy (HSLA) across various industries. It is a flexible and cost-effective process. Additionally, MIG/GMAW is commonly used in a variety of industries, including automotive, construction, and manufacturing. Owing to the characteristics of MIG type, such as speed, weld quality, and versatility, it constitutes the highest market share and CAGR. TIG/GTAW also holds considerable market share as it can be used to weld various metals and alloys, including aluminum, steel, nickel alloys, stainless steel, brass, copper, and even gold.

Resistance soldering is anticipated to grow moderately in the coming years. Compared to other joining methods, the low-cost methods, high reliability, efficiency, accessibility, and the ability for robot automation make it ideal for automotive production. Among the resistance, the seam type holds the highest market share as well as CAGR over the forecast period owing to its characteristics such as minimal environmental damage, speed, ease of operation, and wide adoption in different industries.

Spot type also holds a substantial market share. It demonstrates decent CAGR over the forecast as it does not require any filler metals to weld metal pieces, has high productivity, is easy to operate, and can be automated.

Oxy-acetylene gas and solid-state fabrication are projected to witness progressive market growth in the near future with rising needs in heavy engineering and construction applications.

The others segment is expected to showcase modest growth with limited applications.

By Application Analysis

Heavy Engineering Segment Grow Exponentially in the Coming Years Backed by Introduction of Smart Factories

By application, the market is further categorized into automotive, building & construction, heavy engineering, railway & shipbuilding, oil & gas, and others.

The heavy engineering segment is expected to grow exponentially over the forecast period owing to the introduction of smart factories, industry 4.0, rising automation and others. Moreover, the high demand for precision welds is widening, mainly for joining two different metals without losing their properties, further supplementing the market growth.

The automotive segment is expected to grow significantly in the forecast period as the automotive industry is focusing on reducing the weight of vehicles by replacing metal parts with plastics, which requires high precision. Moreover, the automotive industry prefers to embrace advanced technology to make the best use of high tensile strength steels deployed in manufacturing automotive parts and establish a global position of technological superiority, further boosting the market.

Besides, with the increasing number of residential & commercial projects, the building & construction segment is expected to grow considerably over the forecast period. Also, government initiatives for infrastructure development and bank loans at cheaper rates will uplift the construction sector.

The oil & gas and railway & shipbuilding segments are expected to grow moderately over the forecast period due to rising infrastructure in developing economies and adopting various precision techniques to perform critical operations such as railway tracks and underwater pipelines.

REGIONAL ANALYSIS

Asia Pacific Welding Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The scope of the study is further segmented across five major regions, North America, Europe, Asia Pacific, the Middle East and Africa, and South America. They are further categorized into countries.

Asia Pacific

Asia Pacific dominated the market, with valuations of USD 9.51 billion in 2025 and USD 9.96 billion in 2026. Asia Pacific holds the highest share and is anticipated to grow in the forecast period due to local registered and unregistered manufacturers and rising construction and heavy engineering industries, majorly in China, Japan, and India. For instance, in March 2020, China government released investment plans and “major infrastructure” projects wherein around USD 4.8 trillion would be invested to overcome the potential pressure of the COVID-19 outbreak and boost the dipping real estate business.

China will dominate the Asia Pacific market with the highest market share as well as CAGR over the forecast period due to a large number of equipment manufacturers and the growing number of consumables producers. The country’s manufacturing sector largely influences the market. Supportive government policies in the country have helped the market grow. China has also made a significant investment in research & development in recent years, which has accelerated market growth.

North America

North America and Europe are anticipated to grow steadily in the coming years due to major manufacturers operating in this region. Additionally, the explicit efforts of these companies regarding technological developments, focus on aftermarket services, and high pouring of investments in research and development activities are contributing to the market growth.

To know how our report can help streamline your business, Speak to Analyst

The Middle East & Africa and South America are expected to grow moderately due to increasing construction expenditure in these regions. For instance, according to the International Trade Administration (ITA), in 2019, the Brazilian Ministry of Infrastructure planned 59 new construction projects with a total investment of around USD 10 billion. Besides high investments in the oil & gas sector, the MENA region is also projected to influence the market potential in the coming years. For instance, in January 2019, China led an investment in oil & gas projects in the Middle East and Africa of around USD 75 billion.

