Cloud Computing Market Size, Share & Industry Analysis, By Type (Public Cloud, Private Cloud, and Hybrid Cloud), By Service (Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS)), By Enterprise Type (SMEs and Large Enterprises), By Industry (BFSI, IT and Telecommunications, Government, Consumer Goods and Retail, Healthcare, Manufacturing, and Others), and Regional Forecast, 2026-2034

Cloud Computing Market Size & Share

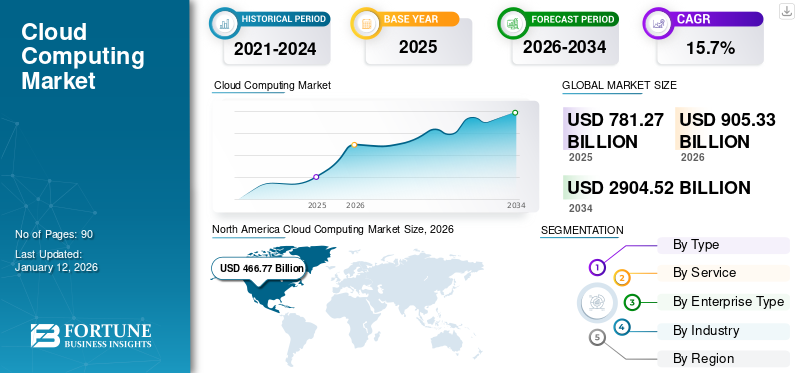

The global cloud computing market size was valued at USD 781.27 billion in 2025 and is projected to grow from USD 905.33 billion in 2026 to USD 2,904.52 billion by 2034, exhibiting a CAGR of 15.7% during the forecast period. North America dominated the cloud computing industry, with a 52.0% market share in 2025. Industry growth is driven by enterprise digital transformation, artificial intelligence integration, hybrid infrastructure adoption, and sustained hyperscale capital investment across developed and emerging economies.

Public cloud deployment remains the primary growth engine, supported by hyperscale providers expanding geographic availability zones. Hybrid architectures are gaining traction as enterprises balance regulatory compliance with operational flexibility. Private cloud investments persist in regulated industries where data governance remains critical. Collectively, these dynamics sustain broad-based cloud computing market growth.

Neocloud platforms are emerging as specialized infrastructure providers focused primarily on GPU cloud environments. Their contribution to total cloud computing market size remains limited; however, their presence is strategically meaningful. GPU cloud has become a strategic differentiator within the cloud computing industry. Capacity allocation, semiconductor supply cycles, and power availability are shaping deployment decisions. Enterprises increasingly evaluate providers based on artificial intelligence readiness, not only on storage or general compute scalability.

Artificial intelligence workloads are materially increasing compute intensity. Enterprises require elastic infrastructure capable of supporting advanced analytics and generative models. Infrastructure as a Service (IaaS) adoption is expanding among organizations seeking capital efficiency. Platform as a Service (PaaS) accelerates application development lifecycles, while Software as a Service (SaaS) continues to dominate recurring enterprise software consumption. Hyperscaler share shifts increasingly reflect access to advanced compute capacity rather than traditional enterprise migration alone. Infrastructure depth, capital discipline, and graphics processing unit availability now directly influence cloud computing market growth.

Cloud computing market share remains concentrated among global hyperscale providers. However, regional vendors and sovereign cloud initiatives are strengthening in response to data localization mandates. Pricing optimization, long-term enterprise contracts, and integrated security frameworks influence competitive positioning. Historically, cloud computing market share expanded through geographic scale, partner ecosystems, and service breadth. While those factors remain relevant, artificial intelligence integration has intensified compute concentration. Providers with sustained investment in GPU clusters, high-bandwidth networking, and energy-efficient data center design are capturing a disproportionate share of incremental demand.

The cloud computing industry is growing due to several major factors, including increasing digital transformation across industries, growing internet and mobile device adoption around the world, and increased usage of big data. As industries undergo modernization, cloud platforms have become indispensable in supporting digital business operations. Furthermore, the implementation of Internet of Things (IoT), edge computing, 5G, and real-time analytics driven by Artificial Intelligence (AI) and Machine Learning (ML) is anticipated to increase the value of cloud computing technology across different businesses. For instance,

- In January 2025, SAP SE integrated AI and Machine Learning (ML) into its enterprise ecosystem to help companies make better data-driven decisions and increase productivity.

Download Free sample to learn more about this report.

Cloud Computing Market Key Takeaways

- 2025 Market Size: USD 781.27 billion

- 2026 Market Size: USD 905.33 billion

- 2034 Forecast Market Size: USD 2,904.52 billion

- CAGR: 15.70% from 2026–2034

- The SaaS segment held the largest market share in 2025.

