Software as a Service (SaaS) Market Size, Share & Industry Analysis, By Deployment Type (Public, Private, and Hybrid), By Application (Customer Relationship Management (CRM), Enterprise Resource Planning (ERP), Content, Collaboration, & Communication, BI & Analytics, Human Capital Management, and Others), By Enterprise Type (Large Enterprises and SMEs), By Industry (BFSI, IT & Telecom, Education, Retail & Consumer Goods, Healthcare, Education, Manufacturing and Others), and Regional Forecast, 2026-2034

GLOBAL SOFTWARE AS A SERVICE (SAAS) MARKET: GROWTH DRIVERS, TRENDS, AND FUTURE OUTLOOK

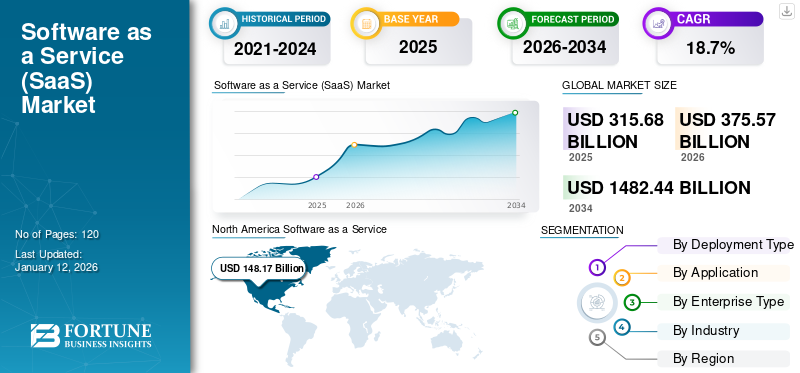

The global Software as a Service (SaaS) market size was valued at USD 315.68 billion in 2025. The market is projected to grow from USD 375.57 billion in 2026 to USD 1,482.44 billion by 2034, exhibiting a CAGR of 18.7% during the forecast period. North America dominated the global market with a share of 46.9% in 2025.

The growth of the Software as a Service market can be attributed to several factors, such as integration with other tools, rise in adoption of public and hybrid cloud-based solutions, and centralized data-driven analytics. According to industry experts, in 2023, 73% organizations used SaaS applications. This percentage is growing as more companies move to the cloud, driven by benefits such as cost efficiency, scalability, and remote work capabilities.

The spread of the COVID-19 pandemic severely impacted the global economy as lockdown measures were implemented to control the spread of the virus. People were confined to their homes to minimize human contact. The rapid spread of the outbreak led IT companies to adopt remote work policies, increasing the need for various software as a service solutions. For instance, the increasing use of Microsoft Office 365 during the COVID-19 pandemic period propelled the growth of the market.

Download Free sample to learn more about this report.

Software as a Service Market KEY TAKEAWAYS

- 2025 Market Size: USD 315.68 Billion

- 2026 Market Size: USD 375.57 Billion

- 2034 Forecast Market Size: USD 1,482.44 Billion

- CAGR: 18.7% from 2026–2034

- North America dominated the SaaS market with a 46.90% share in 2025.

- The Public segment is expected to account for 65.81% of the market in 2026.

- The Content, Collaboration & Communication segment is projected to hold a 29.19% market share in 2026.

North America

North America accounted for USD 148.17 billion in 2025 and is projected to reach USD 172.68 billion in 2026.

Asia Pacific

Asia Pacific generated USD 69.43 billion in 2025 and is expected to reach USD 86.06 billion in 2026.

Europe

Europe accounted for USD 60.04 billion in 2025 and is projected to reach USD 70.81 billion in 2026.

U.S.

The SaaS market is projected to reach USD 141.06 billion in 2026.

Japan

The SaaS market is projected to reach USD 17.05 billion in 2026.

