Point of Sale (PoS) Market Size, Share & Industry Analysis, By Component (Hardware and PoS Terminal Software), By Type (Fixed PoS, Mobile PoS, and Others), By Deployment (On-premise and Cloud-based), By Operating System (Windows/Linux, Android, and iOS), By Payment Technology (Cards, NFC, QR Codes, and Mobile Wallet), By End-user (Restaurants, Retail, Entertainment, and Others), and Regional Forecast, 2026 – 2034

Point of Sale Market Size

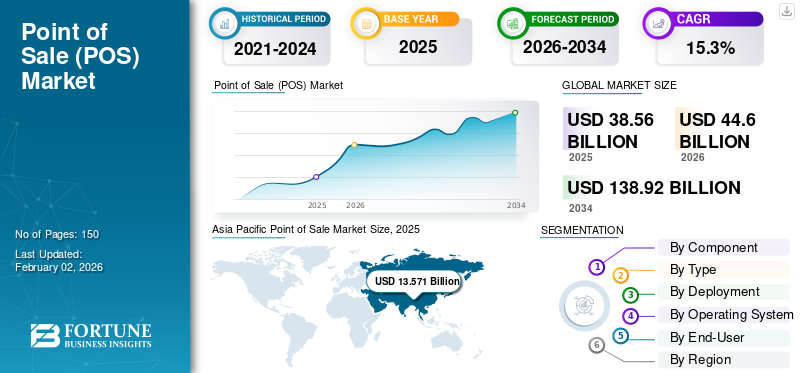

The global point of sale (PoS) market size was valued at USD 38.57 billion in 2025. The market is projected to grow from USD 43.32 billion in 2026 to USD 116.26 billion by 2034, exhibiting a CAGR of 13.1% during the forecast period.

Point of sale (PoS) systems offer several advantages to businesses across retail, restaurants, hospitality, healthcare, entertainment, and other service industries. These systems help minimize human errors in transactions by automating billing, pricing, tax calculation, discounts, and change management. Modern POS platforms are also integrated with inventory tracking, enabling businesses to monitor stock levels in real time data, reduce stockouts or overstocking, and improve reorder planning. In addition, POS systems generate detailed sales reports and analytics, helping businesses track customer preferences, product performance, peak sales periods, pricing trends, and promotional effectiveness.

The growing shift toward omnichannel retail is further increasing the importance of advanced POS systems. Retailers and restaurants now require POS platforms that can connect in-store sales, online orders, mobile payments, loyalty programs, delivery platforms, and inventory systems through a unified interface. This is encouraging businesses to adopt cloud-based, mobile, and integrated POS solutions that support both physical-store transactions and digital commerce workflows.

Leading companies in the market comprise Block, Inc., Toast, Inc., NCR Voyix Corporation, PAX Technology, Oracle Corporation, and Ingenico Group. These players are focusing on cloud POS, restaurant-specific platforms, smart terminals, AI-enabled applications, and unified commerce solutions to strengthen their market presence and maintain competitiveness.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Personalized Shopping, Intelligent Store Operations, and Dynamic Pricing Optimization to Fuel Market Expansion

Generative AI is expected to significantly influence the point of sale (PoS) market growth by improving customer engagement, store operations, pricing decisions, and transaction security. AI-enabled POS systems can analyze customer purchase history, product preferences, basket behavior, and loyalty data to provide personalized recommendations, targeted promotions, and customized checkout experiences. This helps retailers and restaurants improve customer satisfaction, increase repeat purchases, and strengthen loyalty programs. Generative AI can also support store associates by providing real-time product information, inventory visibility, pricing insights, and customer-specific suggestions at the point of sale.

In addition, AI-based POS platforms can support dynamic pricing, demand forecasting, fraud detection, and inventory optimization. These systems can analyze transaction patterns, market demand, competitor pricing, and customer behavior to help businesses adjust pricing strategies and improve profitability.

- In November 2025, ToneTag introduced RetailPOD 3.0, an AI-enabled payment acceptance device designed to talk, transact, and improve customer engagement at the retail point of sale.

- In June 2025, Microsoft highlighted how Dynamics 365 Commerce POS is evolving into an AI-driven storefront with Copilot capabilities that support store associates with customer preferences, inventory, and pricing insights.

- In January 2025, Toshiba Global Commerce Solutions launched new retail innovations at NRF 2025, including self-service solutions and POS hardware using AI, computer vision, and machine learning.

Such developments indicate that generative AI is transforming POS systems from basic transaction tools into intelligent commerce platforms.