- The IaaS segment accounted for 26.00% market share in 2025.

- The Large Enterprises segment accounted for a 52.00% market share in 2025.

North America

North America held a 52.00% share in 2025, valued at USD 406.08 billion.

Asia Pacific

Asia Pacific held a 13.30% share in 2025, valued at USD 104.24 billion.

Europe

Europe accounted for a 22.70% share in 2025, valued at USD 177.14 billion.

U.S.

The market projected to reach USD 282.62 billion by 2026.

Japan

The market projected to reach USD 27.86 billion by 2026.

Read More

Market Dynamics

Promising Opportunities in the Cloud Computing Market

The global cloud computing market comprises a vibrant start-up ecosystem. The market is expected to have 100+ start-ups and innovative cloud computing solutions and services for consumers. Such a fragmented market is likely to create intense competition by forcing existing companies to upgrade and continuously adopt new developments in cloud offerings. Hence, increased competition is likely to expand the market, creating more opportunities for market players.

- China: Developing and deploying applications that leverage edge computing to process data and boost IoT devices, autonomous vehicles, and real-time applications will create a new revenue stream for the Chinese market

- India: Implementing AI and ML algorithms on cloud platforms to power predictive analytics, automation, and intelligent applications will create a great opportunity for the Indian market.

Artificial intelligence infrastructure expansion represents a substantial opportunity within the cloud computing market. Enterprises require scalable environments to train and deploy advanced models. Providers offering optimized graphics processing unit clusters and secure data pipelines can capture premium enterprise contracts. Emerging markets offer long-term growth potential. Digital adoption across Southeast Asia, Latin America, and Africa is accelerating. Investments in regional availability zones strengthen competitive positioning and expand global cloud computing market share.

Sovereign cloud initiatives present an additional opportunity. Governments and regulated industries require locally controlled infrastructure environments. Partnerships with domestic operators enable compliance-aligned expansion. Sustainability-driven cloud services are gaining enterprise attention. Providers integrating renewable energy sourcing and carbon reporting tools enhance differentiation. Environmental accountability increasingly influences procurement decisions.

Market Trends

Growing Acceptance of Omni-Cloud over Multi-Cloud to Propel Industry Growth

An Omni-cloud platform offers upgraded connection facilities to businesses, enabling data to be rationalized and integrated across different platforms. By adopting Omni-cloud systems, companies can achieve greater precision in data management while improving operational efficiency. Hence, major players are leveraging strategies, such as new product innovations, partnerships, and mergers & acquisitions, to expand their market presence. For instance,

- In November 2023, Google Cloud and VMware expanded their alliance to integrate AlloyDB Omni on the VMware Cloud Foundation. The tech preview combines the robust proficiencies of AlloyDB Omni and VMware’s Data Services Manager, providing users with a solution to streamline PostgreSQL management, improve existing databases, and modify processes into generative AI applications.

Hybrid and multi-cloud adoption represents a defining trend in the cloud computing market. Enterprises distribute workloads across multiple providers to enhance resilience and optimize pricing. This strategy reduces concentration risk and strengthens negotiation leverage. Artificial intelligence integration is accelerating platform innovation. Cloud providers are embedding machine learning toolkits and generative model infrastructure within core service offerings. High-performance computing clusters are becoming standard across hyperscale environments.

Industry-specific cloud solutions are gaining traction. Providers are tailoring platforms to address regulatory and operational requirements in banking, healthcare, and government sectors. Vertical specialization enhances competitive differentiation. Edge cloud deployment is expanding to support latency-sensitive applications. Telecommunications integration and 5G rollout increase distributed processing requirements. Edge architectures complement centralized hyperscale infrastructure.

Download Free sample to learn more about this report.

Market Drivers

Integration of AI, Machine Learning, and Big Data with Cloud to Fuel Market Progress

The growing adoption of Artificial Intelligence (AI), big data, Machine Learning (ML), and other emerging technologies is anticipated to drive industry growth. Such technologies are reshaping the market landscape by enabling real-time data processing, visualization, and analytics. Various service providers, such as Google, Amazon, Microsoft, and many others, continue to implement artificial intelligence to enhance efficiency and reduce costs in cloud services.

- For instance, in August 2023, Microsoft partnered with Globant to launch an AI and cloud innovation studio, combining Microsoft’s advanced cloud solutions with Globant's expertise in AI-driven digital transformation.

Thus, the rising integration of AI, big data, and ML technologies is anticipated to drive the market’s growth.