KEY INDUSTRY PLAYERS

Key Players Are Focusing on Cost Leadership Strategy to Stay Competitive in the Global Market

Major manufacturers are adopting various pricing strategies to counter fluctuating raw material prices. For instance, Lincoln Electric adopted a product mix and effective pricing management approach to pursue profitability despite persistent raw material inflation. Also, suppliers proactively improvise their existing product lines in terms of costs, quality, and processes to meet the customers' changing needs and maximize profitability. For instance, DENYO CO., LTD. focuses on machines by reviewing the sales structure and developing new products to stay competitive in the market.

LIST OF KEY COMPANIES PROFILED:

- Lincoln Electric (U.S.)

- KOBE STEEL, LTD (Japan)

- ESAB (U.S.)

- Fronius International GmbH (Austria)

- ZULFI (Saudi Arabia)

- KISWEL CO., LTD. (South Korea)

- CS HOLDINGS CO., LTD. (South Korea)

- RME MIDDLE EAST (UAE)

- voestalpine BÖHLER Edelstahl GmbH (Austria)

- capilla GmbH (Germany)

- Tianjin Golden Bridge Welding Materials Group International Trading Co., Ltd. (China)

- Miller Electric Mfg. LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- February 2023 – TriMas made an agreement to acquire the net operating assets of Weldmac Manufacturing, a manufacturer of metal fabricated assemblies and components for aerospace and defense.

- November 2022 – Manufacturing Technology, Inc. acquired Friction Welding Technologies Pvt. Ltd. (FWT), a direct drive friction weld company. It was the result of their strategic partnership formed in 2017. Through the acquisition, MTI aims to increase its product offerings in North America and Europe.

- January 2022 – Fronius International GmbH introduced an intelligent, high-end series of Option CycleTIG named “iWave,” which offers high quality, flexible and flawless weld results for all weldable materials. This multiprocess system provides customized solutions as per the requirements.

- December 2021 – The Lincoln Electric Company introduced Welder/Generator ‘Ranger 330MPX EFI’, a versatile and compact unit built for all seasons with a more powerful, smarter, smaller, and quieter machine.

- October 2021 – To celebrate the “75 years of Fronius” anniversary, the company manufactured a limited edition of the compact TransPocket 150 in vintage design to train future fabrication experts (fabrication students). This limited-edition was handed over by Mr. Peter Fronius himself to the Wels School.

REPORT COVERAGE

The global welding market research report provides detailed information regarding various insights into the market. Some of them are growth drivers, restraints, competitive landscape, regional analysis, and challenges. It further offers an analytical depiction of the market, current trends, and estimations to illustrate the forthcoming investment pockets. The market is quantitatively analyzed from 2022 to 2029 to provide the financial competency of the market. The information gathered in this report has been taken from several primary and secondary sources.

Request for Customization to gain extensive market insights.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021 – 2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026 – 2034 |

|

Historical Period |

2021 – 2024 |

|

Growth Rate |

CAGR of 4.7% from 2026 to 2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Product Type, Welding Type, Application, and Region |

|

By Product Type |

|

|

By Welding Type |

|

|

By Application |

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 27.11 billion in 2025 and is projected to reach USD 40.99 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 9.51 billion.

The market will exhibit steady growth of 4.7% CAGR in the forecast period (2026-2034).

The heavy engineering segment is expected to be the leading segment in this market during the forecast period.

Substantial application of joining processes in the automotive and aeronautic industry is a major factor driving the market growth.

The Lincoln Electric Company, ESAB, and Kobe Steel are the major market players.

Asia Pacific dominated the market share in 2025.

Lack of availability of skilled welders is expected to hamper the market.

Arc segment is expected to lead the market.

The current market trend is the iteration of advanced technologies and equipment in joining processes.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us