Composites Market Size, Share & Industry Analysis, By Matrix (Polymer Matrix Composites (PMCs) [Fiber {Glass, Carbon, Aramid, & Others} and Resin {Thermoset & Thermoplastic}], Ceramic Matrix Composites (CMCs), and Metal Matrix Composites (MMCs)), By Manufacturing Process (Hand Lay-Up, Injection Molding Process, Resin Transfer Molding (RTM), Filament Winding, Compression Molding, Pultrusion), By Application (Automotive, Building & Construction, Electrical & Electronics Goods, Pipes & tank manufacturing, Consumer Goods, Wind Power, Maritime, Defense & Aviation)), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

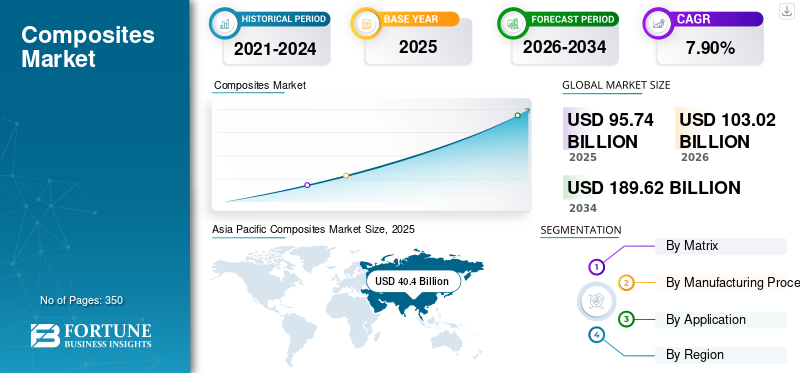

The global composites market size was valued at USD 95.74 billion in 2025. The market is projected to grow from USD 103.02 billion in 2026 to USD 189.62 billion by 2034 at a CAGR of 7.90% during the forecast period. Asia Pacific dominated the composites market with a market share of 42.20% in 2025.

Composites are materials created by combining two or more different substances to produce a new material with enhanced properties. A composite consists of a matrix (a continuous phase that holds everything together) and reinforcement (a dispersed phase that provides strength, stiffness, or other desired attributes). The matrix, often made of polymers, metals, or ceramics, surrounds and supports the reinforcement materials, such as fibers (such as glass, carbon, or aramid) or particles (such as ceramic or metal). This combination results in a material that is stronger, lighter, or more durable than the individual components alone.

Composites are designed to take advantage of the best qualities of each constituent material while minimizing their weaknesses. For instance, fiberglass, a composite of glass fibers and a polymer resin, offers high strength, corrosion resistance, and lightweight properties, making it ideal for applications in boatbuilding, automotive parts, and wind turbine blades. Similarly, carbon fiber-reinforced polymers provide exceptional strength-to-weight ratios, widely used in aerospace, sports equipment, and high-performance vehicles. Due to their customizable properties, composites are increasingly used across various industries, including aerospace, automotive, construction, and marine, to meet specific performance needs and improve product efficiency.

The properties associated with composite materials, such as corrosion resistance, high strength-to-weight ratio, and long lifespan, make them highly suitable for infrastructure projects. These products are used in roads, water/drainage systems, bridges, and seawalls to build resilient structures. Moreover, the aging infrastructure is a potentially massive opportunity for the market. According to the American Road and Transportation Builders Association Report 2019, more than 600,000 bridges in the U.S. are in poor condition and need urgent repairs. Additionally, scientific advancements in composites are gaining momentum due to rapid industrialization and technological developments.

The global market witnessed a marginally lower growth than expected in 2020 owing to the low demand from the automotive and aerospace industries and the lack of availability of raw materials. The volatility in crude oil prices negatively affected the prices of feedstock. The demand for consumer goods for the application of these materials is expected to remain strong in spite of the pandemic due to healthy demand. The building & construction and automotive industries were some of the worst-hit sectors due to the pandemic, and slow recovery is expected in these sectors because of other macroeconomic factors such as job losses and debt crisis. This slow recovery is anticipated to hamper the composites market growth in the long run. Moreover, the changing political landscape and rising trade conflicts between prominent nations such as the U.S. and China are likely to suppress market growth over the forecast period.

The COVID-19 pandemic significantly impacted the market, disrupting supply chains, reducing production capacity, and causing demand fluctuations across key industries. Lockdowns and restrictions slowed manufacturing processes, particularly in the automotive and aerospace sectors, which are major consumers of composites. Travel restrictions and reduced demand for new aircraft severely affected the aerospace industry, while the automotive sector faced challenges with reduced vehicle sales and delays in production schedules. On the other hand, the wind energy and construction sectors showed resilience, with an increased focus on renewable energy and infrastructure projects aiding demand recovery for composites in these applications. However, raw material shortages and logistics disruptions caused price volatility, affecting manufacturers' profitability. As economies reopened and industrial activities resumed, the composites market began recovering, driven by advancements in lightweight materials and sustainable solutions, as industries aimed to enhance efficiency and reduce carbon footprints.

Download Free sample to learn more about this report.