Enterprise digital transformation remains the primary driver of cloud computing market growth. Organizations are modernizing legacy systems to improve scalability, cost transparency, and operational resilience. Migration to cloud-native architectures enhances agility and reduces capital expenditure associated with on-premise infrastructure. Artificial intelligence and advanced analytics adoption significantly increase demand for elastic computing environments. Cloud platforms provide on-demand access to high-performance compute clusters and storage resources. Enterprises leverage Infrastructure as a Service to scale workloads dynamically without long-term hardware commitments.

Remote and distributed workforce models continue to support Software as a Service adoption. Collaboration platforms, enterprise resource planning systems, and customer relationship management solutions increasingly operate in cloud environments. This structural shift expands recurring revenue streams across the cloud computing market. Regulatory frameworks encouraging data protection and business continuity planning also influence cloud migration strategies. Providers offer certified compliance environments that reduce enterprise governance complexity. Cybersecurity investment strengthens confidence in multi-cloud deployment models.

Market Restraints:

Data Privacy and Security Concerns to Hamper Market Growth

Customers adopt cloud services to securely store business and personal data on cloud platforms. However, concerns related to data privacy and data breaches, loss of data, unexpected emergencies, application vulnerabilities, and cyberattacks pose significant challenges to the growth of the cloud industry. Cybercrimes, such as cloud malware injection, service or account hijacking, meltdown, and man-in-the-cloud assaults, can expose critical company data, resulting in financial losses and operational disruptions. Cyberattacks also disturb corporate functions, thereby restraining the progress of the market.

- For instance, as per a Thales Cloud Security Study, 2023, more than 39% of businesses encountered a data breach in their cloud environment in 2022, marking a 35% increase from the previous year. Human error was identified as the leading reason for data breaches.

Data sovereignty regulations present structural constraints within the cloud computing market. Cross-border data transfer restrictions require localized infrastructure deployment, increasing compliance complexity. Enterprises operating in multiple jurisdictions must navigate evolving regulatory frameworks. Vendor lock-in concerns limit full-scale migration for certain organizations. Proprietary architectures and integration dependencies increase switching costs. Multi-cloud strategies mitigate concentration risk but add operational complexity.

Cybersecurity risk remains a persistent challenge. As cloud environments scale, threat exposure expands. Organizations must invest in advanced identity management, encryption, and continuous monitoring frameworks. Security breaches can negatively affect a provider's reputation and cloud computing market share. Cost predictability challenges also restrain adoption. While operating expenditure models reduce upfront capital investment, variable usage pricing can create budgeting uncertainty. Enterprises increasingly seek workload optimization tools to manage cloud spending.

Use Cases

|

Infrastructure as a Service (Technology) |

Challenges: Netflix initially relied on traditional data centers, but scaling them became increasingly difficult as the platform’s popularity grew. The physical infrastructure couldn’t keep up with the demands of its global user base, especially as content streaming needed more computational power and storage. Solution: Netflix teamed up with IaaS providers such as Amazon Web Services to host its content streaming services. By using cloud infrastructure, Netflix can dynamically scale its resources based on demand, ensuring seamless content delivery to users globally. |

|

Retail (Industry) |

Challenges: Maintaining an on-premise infrastructure required constant investment in hardware, software, and IT personnel. As Walmart’s operations expanded globally, this became increasingly expensive, particularly with data centers that needed constant monitoring and updates. Solution: Walmart adopted cloud platforms such as Microsoft Azure to integrate its online and offline systems, enabling a seamless omnichannel experience. Now, customers can shop on Walmart’s website and mobile app while receiving real-time updates. |

IMPACT OF GENERATIVE AI:

Implementation of Generative AI Capabilities Across Cloud Infrastructure to Fuel Market Expansion

Generative AI can transform cloud investment and returns, creating numerous growth opportunities for market players. Cloud infrastructure supports generative AI’s innovations, enabling enterprises to improve threat detection, data augmentation, data anonymization, tech democratization, and cybersecurity. End-to-end, generative AI-driven workflows allow enterprises to migrate their transactional applications to the cloud, optimizing efficiency.

- For instance, according to industry experts, generative AI can provide around 75-110% points of Return on Investment (ROI) to cloud programs. Its key benefits include minimizing the cost and time of application migration and remediation, creating new business use cases, and improving the efficiency of application expansion and cloud infrastructure.

Leading vendors are increasingly using generative AI to improve operational intelligence and scalability in the cloud computing sector. Predictive resource allocation, dynamic workload management, and cost optimization are made possible by the incorporation of large language models (LLMs) and AI automation into cloud systems. This development gives businesses real-time flexibility for complex data environments while also bolstering the effectiveness of the global cloud services market. Therefore, over the course of the forecast period, it is anticipated that the generative AI and cloud platforms will significantly increase the size of the cloud computing market and further solidify the market share of major players.

