Nylon Market Size, Share & Industry Analysis, By Type (Nylon 6 {Resin & Fiber} and Nylon 6,6 {Resin & Fiber}), By Application (Automotive, Electrical & Electronics, Appliances, Film & Coating, Wire & Cable, Consumer, Industrial & Machinery, and Others), and Regional Forecast, 2026-2034

NYLON MARKET SIZE AND FUTURE OUTLOOK

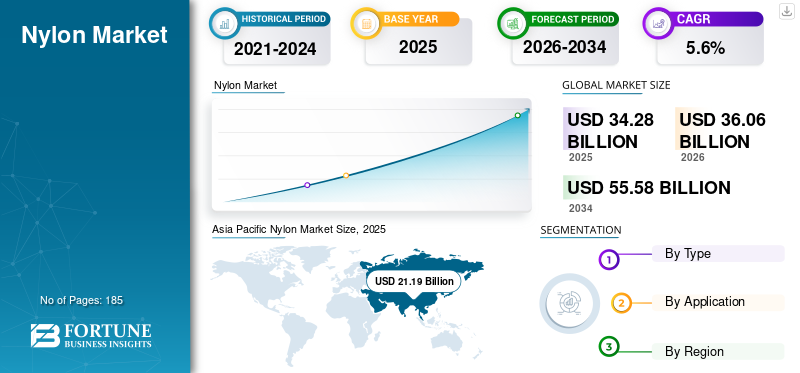

The global nylon market size was valued at USD 34.28 billion in 2025. The market is projected to grow from USD 36.06 billion in 2026 to USD 55.58 billion by 2034, exhibiting a CAGR of 5.6% during the forecast period.

Typically, nylon or polyamide (PA) is manufactured by polymerizing caprolactam or adipic acid and hexamethylene diamine. It is a highly versatile polymeric material used in various industries for different applications. The adoption of the product is significant in automotive and sports applications. For instance, polyamide fiber is used in the airbags of vehicles as well as in professional volleyball nets.

Players operating in this industry are improving their production capacities to serve the increasing demand from various end-use industries. For instance, in July 2022, Invista announced investments in its production plant in South Carolina, U.S. The investment will change the facility’s polyamide production process and logistics capabilities. Key players operating in the market include DuPont, BASF SE, Lanxess AG, and Nylon Corporation of America, Inc., among others.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

NYLON MARKET TRENDS

Inclusion of PA 6 and PA 6,6 in 3D Printing to Provide Market Growth Opportunities

PA 6 and PA 6,6 have superior properties, such as high durability and flexibility, making them a good choice for 3D printing. Excellent malleability makes them much tougher than other traditionally used thermoplastics such as PLA and ABS. Hence, these polymers have the potential to become the go-to material for 3D printers. PA exhibits excellent chemical resistance and mechanical properties comparable to ABS. It has an impact resistance that is significantly higher than that of ABS, which makes it a potential material of choice in manufacturing industrial components. Besides, the moisture absorption property helps with easy post-processing with fabric dyes and spray paints.

The flexibility and durability of polyamide can help in 3D printing parts with thin walls. The low coefficient of friction with a high melting point makes it especially resistant to abrasion. Thus, it can be used in printing parts such as functional interlocking gears. Advancements in 3D printing technology are likely to augment polyamide adoption in industrial 3D printing operations, propelling nylon market growth.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand from the Automotive Industry to Drive Market Growth

Polyamide is extensively used in the automotive industry due to its high workability, strength, and toughness. The polymer supports both the molding and extrusion processes and can be used to manufacture a variety of auto parts. Properties, such as high-temperature resistance and chemical resistance, make it the material of choice for harsh environments. For instance, auto parts that are exposed to extreme temperatures and fluids, such as engine lubricants, are developed from polyamide. PA 6 and PA 6,6 parts are relatively lighter than metallic components. This factor can significantly improve the efficiency of conventional IC-powered vehicles. Due to the high prices of gasoline and rising environmental concerns, the vehicle economy is becoming the main aspect when purchasing vehicles.