Point of Sale (PoS) Market Trends

Rising Adoption of Cloud-based POS, AI Integration, and Unified Commerce Platforms to Aid Market Growth

The surging adoption of cloud-based and AI-enabled POS solutions is supporting the modernization of retail, restaurant, and service-sector operations. Businesses are moving away from traditional on-premise POS systems toward cloud platforms that offer remote access, faster software updates, real-time inventory visibility, omnichannel order management, customer data integration, and advanced analytics. AI integration is further improving POS capabilities by supporting personalized recommendations, inventory optimization, demand forecasting, loyalty management, and employee productivity. For instance,

- In January 2026, NCR Voyix unveiled an AI-accelerated application suite on the Voyix Commerce Platform, including VoyixPOS. The solution has been launched to help retailers and restaurants improve operations, customer experience, and business outcomes.

- In October 2025, Zebra Technologies and Salesforce introduced a Retail Cloud POS solution on Android to streamline store operations and improve frontline associate productivity.

- In January 2025, Salesforce launched Agentforce for Retail and Retail Cloud with Modern POS to help retailers improve productivity, unify in-store and digital shopping, and deliver personalized customer experiences.

Such developments indicate that cloud-based, AI-enabled, and unified commerce POS platforms are becoming key growth drivers in the global POS market.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Adoption of Digital Payments, Mobile Wallets, and QR-based Transactions to Fuel Market Growth

The growing adoption of digital payments, mobile wallets, QR-based payments, and contactless transactions is significantly supporting the demand for modern POS systems. Consumers are increasingly using payment apps, cards, mobile wallets, UPI, Apple Pay, Google Pay, and other contactless methods for daily transactions, encouraging retailers, restaurants, and service providers to upgrade their POS infrastructure. Younger consumers and digitally active shoppers are especially driving the adoption of mobile-first payment experiences, where speed, convenience, and secure checkout are key expectations. This is pushing POS providers to integrate multiple payment modes, including cards, wallets, QR codes, UPI, and tap-to-pay, into a single platform.

- In October 2025, Zoho Payments launched POS devices that support card payments, UPI QR codes, and soundbox-based payment confirmations, showing how POS platforms are being upgraded to support faster and more seamless digital transactions.

- In March 2025, Visa reported that its Tap to Phone solution recorded 200% year-on-year growth globally, enabling small businesses to accept contactless payments directly on smartphones.

Such advancements are expected to strengthen POS adoption across retail, restaurants, hospitality, banking, and other service industries.

MARKET RESTRAINTS

Data Security Concerns May Impede the Market Growth

Data security is a major concern in the PoS market for businesses and consumers. Unauthorized access to payment card data may lead to data breach. If PoS systems are compromised, it can lead to the exposure of payment card information, putting customers at risk of fraud and identity theft. Furthermore, inadequate password protection and weak authentication measures can make PoS systems vulnerable to unauthorized access. This may lead to unauthorized individuals gaining control over the PoS system and accessing sensitive data. In addition, integrations with third-party services or software can introduce security risks. If these third-party components are not adequately secured, they can serve as entry points for cyber attackers to gain access to PoS systems. These factors are expected to hamper the market growth.

MARKET OPPORTUNITIES

Self-checkout and Kiosk-based POS Adoption to Create Strong Growth Opportunities in Retail and QSRs

The rising adoption of self-checkout and self-ordering kiosks is creating a strong opportunity for market players, especially across retail stores and QSR chains. Retailers are using self-checkout to reduce queues, improve store throughput, and manage labor shortages, while QSRs are using kiosks to support faster ordering, upselling, digital payments, and kitchen workflow integration For instance,

- In July 2025, NCR Voyix stated that global self-checkout shipments in 2024 reached the second-highest level ever, with the company holding 22% of total shipments. This showcases strong retailer investment in automated checkout systems.

The National Restaurant Association reported that, in restaurants, operators increasingly view technology as a competitive advantage, with customers showing interest in tools that make ordering and payment faster. McDonald’s has also been testing cash-accepting self-service kiosks in U.S. stores, reflecting how QSRs are expanding kiosk use beyond card-only digital ordering. These developments indicate that self-checkout and kiosk-based POS systems will remain a major growth avenue across developed markets such as North America, Europe, Japan, South Korea, and GCC.

Segmentation Analysis

By End-User

Greater Adoption of Point of Sale Solutions in Retail Shops to Spur Retail Segment Expansion

The market is divided into retail, restaurants, entertainment, and others (gas stations, transportation, and so on) based on end-user.