GLOBAL COMPOSITES MARKET LANDSCAPE OVERVIEW

Market Size & Forecast:

- 2025 Market Size: USD 95.74 billion

- 2026 Market Size: USD 103.02 billion

- 2034 Forecast Market Size: USD 189.62 billion

- CAGR: 7.90% from 2026–2034

Market Share:

- Asia Pacific led the global composites market in 2025 with a share of 42.20%, driven by strong demand across automotive, aerospace, construction, and electronics industries. The region saw growth from USD 40.4 billion in 2025 to USD 43.64 billion in 2026.

- By matrix type, polymer matrix composites (PMCs) dominated the market due to their high strength-to-weight ratio, corrosion resistance, and growing usage in automotive and aerospace components.

- By manufacturing process, hand lay-up was the leading technique in 2023 owing to its versatility, low cost, and widespread usage in marine, construction, and wind energy sectors.

- By application, the automotive & transportation segment held the largest share in 2023, accounting for approximately 30.9% of the global market, supported by lightweighting trends and rising electric vehicle adoption.

Key Country Highlights:

- China: The largest contributor within Asia Pacific, China’s automotive segment is estimated to hold a 38.7% share in 2023. Expanding EV production and aerospace programs are propelling composite use.

- United States: Composite applications are growing across the aerospace and defense sectors. Over 50% of the Airbus A350XWB is made of composites, reflecting U.S. aerospace adoption trends.

- Germany: Europe’s composites market is driven by EV manufacturing and strict environmental standards, boosting demand for lightweight materials in vehicles and wind turbines.

- Brazil & Mexico: Latin America shows strong growth potential, supported by booming automotive and construction sectors.

- Saudi Arabia & UAE: Infrastructure megaprojects and investments in oil & gas are pushing composite demand due to their corrosion resistance and lightweight advantages.

LATEST TRENDS

Rising Focus on Sustainable Composites Sustainability to Shape New Opportunities

There is a growing shift toward the use of sustainable composite materials, such as bio-based resins, recycled carbon fibers, and natural fiber reinforcements, such as flax, hemp, and jute. These sustainable alternatives offer reduced carbon footprints and energy consumption compared to traditional composites, aligning with the global push for greener manufacturing practices. Regulatory bodies in regions such as Europe and North America are implementing strict regulations to reduce carbon emissions, encouraging manufacturers to explore sustainable options. For instance, the European Union's Green Deal and various initiatives by the International Maritime Organization (IMO) are pushing industries to adopt sustainable materials to reduce their environmental impact. Additionally, advancements in recycling technologies are enabling the efficient reuse of composite materials, minimizing waste, and promoting circular economy practices. As industries such as automotive, aerospace, and construction increasingly prioritize sustainability, the demand for eco-friendly composites is expected to grow, paving the way for innovative materials that offer both performance and environmental benefits.

Technological Advancements in Composite Manufacturing to Emerge as Significant Trend

Innovations in production processes, such as Automated Fiber Placement (AFP), Resin Transfer Molding (RTM), and 3D printing, are revolutionizing how composite materials are produced and applied. Automated manufacturing techniques such as AFP and RTM allow for precise control over fiber orientation and resin distribution, resulting in stronger, lighter, and more reliable composite structures. These methods also reduce production times and material waste, leading to cost savings and improved efficiency. Additionally, 3D printing, or additive manufacturing, is opening new possibilities for producing complex composite parts with minimal material use and reduced lead times. This technology enables manufacturers to create custom shapes and sizes that would be difficult or impossible to achieve with traditional methods. Such advancements are driving the adoption of composites across various industries, including aerospace, automotive, and construction, where there is a need for high-performance, lightweight materials. As these technologies continue to evolve, they will likely lower the cost of composite production and increase their accessibility, further boosting their demand in global markets. Asia Pacific witnessed a composites market growth from USD 32.34 billion in 2022 to USD 34.74 billion in 2023.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Exceptional Performance of Composites to Drive Market Growth

Composite materials are utilized to serve the needs of customers with a variety of highly complex engineered parts, design patterns, and structures. The composites industry serves several industry verticals, such as automotive, aerospace, marine, consumer goods, wind power, and others. These industries consume composite materials in a variety of ways. This usage is driven by the part performance requirements, regulations, consumer demand, and cost thresholds. For instance, the materials, costs, and process technologies in the aerospace industry are substantially different than those in the automotive industry. Composite materials can meet this diverse demand as they are very diverse themselves. For example, resins, an array of fiber, tooling, process, and finishing options are available and can make any fabrication of nearly any composite part for any application.

Continuous Efforts from Automotive Industry for Lightweight Vehicles to Drive Market Growth

The automotive industry is driven by fuel economy and emission regulations and is thus continuously developing composites for lightweight materials. For instance, currently, in the U.S., the Corporate Average Fuel Economy (CAFÉ) standards mandate a fleet average of 23.2 km/Liter by 2025. In China, the Corporate Average Fuel Consumption (CAFC) also sets a fleet target of 20 km/Liter. European emission regulations mandate an emission of 95g/km of CO2 by 2021, with another reduction of 15% by 2025.