The automotive sector has witnessed a paradigm shift toward electric vehicles over the past few years. Major automakers, such as Ford, General Motors, Volkswagen, Toyota, and Tata Motors, are already bidding high on the electric future. Maintaining a high power-to-weight ratio is a key challenge for the electric vehicle industry. Since lighter vehicles influence the battery size, employing lighter materials can be crucial in reducing the overall weight of the electric vehicle. Developing economies, such as China and India, are likely to witness an increase in the demand for mobility solutions during the forecast period owing to the volume growth in population. The rising purchasing power of consumers in developing economies is likely to push the demand for both commercial and passenger vehicles. Advanced engineering materials are poised to be widely employed in auto parts manufacturing due to their superior properties. Thus, the rising demand for the material from the automotive industry is anticipated to drive market growth.

Surging Demand from Electrical & Electronics and Wire & Cable Applications to Drive Market Growth

The escalating demand for nylon in electrical & electronics and wire & cable applications is fueling market expansion. The exceptional properties of the product, including high strength, flexibility, and thermal resistance, make it an ideal material for insulation and protecting wires and cables in various electronic devices and electronic systems. As the electronic industry continues to grow and innovate, there is an escalating need for reliable and durable materials to ensure the safe and efficient transmission of electrical signals. The product’s versatility and ability to meet stringent industry standards for performance and safety make it increasingly sought after by manufacturers. Moreover, the transition toward electric vehicles and renewable energy infrastructure further amplifies the demand for the product in wire and cable applications, significantly driving the market growth.

MARKET RESTRAINTS

Stringent Regulations for Decreasing the Negative Environmental Impact to Hinder Market Growth

Plastic pollution has become the most pressing challenge that the world currently faces. PA 6 and PA 6,6, which are non-biodegradable, remain in the environment for several years. Microplastics, formed due to the breakdown of macroscopic plastics, have a negative environmental impact. These microplastics contaminate the oceans and are ingested by aquatic creatures. Fishing nets are among the major sources of microplastic pollution in the ocean, other than the synthetic textile fibers that wear off during washing.

The dyeing of fibers can contribute significantly to water pollution since a significant share of polymers is typically produced in countries with weaker environmental regulations. The production and processing of polyamide are among the significant contributors to water pollution in developing economies. Furthermore, the production process itself is an energy-intensive process leading to increased fuel consumption and greenhouse gas emissions.

Consumers have become increasingly concerned and aware of environmental health in the last decade. In response, governments and international organizations, in collaboration with the private sector, are establishing methodologies to monitor the adverse effect of polymers. Companies utilizing polyamide and similar polymers are required to restrict and regulate their use to meet stringent standards. This factor may hamper the market growth.

MARKET OPPORTUNITIES

Electrification and Lightweighting to Offer Opportunities in the Engineering-Plastics Space

A major opportunity for the global market is the continued shift toward lightweight, high-strength materials in transportation, electrical, and industrial equipment. Nylon’s balance of toughness, heat resistance, and design flexibility supports metal replacement in functional parts, while its processability enables complex geometries that reduce assembly steps and total system cost.

This opportunity strengthens as electrification increases the number of connectors, housings, cable-management parts, and thermal-management components required per vehicle and per device. Suppliers that can offer stable performance across temperature and humidity ranges, along with application-specific grades for flame retardance, impact, and dimensional stability, are well positioned to capture long-term demand.

MARKET CHALLENGES

Upstream Volatility and Tight Specifications to Create Margin and Qualification Risk

Nylon pricing and profitability are structurally exposed to upstream intermediates and energy costs, which can swing sharply across cycles. This creates recurring challenges for converters and end users in budgeting, long-term contracting, and maintaining product price stability, especially in segments where cost sensitivity is high and substitution pressure is constant.