The retail segment held the largest market share of 43.7% in 2025. This is due to the increasing adoption of PoS systems in retail shops as it is time and cost-efficient and provides real-time data about sales performance. Moreover, this system makes it easy for retailers to manage promotions and discounts. They can apply discounts, track promotional effectiveness, and implement targeted marketing campaigns directly through the PoS solutions.

The restaurants segment is estimated to showcase the highest CAGR of 15.4% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Increasing Installation of Hardware to Enhance Transaction Processing to Foster Hardware Segment Growth

Based on component, the market is classified into hardware and PoS terminal software.

The hardware segment secured the maximum share in the market in 2025 as it facilitates quick and accurate transaction processing. This leads to faster checkouts, reducing waiting times for customers and improving overall operational efficiency. As a result, the installation of PoS hardware has gained momentum in restaurants, retail, banking, and gas stations across the globe.

The PoS terminal software segment is expected to grow at the highest CAGR during the forecast period.

By Type

Capability to Enhance the Overall System’s Functionality in Retail to Fuel the Fixed PoS Segment Growth

Based on type, the market is divided into fixed PoS, mobile PoS, and others (barcode scanner, receipt printer, cash drawer, and so on).

The fixed PoS segment is likely to hold the largest share of 63.6% in the market in 2025. Fixed PoS solutions are designed for stability and reliability. The dedicated hardware and infrastructure at a fixed location contribute to consistent performance, reducing the risk of technical issues. These terminals have larger display screens and can accommodate additional peripherals such as customer displays, card readers, and others to enhance the overall functionality of the system in the retail sector. These factors are spurring the segment growth.

The mobile PoS segment is expected to grow at the highest CAGR of 15.80% during the forecast period.

By Deployment

Surge in Adoption of Cloud-based PoS Systems to Boost the Market Growth

Based on deployment, the market is bifurcated into on-premise and cloud-based.

The cloud-based segment held the maximum point of sale (PoS) market share in 2025 and it is expected to continue its dominance by growing at the highest CAGR of 16.40% over the analysis period. These solutions allow businesses to access their data and perform transactions from any location with an internet connection. This is particularly valuable for businesses with multiple locations, enabling centralized management and real-time visibility. In addition, cloud-based PoS systems often have lower upfront costs compared to traditional on-premises solutions. Businesses can avoid significant investments in hardware and infrastructure, and instead, pay a subscription fee based on usage.

The on-premise segment is expected to grow at the second-highest CAGR of 11.90% during the forecast period.

By Operating System

Windows/Linux OS Segment to Expand due to Rising Implementation with User-friendly Interface

Based on operating system, the market is categorized into Windows/Linux, Android, and iOS.

The Windows/Linux segment held the maximum share of 49.7% in the market in 2025, owing to its user-friendly interface, integration capabilities, and compatibility with a wide range of software applications. This familiarity makes it easier for staff to adopt point of sale system, reducing training time and minimizing errors during transactions. In addition, Windows OS supports multi-tasking, allowing small and medium sized businesses to run multiple applications simultaneously.

The Android segment is anticipated to grow at the highest CAGR of 17.10% during the forecast period.

By Payment Technology

Widespread Merchant Acceptance of Card Payments to Fuel Cards Segment Growth

Based on payment technology, the market is categorized into cards, NFC, QR codes, and mobile wallet.

The cards segment captured the maximum market share of 45.3% in 2025 due to their deeply established acceptance infrastructure across retail, hospitality, and service sectors. Banks, merchants, and payment networks have invested heavily in card issuance and POS terminal deployment over the past two decades, creating strong network effects that favor card usage. Additionally, credit and debit cards remain the preferred payment method for higher-value transactions due to their widespread consumer trust, security features, and access to credit and rewards programs.

The QR codes segment is anticipated to grow at the highest CAGR of 19.20% during the forecast period.

Point of Sale (PoS) Market Regional Outlook

By region, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

Asia Pacific

Asia Pacific Point of Sale (PoS) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for a valuation of USD 13.75 billion in 2025. The regional market is expected to hold a major share in the POS market and grow at the highest CAGR over the analysis period. This is due to its large retail base, fast-growing merchant digitization, and strong adoption of QR, wallet, mobile POS, and smart POS systems. China remains a major contributor, supported by its large retail economy, with total retail sales of consumer goods reaching USD 6.73 trillion in 2024, up 3.5% year-on-year.