Get comprehensive study about this report by, Download free sample copy

Source: Forrester September 2024 Artificial Intelligence Pulse Survey

CLOUD COMPUTING MARKET SEGMENTATION ANALYSIS

By Type Analysis

Public Cloud Segment Dominated Owing to Rising Cost-Efficient Solution of Cloud Computing

Based on type, the market is categorized into public cloud, private cloud, and hybrid cloud.

Public Cloud

The public cloud segment is expected to lead the market, contributing 55.88% globally in 2026, driven by the rising demand for secure, scalable, and cost-efficient solutions. Further, it is driven by factors such as digital transformation and increasing data storage needs by users in major countries.

The growing adoption of multi-cloud strategies by enterprises to ensure flexibility and avoid vendor lock-in is expected to further boost the demand for public cloud infrastructure. The expanding global cloud services market, driven by hyperscalers such as AWS, Microsoft Azure, and Google Cloud, continues to shape the competitive dynamics of the cloud computing industry.

Public cloud represents the largest contributor to the global cloud computing market growth. Enterprises leverage shared infrastructure operated by third-party providers to achieve elastic scalability and consumption-based pricing. Public cloud platforms offer standardized service catalogs, global availability zones, and integrated security frameworks. Hyperscale expansion continues to reinforce geographic coverage and workload migration momentum.

The public cloud model supports rapid deployment of analytics, artificial intelligence, and application modernization initiatives. Infrastructure optimization and automation capabilities enhance operational efficiency. However, regulatory exposure and data residency requirements influence adoption patterns in highly regulated industries. Despite these constraints, public cloud maintains a dominant cloud computing market share due to cost efficiency and global scalability advantages.

Private Cloud

Private cloud environments provide dedicated infrastructure for single organizations, either on-premise or hosted externally. Enterprises with stringent compliance, latency, or security requirements continue to deploy private cloud architectures. This segment is particularly relevant in banking, government, and defense sectors.

Private cloud adoption emphasizes control, governance, and predictable performance. Capital expenditure remains higher compared to public cloud models, but operational oversight and customization justify investment. While private cloud contributes a smaller proportion of the overall cloud computing market size, it remains strategically significant for regulated industries and hybrid strategies.

Hybrid Cloud

The hybrid cloud segment is predicted to record a leading CAGR during the forecast period due to the increasing usage of cloud-driven solutions and the added benefits of the cloud platform over public and private clouds. These benefits include minimized costs, improved control and scalability due to the integration of both private and public clouds, and improved security and risk.

- For instance, in December 2023, Lenovo, in partnership with Intel, announced the launch of a hybrid cloud platform and services. ThinkAgile, the hybrid cloud solution, enhances the performance of Artificial Intelligence and the quickness of cloud solutions by providing more computing power and better memory to its product line.

Hybrid cloud integrates public and private environments, enabling workload portability and risk diversification. This model is expanding rapidly as enterprises seek to balance compliance with scalability. Hybrid deployment supports phased migration strategies and mitigates vendor concentration risk.

Interoperability tools and unified management platforms are central to hybrid expansion. Enterprises increasingly design cloud strategies around workload optimization rather than platform exclusivity. Hybrid cloud is expected to contribute meaningfully to long-term cloud computing market growth as regulatory and operational complexity increases.

By Service Analysis

Rising Need for Easy Deployment Models to Increase the Use of Software as a Service (SaaS)

By service, the market is segmented into Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS).

Software as a Service (SaaS)

The Software as a Service (SaaS) segment held the highest market share in 2024, due to its ease of deployment, lower maintenance costs, and lower cost of ownership. These features will give new market opportunities for SaaS in different regions, including North America, APAC, and European countries.

The SaaS model continues to be a major contributor to the global cloud computing market size, accounting for substantial revenue generation across verticals such as education, healthcare, and retail. The proliferation of remote work and cloud-native business applications is accelerating the demand for SaaS solutions, particularly in enterprise collaboration tools and CRM platforms. This sustained demand underpins the long-term scalability and innovation potential within the cloud services market.

Software as a Service dominates recurring enterprise software consumption. SaaS platforms deliver subscription-based applications across finance, human resources, collaboration, and customer management functions. Enterprises benefit from continuous updates, security management, and predictable cost structures. SaaS penetration remains high across SMEs and large enterprises. Industry-specific SaaS solutions are expanding in healthcare, retail, and manufacturing. Although margins vary by application complexity, SaaS remains a stable and scalable contributor to cloud computing market growth.