In parallel, many high-value nylon applications require long qualification cycles and strict consistency in viscosity, additive packages, and mechanical properties. Any disruption in feedstock availability, grade changes, or processing window can trigger requalification costs and delays, raising supply-chain risk and increasing the importance of reliable, multi-region sourcing strategies.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade policy and geopolitics increasingly influence nylon and intermediates flows by changing the economics of cross-border supply. Tariffs, anti-dumping actions, and shifting customs scrutiny can alter import competitiveness, creating sudden price dislocations and prompting downstream buyers to diversify suppliers or regionalize procurement to reduce exposure.

Structurally, these pressures can accelerate local capacity investments and encourage near-market production, particularly where governments prioritize industrial resilience. While regionalization may raise short-term costs and reduce spot-market flexibility, it can also stabilize long-term supply for strategic sectors such as automotive, electrical, and industrial manufacturing.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D activities in the market are increasingly centered on circularity, including chemical recycling routes that recover monomers and enable near-virgin performance, as well as improved mechanical recycling for controlled waste streams. These efforts are aimed at solving the core barriers of contamination, property retention, and economics, while building credible pathways to scale which brands and OEMs can adopt without performance compromise.

Segmentation Analysis

By Type

Nylon 6 Segment Accounts for Major Share Due to High Adoption and Cheap Cost

By type, the market is segregated into Nylon 6 (resin & fiber) and Nylon 6,6 (resin & fiber).

The Nylon 6 fibers segment dominates the global market. The growth is primarily due to its extensive use in the textile industry. The material offers a favorable balance of toughness, mechanical strength, abrasion resistance, and cost-effectiveness, making it suitable for a wide range of textile and industrial applications. It is widely used in the production of webbing products, including luggage straps, dog leashes, sports goods, and safety belts, where durability and wear resistance are essential.

Nylon 6,6 possesses excellent properties, such as high elasticity of engineering plastics, making it ideal for injection molding applications. It is predominantly used for making plastic components for electronic appliances, automotive, and other industries. Besides, PA 6,6 films and coatings produced by the extrusion process have a considerable demand in the packaging sector, especially for packaging food and fluids such as acidic food, grease, and oils. These are clear, printable, and thermoplastic films that make them ideal for industrial applications. It is also suitable for use in microwave cooking applications. These films have exceptional strength, toughness, and excellent oxygen barrier properties while also being puncture, scratch, and flex-crack resistant. The segment is projected to grow at a CAGR of 6.1% during the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Automotive Segment Held the Highest Revenue in 2025 Owing to Extensive Application

By application, the market is categorized into automotive, electrical & electronics, appliances, film & coatings, wire & cable, consumer, industrial & machinery, and others.

The automotive segment accounted for the largest nylon market share in 2025. The high usability of the fiber and resin in automobiles in the form of airbags, tire cord, and injection molded components results in the generation of high revenue from this segment. The demand for plastics for reduction of vehicle weight and optimization of fuel efficiency is continuously increasing in the automotive industry. With the increasing sales of electric vehicles and the establishment of proper electric vehicle infrastructure, engineering plastics are anticipated to play a major role.

The film & coatings segment accounts for the second-highest share of the global market and is projected to grow at a CAGR of 6.3% during the forecast period. Polyamide films exist as un-oriented polymers and bi-axially oriented (BOPA) films. These films are predominantly used to package goods and products that require a high oxygen barrier and high strength. Some of these products include processed meat (sausage, bacon), cheese & other dairy products, smoked fish, and semi-finished microwavable meals. Moreover, these films are easily recyclable. The ban on the use of single-use plastics globally is expected to boost market share during the forecast period.

NYLON MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Nylon Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held a dominant market share in 2025 and is anticipated to stay dominant, on account of the rising demand from films & coating for packaging sector and automotive applications during the analysis period. The demand in the region is predominantly driven by emerging economies such as India and China. China accounts for over a half of the total production and consumption in the region. Further, to decrease its dependence on imports, major producers are coming up with production facilities in China to cater to the rising demand in the country and the surrounding region. On the other hand, PA 6 and caprolactam are oversupplied in the regional market, which resulted in lower operating rates.