Read More

THE IMPACT OF GENERATIVE AI ON SAAS: AUTOMATION, PERSONALIZATION, AND ENHANCED EFFICIENCY

Generative AI is transforming the software as a service landscape and offers several benefits, ranging from automation, personalized user experiences, and enhanced operational efficiency. It is driving innovation, reshaping business models, and improving productivity across industries. Generative AI can automate various tasks in SaaS platforms, reducing the manual effort required for certain processes, enhancing operational efficiency, and lowering costs. For instance, SaaS companies in content management, marketing, or customer engagement leverage generative AI to create personalized content automatically. Platforms such as Jasper (formerly Jarvis) and Writesonic leverage Artificial Intelligence (AI) to produce marketing copy, blog posts, or product descriptions, automating traditionally time-consuming tasks. Tools such as GitHub Copilot and Tabnine integrate AI to assist developers by generating code suggestions or even entire code blocks, speeding up software development and debugging. As per industry experts, in 2023, AI automated up to 30% of all coding tasks, significantly reducing development time and increasing productivity.

Generative AI allows businesses to offer highly personalized experiences for users. This can range from personalized dashboards and product recommendations to tailored customer support. According to a Salesforce report, 70% of customers expect companies to deliver personalized interactions, and 69% of customers are willing to share personal information in exchange for a more personalized experience. Industry experts predicts that by 2026, 75% of SaaS companies will implement AI-driven automation for at least one major business process, underscoring the scalability benefits.

MARKET DYNAMICS

Market Trend

Rise of Micro Saas: Niche Solutions Driving Growth And Profitability In The SaaS Market

The micro SaaS trend is gaining significant momentum within the broader SaaS ecosystem. Micro SaaS refers to small, niche-focused SaaS businesses that cater to specific sectors or solve particular problems. According to a SaaS industry report, in 2023, approximately 41% of SaaS startups reported focusing on niche markets as a core part of their business strategy, up from only 18% five years ago. Micro SaaS provides specialized tools or services tailored to a targeted customer base. These micro SaaS businesses often have faster development cycles, lower overhead costs, and greater flexibility. They can quickly adapt to customer needs and deliver customized solutions. Established companies and investors are increasingly looking to acquire small but profitable Micro SaaS businesses for their niche customer bases and steady cash flow. In 2022 alone, the number of acquisitions in the SaaS space increased by 16%, with many focused on small-scale SaaS products.

Micro SaaS businesses leverage automation to reduce operational costs. Tools such as Zapier, Integromat, and other automation platforms allow micro SaaS businesses to streamline repetitive tasks, which leads to high margins and low customer acquisition costs. According to The 2023 SaaS Metrics Report, Micro SaaS companies have an average 70% to 80% profit margin, largely driven by low operational costs and automation. Micro SaaS businesses differentiate themselves by providing high-touch, personalized customer support, which enhances retention rates. Micro SaaS companies often achieve an net promter score of 50+, indicating high customer satisfaction. Many Micro SaaS businesses actively take customer feedback and implement customer-driven improvements.

Thus, popularity of micro-SaaS will create the Software as a Service (SaaS) market growth opportunities.

Download Free sample to learn more about this report.

Market Drivers

Rising Adoption of Multi-Cloud and Hybrid Cloud Strategies Driving SaaS Market Growth

As businesses strive for greater flexibility, reliability, and cost-effectiveness, the adoption of multi-cloud and hybrid cloud environments is increasing in the market. Enterprises are avoiding vendor lock-in by spreading their workloads across multiple cloud providers (e.g., AWS, Google Cloud, and Microsoft Azure). Market vendors are adapting their solutions to ensure seamless operation across different cloud platforms. Hybrid cloud adoption allows businesses to leverage both on-premise infrastructure and public cloud services. Service providers are integrating their platforms to support hybrid environments, offering customers greater flexibility.

Therefore, increasing demand for multi-cloud and hybrid cloud is driving the software as a service (SaaS) market growth.

Market Restraints

Addressing SaaS Security Challenges: The Rising Risk of Misconfigurations and Data Vulnerabilities

Professionals store both business-sensitive and personal data on software as a service platforms, making security a significant concern for business professionals. Several enterprises in the industry have identified software as a service misconfiguration as a major challenge.

Furthermore, configuration of internal application setup is becoming a major challenge for security teams. The misconfigurations result in the loss of sensitive data and apprehensive application programming interfaces, leading to unauthorized admission of sensitive data.