India is also driving strong growth, as NPCI data shows UPI handled 23.20 billion transactions in May 2026, reflecting rapid digital payment adoption among small retailers, restaurants, and service merchants. In addition, India’s QR code deployments surged 126% to 633.44 million, while POS terminals crossed 10 million, showing strong merchant-side digital infrastructure expansion.

ASEAN further supports regional growth through QR payment systems such as QRIS, DuitNow QR, SGQR, PromptPay, VietQR, and QR Ph, which are improving merchant acceptance across retail, restaurants, tourism, and transportation. The Asia Pacific region leads as it combines China’s large existing POS base, India’s fast merchant digitization, ASEAN’s QR-led growth, and mature high-value markets such as Japan, South Korea, and Australia.

Japan Point of Sale (PoS) Market

The Japan market was valued at around USD 2.19 billion in 2025, accounting for roughly 5.7% of global revenues.

China Point of Sale (PoS) Market

The China market is projected to be one of the largest markets worldwide, with 2025 revenues touching around USD 5.33 billion, representing roughly 13.8% of global sales.

India Point of Sale (PoS) Market

The India market was estimated at around USD 2.39 billion in 2025, accounting for roughly 6.2% of global market share.

North America

The North America market value stood at USD 10.52 billion in 2025. The region holds the second-largest share in the POS market due to its mature retail infrastructure, high card and contactless payment penetration, strong restaurant technology adoption, and rapid shift toward cloud-based POS platforms. The U.S. remains the key contributor, supported by large-scale supermarkets, convenience stores, QSRs, full-service restaurants, hospitality outlets, and service businesses that require advanced POS systems for payments, inventory, loyalty, analytics, and omnichannel operations. Restaurant digitization is also a major driver. For instance,

- The National Restaurant Association reports that 76% of restaurant operators say that technology gives them a competitive edge, with customers favoring tools that make ordering and payment faster.

- Canada further strengthens the region’s position, with Payments Canada reporting that digital payments represented 86% of total payment volume in 2024. In addition, contactless payments accounted for 58% of transactions, supporting continuous POS upgrades across retail and services.

U.S. Point of Sale (PoS) Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market reached a valuation of around USD 8.92 billion in 2025, accounting for roughly 23.1% of sales.

Europe

Europe is projected to grow at a CAGR of 11.1% over the forecast period and reached a valuation of USD 9.25 billion in 2025. The region already has a mature retail, restaurant, and payment acceptance infrastructure. Most large retailers, supermarkets, restaurants, and service businesses already use POS systems. Therefore, growth is driven more by replacement, cloud POS migration, self-checkout, contactless upgrades, and omnichannel retail rather than first-time adoption. The ECB’s 2024 payment study also shows that consumers are gradually shifting toward cards and other electronic payment methods. However, cash remains widely used at POS in several euro area countries, which keeps the transition gradual. Europe will continue adopting advanced POS solutions across restaurants, hospitality, tourism, and retail.

U.K. Point of Sale (PoS) Market

In 2025, the U.K. market was valued at around USD 1.40 billion, representing roughly 3.6% of global revenues.

Germany Point of Sale (PoS) Market

The Germany market reached approximately USD 1.54 billion in 2025, equivalent to around 4.0% of global sales.

South America and Middle East & Africa

The Middle East & Africa market is expected to grow at a significant CAGR over the forecast period due to rising digital payment adoption, SME digitization, and strong growth in retail, restaurants, hospitality, and fuel retail. GCC countries are expanding cashless payment infrastructure, with Dubai’s Cashless Strategy targeting 90% cashless transactions across government and private sectors by 2026. Saudi Arabia also shows strong POS momentum, with SAMA (Saudi Central Bank) publishing weekly POS transaction data across business activities and cities.

In Africa, mobile money is creating new merchant payment opportunities, as GSMA reported that Sub-Saharan Africa had over 1.1 billion registered mobile money accounts in 2024. This combination of GCC-led cashless initiatives and Africa’s underpenetrated merchant base supports faster POS adoption across the region.

South America is expected to grow at the second-highest CAGR in the POS market due to rapid digital payment adoption, SME digitization, and rising use of mobile POS, QR payments, and instant payment systems across retail and restaurants. Brazil is the key growth driver, as the Central Bank of Brazil reported that Pix was the fastest-growing payment instrument in 2024, with transaction volume rising 52% and accounting for nearly 47% of all non-cash payment transactions by Q4 2024. According to PYMNTS, the region is also shifting away from cash, with digital payments accounting for 30% of Latin America’s POS transaction value in 2024, compared with only 2% in 2014.