China Nylon Market

The China market is one of the largest markets worldwide. The 2025 revenue of the country stood at USD 14.42 billion, representing roughly 42.1% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is a significant producer of polyamide. The automotive industry drives the regional market. The U.S. has witnessed rapid rise in electric vehicle sales in recent years, which is likely to be persistent during the analysis period. According to the U.S. Department of Energy, the electric vehicle sales escalated by 85% in 2021 relative to the previous year. This can be attributed to the increased demand for commercial and passenger vehicles over the last decade. The ban on single-use plastics in the U.S. is expected to further increase the demand for nylon films in the region.

U.S. Nylon Market

The U.S. market is likely to register positive growth. The market was valued at USD 3.77 billion in 2025, representing roughly 11.0% of global sales.

Europe

The Europe market is expected to grow moderately over the forecast period, backed by strong demand from the automotive industry. Lawmakers in Europe are launching attractive policies, such as subsidies, to enhance electric vehicles sales. For instance, Germany has extended the electric vehicle subsidy and expanded the criterion for environmental bonus to owners of e-vehicles until the end of 2025. Similarly, France has also increased the subsidy amount. Meanwhile, countries, such as Sweden, have announced an exemption from vehicle tax for e-vehicle owners. This factor is expected to increase electric vehicle sales and consumption in the automotive industry during the forecast period. Moreover, the EU has voted for a complete ban on single-use plastic by 2021, which is expected to boost the consumption of recyclable plastic films during the forecast period.

Germany Nylon Market

The Germany market held a revenue of USD 1.68 billion in 2025, representing roughly 4.9% of global sales.

France Nylon Market

The France market accounted for a revenue at USD 0.74 billion in 2025, representing roughly 2.1% of global sales.

Latin America

Latin America holds a single-digit market share, with Mexico being the key consumer. However, Brazil is projected to indicate the fastest growth in the regional market due to the fastest expansion of the end-use industry. Moreover, the healthy growth of all end-use industries in the rest of the Latin American economies, such as Columbia and Argentina, are also expected to drive the market.

Mexico Nylon Market

The Mexico market reached a revenue at USD 0.67 billion in 2025, representing roughly 2.0% of global sales.

Middle East & Africa

The Middle East & Africa market is projected to grow at a moderate CAGR during 2026-2034. The GCC dominated the market due to rapid industrialization in the region. The rising adoption of industrial coatings, growth in automotive sales, and favorable growth in the construction industry are driving the market growth in the region.

GCC Nylon Market

The GCC market is one of the largest worldwide. The 2025 revenue of the country market reached USD 0.51 billion, representing roughly 1.5% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Companies Focus on Expansion of Production Facilities to Boost Sales Revenue

The global market is already oversupplied due to a large number of installed capacities. Key players in the supply chain are increasing the capabilities of the product and its feedstock, such as adiponitrile. Ube Industries, INVISTA, and Ascend are some of the players expanding their capacities and feedstock to meet the increasing demand. Further, the prices of these polymeric materials are highly volatile, which is expected to hamper market growth. However, pricing contracts with customers may help stabilize the costs. In addition, the changing geopolitical equations and trade policies directly impact the supply chain.

LIST OF KEY NYLON COMPANIES PROFILED

- DuPont (U.S.)

- BASF SE (Germany)

- Lanxess AG (Germany)

- Nylon Corporation of America, Inc. (U.S.)

- Shenma Industrial , Ltd. (China)

- Ascend (U.S.)

- Domo Chemicals (Belgium)

- Radici Partecipazioni SpA (Italy)

- Invista (U.S.)