Infrastructure as a Service (IaaS)

Infrastructure as a Service (IaaS) will grow at the highest rate during the forecast period (2026-34), along with holding 26% market share in 2025, as it minimizes initial investment costs by eliminating the need for on-site data centers and reducing ongoing service and maintenance costs. Moreover, the rise of digitization, along with the increasing adoption of cloud computing services, is a key driver of the cloud computing market growth.

Infrastructure as a Service forms the foundational layer of the cloud computing market. IaaS delivers compute, storage, and networking resources on demand. Enterprises adopt IaaS to avoid capital-intensive hardware procurement and to enable dynamic workload scaling.

Artificial intelligence, high-performance computing, and enterprise application hosting significantly expand IaaS demand. Providers differentiate through pricing models, performance optimization, and geographic footprint. IaaS represents a substantial portion of the global cloud computing market size and directly influences hyperscale capital investment cycles.

Platform as a Service (PaaS)

The Platform as a Service (PaaS) is estimated to hit a CAGR of 17.06% during the forecast period. New developments like serverless computing and container orchestration are altering the PaaS environment and helping the cloud industry as a whole grow. Platform as a Service supports application development and deployment through integrated toolkits and runtime environments. Developers leverage PaaS to accelerate innovation cycles and reduce infrastructure management complexity. This model enhances productivity and shortens time-to-market.

PaaS adoption is particularly strong among digital-native enterprises and technology-focused organizations. Integration with analytics, artificial intelligence services, and container orchestration platforms strengthens ecosystem lock-in. PaaS growth contributes to long-term cloud computing market share concentration among providers offering comprehensive developer ecosystems.

By Enterprise Type Analysis

The SMEs Segment is expected to dominate due to increased product Adoption among SMEs

Based on enterprise type, the market is bifurcated into SMEs and large enterprises.

SMEs

The SMEs segment is projected to display the highest CAGR of 18.78% during the forecast period, as cloud technology has revolutionized the operations of small and medium-sized enterprises. It helps SMEs decrease spending on expensive hardware and software by offering flexible payment options, such as a pay-as-you-go model, thereby reducing overall costs. Moreover, various market players are introducing new cloud solutions designed for SMEs, driving adoption.

For instance, DE-CIX and BasicBrix collaborated to leverage cloud computing solutions for SMEs in Malaysia. With the unification of hassle-free computing services of BasicBrix and high-performance and secure direct connections of DirectCLOUD, a service offered by DE-CIX, Malaysian start-ups and SMEs can take advantage of these solutions.

Small and medium enterprises (SMEs) represent a rapidly expanding segment within the cloud computing market. Limited internal information technology infrastructure encourages SMEs to adopt subscription-based cloud solutions. SaaS and IaaS offerings enable cost predictability and operational flexibility.

Cloud adoption among SMEs is often incremental, beginning with collaboration tools and financial software before expanding into infrastructure services. Providers targeting SMEs emphasize ease of deployment and bundled service offerings. SME demand supports diversified revenue streams across the cloud computing industry.

Large Enterprises

The large enterprises segment accounts for the highest market share of 52% in 2025 as cloud technology enhances operational efficiency, offers better scalability, and drives widespread adoption among large enterprises. Large enterprises account for a significant proportion of the total cloud computing market size. Migration strategies often involve complex, multi-year transformation programs. Hybrid and multi-cloud architectures are common among global corporations seeking resilience and regulatory compliance.

Enterprise contracts are typically long-term and high-value. Providers compete through customized service agreements, dedicated support teams, and advanced security frameworks. Large enterprise adoption materially influences overall cloud computing market growth trajectories.

By Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Higher Adoption of Cloud Solutions Propels IT & Telecommunications Industry Expansion

Based on industry, the market is distributed into BFSI, IT and telecommunications, government, consumer goods and retail, healthcare, manufacturing, and others.

BFSI

Banking, financial services, and insurance represent a critical vertical within the cloud computing market. Institutions require secure environments, disaster recovery capabilities, and regulatory compliance alignment. Hybrid cloud models are prevalent in this segment.

IT and Telecommunications

The IT and telecommunications segment holds the largest market share of 25% in 2025 due to the rising popularity of cloud-powered computing solutions in different organizations. With the help of this technology, telecommunication service providers and operators can store and calculate customer data, build cloud data warehouses, transfer cloud data, manage other cloud-based telecommunication services autonomously, access tele services with the help of the cloud, and much more. Moreover, various market players are collaborating and forming alliances with telecom providers to drive business growth.

- For instance, in February 2023, Airtel announced a strategic alliance with Vultr to provide cloud solutions to businesses in India. These cloud solutions are hosted at Airtel’s data centers across Mumbai, Bangalore, and Delhi-NCR, allowing businesses to measure their digital functions globally.