- For instance, in April 2022, according to Cloud Security Alliance (CSA), SaaS misconfigurations were responsible for up to 63% of security incidents. At least 43% firms had reported dealing with one or more security incidents due to misconfiguration. The primary cause for misconfigurations is the lack of clarity on changes in the security settings, with several departments having access to SaaS security settings.

Market Opportunity

The Rise of SaaS Superapps: Transforming User Experiences and Business Monetization

The demand for SaaS superapps is growing as they provide end users with a set of core features and the ability to create mini-apps independently. A superapp serves as a platform that delivers consistent and personalized app experiences, offering significant competitive advantages to its providers. More than just an application that combines multiple features and services in one interface, a superapp is a composable application and architecture, allowing the integration of various unrelated functionalities into a single platform. This trend is expected to gain even more momentum in 2025, particularly in the SaaS B2B landscape, where more businesses are anticipated to develop a “One API for all” approach by unifying several APIs into a single solution.

Superapps provide businesses with opportunities to monetize through in-app advertising by displaying ads to an engaged user base. They enable companies to deliver more comprehensive and personalized experience for their customers. Market players are focusing on launching superapp to support businesses across various industries, allowing them to enhance their products and services, target advertising more effectively, and increase conversion rates. Several superapps have been launched by companies, for instance,

- WeChat: A Chinese superapp developed by Tencent that provides a variety of services, including messaging, social media, e-commerce, and mobile payments. With over 1 billion active users, it has become an essential tool for daily life in China.

- Gojek: It's an Indonesian superapp that offers a wide range of services, such as ride-hailing, food delivery, and mobile payments. It has over 150 million active users and has become an essential tool for daily life in Indonesia.

- Paytm: India's superapp offers a wide range of services, including mobile payments, online shopping, and bill payments. It has over 350 million active users and has become an essential tool for daily life in India.

- Kakao: This South Korean superapp offering services including messaging, social media, and mobile payments. It has over 50 million active users and has become an essential tool for daily life in South Korea.

Thus, SaaS superapp is expected to create lucrative opportunities for key vendors operating in the market.

SEGMENTATION ANALYSIS

By Deployment Type

Hybrid Cloud Adoption Surges as Organizations Seek Flexibility and Security

Based on deployment type, the market is categorized into public cloud, private cloud, and hybrid cloud.

The hybrid deployment model is projected to experience the highest compound annual growth rate (CAGR) during the forecast period. This growth is primarily driven by the increasing adoption of hybrid cloud solutions among government agencies, public sector organizations, banking and financial institutions, and others. Furthermore, cloud policies are evolving worldwide in response to the growing demand for cloud services.

- For example, in 2023, Cloud First policy was replaced by “Cloud Smart3” in many regional and national governments to meet the increased demand for flexibility, visibility, speed, advanced security, and control across different environments.

According to a survey conducted by Microsoft in January 2022, 86% of the U.S.-based respondents were planning to increase their investment in hybrid cloud and multi cloud.

The Public segment is expected to lead the market, contributing 65.81% globally in 2026. Public deployment type dominated the market with most Banking, Financial Services and Insurance (BFSI) sector companies already shifted or upgraded to public cloud from their existing on-premise self-hosting banking solutions.

By Application Analysis

Rising Adoption of Content Collaboration and BI & Analytics Solutions in SaaS Market

Based on application, the market is segmented into Customer Relationship Management (CRM), ERP, content, collaboration & communication, BI & analytics, human capital management, and others (HRM, operations management).

The Content, Collaboration & Communication segment will account for 29.19% market share in 2026. Deploying these solutions in content collaboration tools can streamline data flow for content creation, collaborative processes, modification, versioning, and sharing activities of organizations. According to a study by Forbes in 2022, around 73% of companies plan to increase collaboration, considering it an essential part of a project’s success.

BI & analytics is estimated to grow significantly in coming years, as BI & analytics tools offer customizable dashboards and reporting features that can be tailored to specific business needs. BI tools help organizations establish and track key performance indicators (KPIs), ensuring accountability and driving performance improvement across the board. Analytics ensures transparency within the organization as stakeholders can easily access performance data and insights.