- DSM (Netherlands)

- Formosa Group (Taiwan)

- SINOPEC (China)

- Ube Industries (Japan)

- LIBOLON (Taiwan)

- ZIG SHENG INDUSTRIAL CO., LTD. (Taiwan)

KEY INDUSTRY DEVELOPMENTS

- April 2023: Microwave Chemical and Asahi Kasei together launched a demonstration project for the commercialization of the chemical recycling process for Nylon 66 using microwave technology.

- April 2023: Tire and nylon manufacturing company Kordsa announced plans to invest USD 50 million for the expansion of its nylon production at its Chattanooga plant. The move is anticipated to enable the company to meet the rising demand from the automotive industry.

- November 2022: INVISTA initiated the construction of its new nylon production facility. The company announced plans to invest USD 64 million for this new plant to enhance its polymer and CORDURA fiber spinning production. The construction of new facility would enable company to increase its production capacity and deliver newly developed products to the market.

- April 2022: DOMO chemicals expanded the production capacity of TECHNYL polyamide in China. This plan aims to meet growing demand in the automotive, electrical & electronics, and industrial consumer goods industries.

- March 2022: BASF planned the expansion of its Ultramid polyamide production capacity in India. The surge in capacity expansion would help meet the growing requirements of PA 6 and PA 6,6 in domestic end-use sectors such as industrial manufacturing, consumer goods, automotive, and electronics.

- February 2022: BASF announced plans to expand its polyamide (nylon) and polyphthalamide offerings in Europe. The move is anticipated to help the company in strengthening its backward integration to cover the entire value chain of polyamide 66.

- January 2022: BASF announced plans for expanding its PA 6,6 production in Freiburg in Germany. The company also expressed intent to construct a new hexamethylene diamine (HMD) plant in Chalampé, France. HMD is a precursor utilized in the production of PA 6,6 plastics and raw materials’ This unit is anticipated to begin production by 2024.

- January 2022: China Pingmei Shenma Group and Invista inked agreements for establishing a strategic relationship. This agreement includes a five-year plan for adiponitrile and adipic acid purchase and sale and the license of key technologies for the manufacturing of polyamide.

- November 2021: LANXESS announced plans to expand its high-tech plastics production capacity in China. These plastics include polyamide compounds marketed under the brand name Durethan. The company planned to invest funds to increase the total production capacity of high-tech plastics in China by 30,000 metric tons per year. Through this expansion, the company aims to meet the rising demand from the Chinese automotive industry, especially in the electric vehicles segment.

- June 2021: Ascend Performance Materials enhanced the production capacity of its HiDura PA 610 and 612, the new long-chain PA product line. These polymers will be used to develop durable materials for EVs, consumer goods, and industrial applications.

REPORT COVERAGE

The report provides qualitative and quantitative insights on the growth rate, market share, size, and trend analysis by different segments. Along with this, the research report provides an elaborative analysis of the market dynamics and competitive landscape. Various key insights presented in the report are Porter’s five forces, recent industry developments in the market, regulatory scenario in crucial countries, macro & microeconomic factors, SWOT analysis, key industry trends, competitive landscape, and company profiles.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.6% from 2026 to 2034 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Type, Application, and Region |

|

By Type

|

|

|

By Application

|

|

|

By Region

|

|

Frequently Asked Questions

Fortune Business Insights says that the market was valued at USD 34.28 billion in 2025 and is expected to reach USD 55.58 billion by 2034.

The market will exhibit considerable growth at a CAGR of 5.6% over the forecast period.

The automotive segment led the market by application in 2025.

Increasing product consumption across the automotive and film & coatings industries is a key factor driving the growth of the market.

Asia Pacific held the highest market share in 2025.

DuPont, BASF SE, Nylon Corporation of America, Lanxess, and INVISTA are the key players in the market and have adopted strategies, such as acquisition and capacity expansion, for their growth in the market.

The inclusion of PA 6 and PA 6,6 in 3D printing is a key trend in the global market.

- 2021-2034

- 2025

- 2021-2024

- 185

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us