IT and Telecommunications drive hyperscale infrastructure demand. Cloud-native application hosting, content delivery, and network virtualization increase compute intensity. This vertical significantly shapes the global cloud computing market share distribution.

Healthcare

The healthcare segment is projected to record the highest CAGR of 19.04% during the forecast period. The segment’s growth can be attributed to the increased deployment of mobile applications, cloud-based software, wearable healthcare tools, and smart healthcare apparatus. Additionally, the healthcare industry's cloud computing market is expanding due to the rise in telemedicine, AI-driven diagnostics, and electronic health records (EHRs).

Manufacturing

Manufacturing integrates cloud platforms with industrial Internet of Things ecosystems and predictive maintenance systems. Hybrid architectures support operational continuity and edge connectivity.

Regional Insights

North America Cloud Computing Market Analysis

North America Cloud Computing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the North America market stood at USD 406.08 billion, representing 52.00% of global demand, and is expected to reach USD 466.77 billion in 2026. North America will account for the highest market share during the forecast period owing to the early adoption of high-tech technologies, such as AI, Blockchain, robotics, the Internet of Things (IoT), and the cloud. The major presence of leading cloud providers, such as IBM Corporation, Oracle Corporation, and Microsoft Corporation, will further contribute to the adoption of cloud in the region. The U.S. market stands at USD 282.62 billion in 2026.

- For instance, in September 2023, Oracle announced a partnership with TELMEX-Triara and became the first hyperscaler with two cloud regions in Mexico. Enterprises benefit from Oracle’s Cloud Infrastructure (OCI), which enhances performance, strengthens security, and provides advanced analytics and distributed cloud proficiencies.

North America leads the cloud computing market, supported by hyperscale infrastructure density and enterprise digital maturity. Strong capital expenditure from major providers sustains the regional cloud computing market size expansion. Enterprises prioritize artificial intelligence integration, cybersecurity investment, and hybrid deployment models. Regulatory clarity and advanced connectivity infrastructure reinforce regional cloud computing market growth across financial services, healthcare, and technology sectors.

United States Cloud Computing Market

The United States dominates the regional cloud computing market share, driven by hyperscale concentration and enterprise innovation spending. Large enterprises continue migrating mission-critical workloads to multi-cloud environments. Artificial intelligence infrastructure investments accelerate compute demand. Federal modernization programs and private sector digital transformation initiatives sustain consistent cloud computing market growth across verticals, including banking, retail, and advanced manufacturing.

To know how our report can help streamline your business, Speak to Analyst

Europe Cloud Computing Market Analysis

The Europe region captured 22.70% of the global market in 2025, generating USD 177.14 billion in revenue, and is expected to reach USD 205.63 billion in 2026. Government initiatives and investments to improve cloud adoption and implementation will fuel the market’s growth across European countries. Additionally, private corporations are accelerating cloud adoption through growing investments and business expansions.

- For instance, in December 2023, the European Commission approved financial aid worth USD 1.2 billion for cloud computing projects in the region. The project, named IPCEI CIS (Next Generation Cloud Infrastructure and Services), was developed by seven European Union states, including France, Poland, Hungary, Germany, Italy, the Netherlands, and Spain.

Europe demonstrates steady cloud computing market growth supported by regulatory modernization and sovereign cloud initiatives. Data protection requirements influence hybrid and localized deployment strategies. Regional providers compete alongside global hyperscalers. Industrial digitization across the manufacturing and automotive sectors strengthens infrastructure demand. European enterprises emphasize compliance-certified environments, reinforcing structured and risk-managed cloud computing market expansion.

United Kingdom Cloud Computing Market

The market in the U.K. stands at USD 55.20 billion, along with France, estimated to hit USD 22.77 billion, and the German market is expected to reach USD 53.94 billion in 2026. The United Kingdom maintains a strong position within the European cloud computing market. Financial services institutions accelerate migration toward secure, scalable environments. Government cloud-first policies stimulate public sector modernization. Start-up ecosystem expansion supports Software as a Service adoption. Despite economic volatility, digital investment continues to sustain stable cloud computing market growth.

Germany Cloud Computing Market

Germany represents a major contributor to the European cloud computing market size. Industrial digitization and Industry 4.0 initiatives accelerate cloud-based analytics and automation adoption. Data sovereignty considerations drive demand for localized data centers. Enterprises prioritize hybrid cloud architectures to align with regulatory frameworks. Manufacturing and automotive sectors significantly influence the national cloud computing market growth.