By Enterprise Type

Growing SaaS Adoption Among SMEs Due to Cost-Effectiveness and Scalability

Based on enterprise type, the market is bifurcated into large enterprises and SMEs.

The small and medium-sized enterprises (SMEs) are expected to experience significant CAGR of 21.90% during the forecast period. The on-demand software delivery model has transformed the IT landscape and has been widely adopted by SMEs. Due to their limited budgets, SMEs often cannot afford the initial capital expenditures or ongoing service and maintenance costs associated with traditional IT infrastructures. This makes software as a service an attractive option, as it is cost-effective, readily available, and scalable. Additionally, investments in product development are also driving the demand for these solutions. For instance,

- In April 2023, Taclia, a software as a service startup, announced a solution to digitize everyday management processes. The company secured USD 6.7 million in funding to scale the development of its solution.

The Large Enterprises segment is expected to account for 60.40% of the market in 2026. By using SaaS applications, large enterprises can enhance operational efficiency, reduce costs, and increase agility while staying competitive in a rapidly changing market.

These factors are expected to boost the software as a service market share.

By Industry

To know how our report can help streamline your business, Speak to Analyst

Healthcare Sector to Experience Highest SaaS Growth, While IT & Telecom Leads Market Share

Based on industry, the market is segmented into IT & telecom, BFSI, retail & consumer goods, healthcare, education, manufacturing, and others.

The Healthcare segment is anticipated to hold a dominant market share of 23.37% in 2026 and predicted to record the highest CAGR of 26.00% during the projected period. Healthcare professionals are migrating application and storage to the cloud to enable hybrid and remote working. Cloud services help medical professionals gain real-time health data insights and minimize the complexities within an IT system with simplified storage solutions. Rapid advancement in telemedicine technologies, such as video/audio conferencing, telesurgery, and teleradiology, will drive the adoption of cloud services.

- For instance, May 2021, HCA Healthcare, an American healthcare company, partnered with Google Cloud. Through this partnership, the companies aimed to build an advanced analytics platform and develop machine learning models for workflow improvements and science-informed decision support.

IT & telecom dominated the market in 2024. As per PwC survey, around 84% of IT executives believe SaaS solutions offer more robust security than on-premises alternatives. According to industry experts, 57% of telecom companies have integrated AI-driven applications into their operations to improve customer service and operational efficiency.

Software as a Service (SaaS) Market Regional Outlook: North America Leads, Asia Pacific and Europe Drive Growth

The market is geographically studied across North America, South America, Europe, the Middle East & Africa, and Asia Pacific and each region is further studied across countries.

North America

North America Software as a Service (SaaS) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 46.90% to the global market in 2025, with a valuation of USD 148.17 billion, and is projected to reach USD 172.68 billion in 2026. The presence of key providers, such as IBM Corporation, Oracle Corporation, and Microsoft Corporation contributes to the region’s adoption of software as a service application. The region is expected to grow further due to rising innovations in the market. The U.S. has approximately 17,000 software as a service companies, while Canada has around 2,000 companies. Thus, the U.S. is estimated to hold a major market share during the forecast period.

The growth of Software as a Service (SaaS) in the U.S. has been remarkable, valuating for USD 141.06 billion in 2026, driven by technological advancements, increasing demand for cloud-based solutions, and the shift toward digital transformation across industries. A study by industry experts reveals that 70% of U.S. businesses have adopted at least one SaaS solution for enterprise operations, with over 50% of companies running mission-critical applications on software as a service platforms.

As companies migrate to cloud-based environments, SaaS plays a crucial role in enabling this transition. The U.S. has witnessed a massive shift in IT infrastructure, with SaaS applications being seen as more agile, scalable, and cost-effective than on-premises software. According to industry experts, around 90% of U.S. organizations have adopted some form of cloud solution, with SaaS being the most popular deployment model. Additionally, 79% of organizations in the U.S. use cloud-based applications for functions such as CRM, HR management, and accounting. Startups in the U.S. have attracted massive venture capital (VC) investments over the past few years. This influx of capital has fueled innovation, especially in emerging areas such as AI-powered SaaS, automation, and data analytics. In 2023, there were over 60 SaaS unicorns in the U.S.