Countries such as Chile, Colombia, Peru, and Argentina are also seeing higher wallet, QR, and card acceptance, creating strong demand for low-cost POS terminals and cloud-based POS systems. This combination of Brazil’s Pix-led payment expansion, underpenetrated SME merchants, and rising digital acceptance supports South America’s second-highest CAGR.

GCC Point of Sale (PoS) Market

The GCC market reached a value of around USD 0.65 billion in 2025, representing roughly 1.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Players to Focus on Partnerships and Acquisition Strategies to Retain their Dominance

Key market players are focusing on expanding their geographical presence across the globe by presenting industry-specific services. Leading companies are emphasizing acquisitions and collaborations with regional players strategically to maintain dominance across regions. Moreover, top market participants are introducing novel products to increase their consumer base. A surge in constant R&D investments for product innovations is enhancing market expansion. Hence, top companies are rapidly implementing these strategic initiatives to sustain their competitiveness in the market.

List of Key Point of Sale (PoS) Companies Profiled

- NCR Corporation (U.S.)

- Toast, Inc. (U.S.)

- Oracle Corporation (U.S.)

- HP Development Company, L.P. (U.S.)

- Ingenico Group (Worldline) (France)

- PAX Global Technology Limited (China)

- Lightspeed (U.S.)

- Block, Inc. (U.S.)

- Nomia LLC (Russia)

- Fujitsu Frontech Limited (Japan)

KEY INDUSTRY DEVELOPMENTS

- May 2026: Gyro Hut chose NCR Voyix as its technology partner to support its next growth phase and modernize restaurant operations. The brand plans to migrate to NCR Voyix’s next-generation restaurant POS solution, Aloha Next, once available. This development highlights rising demand for scalable, enterprise-grade POS platforms among fast-casual and expanding restaurant chains.

- October 2025: Zebra Technologies and Salesforce launched a joint Retail Cloud POS on Android solution at Dreamforce 2025. The solution integrates Zebra’s Android mobile devices with Salesforce’s cloud platform to support frontline associates, improve inventory visibility, and streamline store operations. This development shows how mobile POS, cloud POS, and AI-enabled retail workflows are converging in modern stores.

- October 2025: NCR Voyix and Corpay announced a partnership to support commercial fuel transactions through NCR Voyix’s cloud-native POS systems in the U.S. The integration will connect Voyix Connect with Corpay’s Comdata system for fleet card processing. NCR Voyix noted that it supports more than 18,000 fuel stations in the U.S., making this development important for the fuel, fleet, and convenience POS segment.

- September 2025: Global Payments launched its Genius for Enterprise POS solution in the U.S., targeting QSRs, fast-casual restaurants, stadiums, venues, and foodservice management environments. The platform includes POS, kitchen management, back office, payments, drive-thru, kiosks, and digital signage. The company also stated that 51,000 restaurants worldwide use its enterprise technology, supporting its scale in restaurant and venue POS.

- September 2025: Global Payments launched its Genius for Enterprise POS solution in the U.S., targeting QSRs, fast-casual restaurants, stadiums, venues, and foodservice management environments. The platform includes POS, kitchen management, back office, payments, drive-thru, kiosks, and digital signage. The company also stated that 51,000 restaurants worldwide use its enterprise technology, supporting its scale in restaurant and venue POS.

- August 2025: Zebra entered a definitive agreement to acquire Elo Touch Solutions, a provider of kiosks, touchscreen, payment, and POS-related solutions. Elo’s portfolio supports retail, hospitality, QSR, healthcare, and industrial markets, including self-service and payment workflows. The acquisition expands Zebra’s ability to serve modern store, kiosk, self-checkout, and connected frontline use cases.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product/service types, and leading applications of the product. Besides this, it offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Type, Deployment, Operating System, Payment Technology, End-user, and Region |

| By Component |

|

| By Type |

|

| By Deployment |

|

| By Operating System |

|

| By Payment Technology |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 38.57 billion in 2025 and is projected to reach USD 116.26 billion by 2034

In 2025, the Asia Pacific market value stood at USD 13.75 billion.

The market is expected to grow at a CAGR of 13.1% over the forecast period.

By end-user, retail segment led the market in 2025.

The rising adoption of digital payments, mobile wallets, and QR-based transactions to enhance user experience is a key factor driving market growth.

Block, Inc., Toast, Inc., NCR Corporation, PAX Technology, Oracle Corporation, and Ingenico Group are the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 240

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us