Asia-Pacific Cloud Computing Market Analysis

Asia Pacific maintained a strong presence in the global market, reaching USD 104.24 billion in 2025, accounting for 13.30% share, and is expected to reach USD 123.4 billion in 2026, driven by the rising demand for cloud-based solutions in telecommunications and healthcare sectors. The cloud computing industry in China holds USD 39.94 billion, along with India, estimated to hit USD 20.70 billion, and the Japanese market accounting for USD 27.86 billion in 2026.

- For instance, in February 2023, Tech Data introduced cloud services in Australia, offering customized solutions for AWS and Microsoft’s IaaS (Infrastructure as a Service) and PaaS (Platform as a Service) business models.

Asia-Pacific exhibits high cloud computing market growth driven by rapid digital adoption and expanding internet penetration. Hyperscale providers increase regional availability zones to support enterprise migration. Government digital infrastructure programs enhance connectivity. E-commerce expansion and fintech innovation strengthen demand. Regional competition intensifies as domestic providers expand market share.

Japan Cloud Computing Market

Japan’s cloud computing market reflects strong enterprise modernization and automation initiatives. Manufacturing and robotics integration increase infrastructure demand. Regulatory compliance requirements encourage hybrid cloud adoption. Enterprises emphasize resilience and cybersecurity investment. Artificial intelligence-driven analytics adoption supports ongoing cloud computing market growth across industrial and financial sectors.

China Cloud Computing Market

China represents one of the fastest-growing cloud computing market segments globally. Domestic hyperscale providers dominate market share, supported by regulatory frameworks and state-backed digital initiatives. Rapid e-commerce and fintech expansion drive infrastructure demand. Data localization policies shape competitive dynamics. Enterprise cloud adoption continues to expand across the manufacturing and technology industries.

Middle East & Africa

The Middle East & Africa market accounted for USD 53.87 billion in 2025, representing 6.90% of the global industry, and is expected to reach USD 62.85 billion in 2026. The region’s progress is attributed to improved investments in developing technologies, such as 5G, Machine Learning (ML), Big Data, Artificial Intelligence (AI), and cloud computing, by the governments of Israel, the GCC countries, and Turkey. The GCC countries are projected to reach a value of USD 19.45 billion in 2025.

Latin America Cloud Computing Market Analysis:

In 2025, Latin America represented USD 39.93 billion, accounting for 5.10% of the worldwide market, and is expected to reach USD 46.68 billion in 2026. Latin America demonstrates emerging cloud computing market growth supported by digital banking expansion and telecommunications modernization. Regional enterprises prioritize cost-efficient infrastructure models. Data center investment increases across major economies. Regulatory development remains uneven, influencing deployment strategies. Market share distribution gradually diversifies as global providers strengthen regional partnerships. The cloud computing industry in South America is in an evolving phase, owing to the increased use of smartphones, laptops, and the internet. The need to store and process huge volumes of data has increased significantly, allowing businesses to provide customer-centric services to their customers, driving market growth.

Middle East & Africa Cloud Computing Market Analysis:

The Middle East and Africa region shows an expanding cloud computing market size driven by smart city initiatives and public sector digitization. Investment in localized data centers increases regional competitiveness. Energy and government sectors anchor demand. Infrastructure modernization and cybersecurity investment contribute to steady cloud computing market growth across selected economies.

Cloud Computing Industry Competitive Landscape

Key Market Players

Key Players to Focus on Advanced Solutions to Strengthen Their Market Positions

Key market players are working on creating a wide variety of distributed cloud solutions to address the needs of customers and organizations. The introduction of innovative solutions helps companies increase their business expertise. In addition, the upgrading and expansion of existing product portfolios will improve vendors’ market position.

The cloud computing industry remains highly concentrated among global hyperscale providers. Market share is dominated by vertically integrated platforms offering Infrastructure as a Service, Platform as a Service, and Software as a Service within unified ecosystems. Competitive advantage is primarily defined by capital intensity, global availability zones, artificial intelligence infrastructure capacity, and integrated security architecture.

Leading providers focus on long-term enterprise contracts and recurring revenue optimization. Pricing strategies balance consumption-based flexibility with reserved capacity commitments. Multi-year agreements enhance revenue visibility and strengthen retention metrics. Competitive positioning increasingly depends on hybrid integration capabilities and workload portability frameworks.

Artificial intelligence acceleration represents a major competitive differentiator. Providers investing in advanced graphics processing unit clusters and machine learning services capture high-value enterprise workloads. Strategic partnerships with semiconductor manufacturers reinforce compute performance advantages. Sovereign cloud and compliance-certified environments represent another area of differentiation. Providers collaborate with domestic operators to address regulatory requirements and data localization mandates. This strategy expands the addressable cloud computing market share within regulated sectors.