Asia Pacific

The Asia Pacific market was valued at USD 69.43 billion in 2025, capturing 22.00% of global revenue, and is estimated to reach USD 86.06 billion in 2026, owing to the demand for increased resilience and agility across businesses that are likely to adopt cloud solutions. Developed and developing economies, such as China, Japan, and India, have made significant contributions in facilitating the region's adoption of cloud-driven technologies. Chinese market holds USD 19.44 billion, along with India valuating USD 17.25 billion, and the market in Japan is anticipated to hit USD 17.05 billion in 2026.

Europe

Europe accounted for USD 60.04 billion in 2025, representing 19.00% of the global market share, and is projected to reach USD 70.81 billion in 2026, due to advancements in solutions by the region’s key players. The region’s private and government corporations are also boosting their investments to increase the adoption of cloud solutions. For instance, Google Cloud invested USD 1.2 billion in its German cloud computing program. The investment aimed to expand Germany's cloud infrastructure by adding a data center in Berlin. As per industry experts, 65% of European enterprises are using SaaS solutions for core functions such as customer relationship management (CRM), financial management, and human resources (HR). In contrast, only 40% of European firms were using cloud solutions in 2017. According to European Commission data, 63% of European SMEs use at least one cloud-based application, with 43% using SaaS solutions for business operations such as accounting, project management, and marketing automation. The U.K. market holds USD 12.93 billion, along with Germany valuating USD 14.81 billion and France market anticipated to hit USD 13.19 billion in 2026.

Middle East and Africa

The market in Middle East & Africa reached USD 15.14 billion in 2025, representing 4.80% of total market revenue, and is projected to reach USD 18.43 billion in 2026. The Middle East & Africa is likely to show significant growth in the coming years due to increased investment from cloud service providers. Government investments during the pandemic in large-scale smart city & public management projects and the availability of a wide range of data center and managed service alternatives will support the adoption of new technologies. These factors are also expected to drive the usage of cloud computing in the Middle East. The GCC market stands at USD 7.14 billion in 2025.

South America and Latin America

The market growth in South America has been significant in recent years, accounting for USD 22.90 billion in 2025 driven by increasing digital transformation efforts, the rise of cloud computing, and a growing startup ecosystem. As per PwC report, around 65% of South American companies have integrated at least one solution into their operations, with customer relationship management (CRM) and enterprise resource planning (ERP) being the most common applications.

In 2025, the Latin America market stood at USD 22.9 billion, representing 7.30% of global demand, and is projected to grow to USD 27.59 billion in 2026.

Competitive Landscape: Key Players Focus on Innovation and Strategic Expansion

Leading companies offer software as a service across all businesses. Key market players are creating new solutions, updating tools and technologies, and expanding their scope to enhance their technological capabilities. By working together, companies gain expertise and expand their business by reaching a large customer base. Key players are focused on increasing their market share and customer reach through strategic acquisitions.

Long List of Companies Studied:

- Microsoft Corporation (U.S.)

- SAP SE (Germany)

- IBM Corporation (U.S.)

- Oracle Corporation (U.S.)

- HPE (U.S.)

- ServiceNow (U.S.)

- TCS (India)

- Google LLC (U.S.)

- Cisco Systems, Inc. (U.S.)

- Infosys (India)

- Babbel (Germany)

- Zoho Corporation (India)

- Workiva (Germany)

- Tecent Holdings (China)

- Trend Micro (Japan)

…and more

KEY INDUSTRY DEVELOPMENTS:

- December 2024: Workiva announced data integration between more than 100 cloud, on-premise, and SaaS applications, including Oracle Enterprise Resource Planning (ERP) Cloud and its Wdesk platform.

- October 2024: Salesforce launched a new offering called Government Cloud Premium, Software as a Service and Platform as a Service (PaaS) offering. This offering provides national security and intelligence organizations in the U.S. with a dedicated environment for application development using no-code, low-code, and pro-code options. It also supports workflow automation and features an API-first architecture, making it easier to integrate various government systems and tools.