Emerging regional players compete through localized pricing, regulatory alignment, and niche specialization. While scale disadvantages persist, targeted vertical solutions support market entry. Mergers and acquisitions remain active within platform integration and cybersecurity domains. Providers expand service portfolios to enhance ecosystem stickiness. Operational efficiency, automation, and sustainability initiatives further shape competitive dynamics.

List of Top Cloud Computing Companies:

|

Cloud Computing Large Companies |

Cloud Computing SMEs |

|

· Amazon Web Services, Inc. (U.S.) · Oracle Corporation (U.S.) · IBM Corporation (U.S.) · Alibaba Group Holdings Limited (China) · Microsoft Corporation (U.S.) · VMware, Inc. (U.S.) · Google LLC (U.S.) · SAP SE (Germany) · Salesforce, Inc. (U.S.) · Rackspace Technology, Inc. (U.S.) · And More… |

· ScaleWay (France) · Turkcell Cloud (Turkey) · Vargonen (Turkey) · CtrlS Datacenters (India) · Linx Cloud (Brazil) · Netmagic Solutions (India) · Sentia (Netherlands) · Cegeka (Belgium) · CloudVPS (Netherlands) · UOL Diveo (Brazil) · And More… |

Latest Cloud Computing Industry Developments:

- February 2025: Accenture collaborated with Google Cloud to accelerate the adoption of generative AI and cloud solutions in Saudi Arabia. The initiative aims to help enterprises unlock new business opportunities, improve customer experiences, enhance modern digital core, and scale generative AI agents.

- February 2025: Alibaba Cloud expanded regional availability zones across Southeast Asia to increase cloud computing market share, focusing on e-commerce scalability, fintech workloads, and localized regulatory compliance frameworks.

- April 2025: Oracle Cloud Infrastructure launched enhanced high-performance computing clusters targeting enterprise artificial intelligence and database workloads, strengthening competitive positioning through optimized networking architecture and enterprise-grade security enhancements.

- January 2024: Microsoft and Vodafone signed a ten-year strategic alliance to bring generative AI, cloud, and digital services to over 300 million consumers, businesses, and public sector organizations across Africa and Europe. This collaboration enables Vodafone to leverage Microsoft’s generative AI to enhance customer experiences, build new digital and financial facilities for enterprises, and overhaul its global data center cloud strategy.

- January 2024: IBM collaborated with American Tower to introduce edge cloud services, driving innovation and improving customer experiences. The company aims to fast-track the progress of multi-cloud and hybrid cloud computing platforms at the edge.

- November 2023: Udemy collaborated with Google Cloud as an initial member of its new cloud-driven content program. The partnership addresses the increasing demand for cloud computing expertise across the globe.

- February 2023: Akamai Technologies, Inc. announced the launch of the Connected Cloud platform for content delivery, security, and cloud computing to preserve applications and avoid threats.

CLOUD COMPUTING INDUSTRY INVESTMENT ANALYSIS AND OPPORTUNITIES

Key players are focusing on Research and Development (R&D) activities to develop a comprehensive range of cloud computing offerings to meet the customers' and organizations' needs. In January 2025, Microsoft invested USD 3 billion in AI and cloud computing in India. Furthermore, the launch of advanced cloud computing solutions assists players in sustaining their business competence. The enhancement and expansion of the existing product portfolio uplift the position of vendors in the market.

CLOUD COMPUTING INDUSTRY REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, service types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 15.7% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

Type, Service, Enterprise Type, Industry, and Region |

|

Segmentation |

By Type

By Service

By Enterprise Type

By Industry

By Region

|

|

Companies Profiled in the Report |

Amazon Web Services Inc. (U.S.), Oracle Corporation (U.S.), IBM Corporation (U.S.), Alibaba Group Holding Limited (China), Microsoft Corporation (U.S.), VMware, Inc. (U.S.), Google LLC (U.S.), Rackspace Technology, Inc. (U.S.), SAP SE (Germany), and Salesforce, Inc. (U.S.) |

Frequently Asked Questions

The market is projected to reach USD 2,904.52 billion by 2034.

In 2025, the market was valued at USD 781.27 billion.

The market is projected to grow at a CAGR of 15.7% during the forecast period.

By industry, IT and telecommunications segment leads by holding the largest market share.

Integration of AI, machine learning, and big data with cloud is a key factor driving market growth.

Amazon.com Inc., Oracle Corporation, Microsoft Corporation, and IBM Corporation are the top players in the market.

North America is expected to hold the highest market share.

- 2021-2034

- 2025

- 2021-2024

- 90

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us