- September 2024: Palo Alto Networks acquired IBM’s Software as a Service assets QRadar, which enhances strategic alliance and allows more organizations to benefit from their joint next-generation security operations and AI-powered solutions.

- May 2023: Stibo Systems, a provider of master data management software, joined Microsoft's Partner Program as an independent software exporter to create and host cloud-based Software as a Service on Microsoft Azure. Stibo Systems improved its cloud services with support and guidance from Microsoft. This integration would help customers improve short and long-term performance of their cloud investments and resources.

- February 2023: Oracle, the world's largest cloud company, launched Banking Cloud Services, a new set of componentized and constructed banking services. Retail and Corporate banks are able streamline their banking applications to meet customer demands with the help of Oracle’s cloud-based software as a service solution.

Investment Trends: Venture Capital and Public Market Activity Driving SaaS Growth

Over the years, SaaS has attracted significant venture capital (VC) funding, private equity, and public market investment, spurring innovation and the emergence of new market leaders. The SaaS industry has consistently attracted large amounts of venture capital (VC) funding, especially in the past 5-6 years. Startups often raise substantial sums in early and late-stage funding rounds, contributing to rapid scaling and global expansion. In 2021, global SaaS funding surged to an all-time high, with startups raising over USD 50 billion in venture capital across more than 1,500 deals. In 2020 and 2021, several companies opted for mergers with SPACs as an alternative to traditional IPOs. This method allowed them to go public with less regulatory scrutiny and quicker access to capital. DigitalOcean, a cloud infrastructure SaaS provider, went public in 2021 via a Special Purpose Acqusition Companies (SPAC) merger and raised USD 775 million in the process. Unity Software, a SaaS company focused on game development, merged with a SPAC and raised USD 1.3 billion in 2020.

REPORT COVERAGE

The market research report offers a comprehensive analysis, covering key aspects such as leading companies, product offerings, and applications. It also provides insights into the latest market trends and highlights significant industry developments. Additionally, the report examines various factors that have driven market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

CAGR of 18.7% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

| Segmentation | By Deployment Type, Application, Enterprise Type, Industry, and Region |

|

Segmentation |

By Deployment Type

By Application

By Enterprise Type

By Industry

By Region

|

|

Companies Profiled in the Report |

Microsoft Corporation (U.S.), IBM (U.S.), Cisco System (U.S.), Alphabet Inc. (U.S.), Amazon.com, Inc. (U.S.), Salesforce (U.S.), Service Now (U.S.), Fujitsu (Japan), SAP SE (Germany), Infosys (India), TCS (India), and Accenture Plc (Ireland) |

Frequently Asked Questions

The market is projected to reach USD 1,482.44 billion by 2034.

In 2025, the market was valued at USD 315.68 billion.

The market is projected to grow at a CAGR of 18.7% during the forecast period.

The public deployment type leads the market in terms of market share.

Increasing demand for multi-cloud and hybrid cloud adoption is a key factor boosting market growth.

Microsoft Corporation, IBM, Cisco System, SAP SE, Salesforce, and Accenture are the top players in the market.

North America dominated the global market with a share of 46.9% in 2025.

By industry, healthcare sector is expected to grow with a highest CAGR during the forecast period.

Below is the list of companies that are studied in order to estimate the market size and/or understanding the market ecosystem

This list does not necessarily mean that all the below companies are profiled in the report. The report includes profiles of only the top 10 players based on revenue/market share.

Software-as-a-Service Market

- Cisco Systems, Inc.

- Nokia

- Adverity

- Proceedix

- Enhancv

- TalentLyft

- Omilia

- Smartlook

- Templafy

- Dashbird

- MeetingPackage

- Welcome to the Jungle

- FinCompare

- Hosthub

- Talentuno

- 50Skills

- SailPoint Technologies

- Cloudmore

- 10Pearls

- Salesforce

- Microsoft

- Adobe Creative Cloud

- FreshBooks

- Paychex

- Xero

- Zendesk

- RingCentral

- ServiceNow

- Workday

- Twilio

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us