In the automotive industry, more than 100 models currently specify carbon-fiber-reinforced plastic for OEM components. Moreover, the growing trend of the use of thermoplastics in automobiles is also driving the market. The Original Equipment Manufacturers (OEMs) are using automotive composites in the manufacturing of vehicles to reduce vehicle weight, reduce vehicle emissions, and improve fuel efficiency & economy.

MARKET RESTRAINTS

Issues Related to Recycling to Restrict Market Growth

Strict environmental policies and legislations and the increased restrictions and costs for the disposal of landfills are some of the forces restricting the market development. Moreover, the increasing use of life cycle assessment as part of the material selection process in many sectors is also putting composite end-of-life waste management under intense scrutiny. For example, it is estimated that 90% of U.K. composite waste currently goes into landfills, and thus, the composite industry has to tackle significant societal and industrial challenges. Moreover, increasing plastic waste has compelled lawmakers around the world to implement stringent environmental norms. Ban on single-use plastic in various countries has highlighted the steps taken by governments to tackle the concerns arising from plastic waste.

MARKET CHALLENGES

High Production Costs Hamper Market Growth

The high production costs associated with advanced composite materials are one of the challenges for the market. The manufacturing processes for composites, such as resin transfer molding and pultrusion, require significant investment in specialized equipment and technology. Additionally, the raw materials used in composites, such as carbon fiber and specialized resins, are often expensive. These high costs can limit the adoption of composites, particularly in cost-sensitive industries such as automotive and construction. While composites offer numerous benefits, such as lightweight and high-strength properties, the initial investment and ongoing production expenses can deter manufacturers from incorporating them into their products, affecting market growth and product accessibility.

SEGMENTATION ANALYSIS

By Matrix

Polymer Matrix Dominated Market Owing to their Versatility and Effectiveness

Based on the matrix, the market is classified into polymer matrix (PMCs), ceramic matrix (CMCs), and metal matrix (MMCs).

The polymer matrix segment is projected to dominate the market with a share of 74.65% in 2026 and is estimated to record a significant growth rate during the forecast period. The polymer matrix segment is further divided into resin (glass, carbon, aramid, and others) and fiber (thermoset and thermoplastics). This matrix has high mechanical strength, high stiffness, high resistance to wear and corrosion, low density, and high fatigue resistance. These properties make the polymer matrix the most commonly used composite, and hence, most developments and expansions in many companies are with respect to the polymer matrix. For instance, in July 2019, Kordsa, a global player in the reinforcement technologies market and a subsidiary of Sabancı Holding, acquired Axiom Materials, a composite materials manufacturer based in the U.S., to strengthen its capacity to develop new products.

The ceramic segment is expected to witness sustainable growth over the forecast period. The increasing demand for high-performance materials in industries such as aerospace, defense, and automotive is driving the adoption of Ceramic Matrix Composites (CMCs). These materials are prized for their exceptional thermal stability, high strength, and resistance to wear and corrosion, making them ideal for applications that require durability under extreme conditions.

The metal matrix segment is likely to witness considerable growth due to the increasing demand for high-performance materials across various industries, including aerospace, automotive, and defense. MMCs, which combine metal matrices with reinforcing materials such as ceramics or fibers, offer superior strength-to-weight ratios, enhanced thermal conductivity, and improved wear resistance compared to traditional metals.

By Manufacturing Process

Hand Lay-Up Segment Dominated Market Due to Increased Demand from End-use Industries

Based on the manufacturing process, the market is classified into hand lay-up, injection molding process, Resin Transfer Molding (RTM), filament winding, compression molding, pultrusion, and others.

The hand lay-up segment is projected to dominate the market with a share of 52.50% in 2026 and is estimated to maintain dominance throughout the forecast period. The growing demand for lightweight, high-strength materials across multiple industries, combined with advancements in resin formulations and fiber technologies, continues to drive interest in hand lay-up composites. The hand lay-up process offers significant flexibility and cost-effectiveness for producing composite parts, especially for small to medium-sized production runs and custom applications.

The compression molding segment is likely to register significant growth during the forecast period. The rising demand for lightweight and high-strength materials across various industries, such as automotive, aerospace, and consumer goods, is driving the adoption of compression molding. This manufacturing process offers significant advantages, including the ability to produce complex shapes with high precision and consistency, which is essential for meeting the stringent performance and safety standards of modern applications.

The growth of the Resin Transfer Molding (RTM) segment market is driven by the increasing emphasis on lightweight and fuel-efficient components, particularly in the automotive and aerospace sectors, which is driving demand for RTM, as it enables the manufacturing of lightweight, high-performance parts that enhance overall efficiency and reduce emissions.

By Application

To know how our report can help streamline your business, Speak to Analyst

Automotive & Transportation Dominated Market Due to Technological Advancements and Innovations

In terms of application, the market is segmented into automotive & transportation, building & construction, electrical & electronics goods, pipes & tank manufacturing, consumer goods, wind power, maritime, defense & aviation, and others.

The automotive segment is projected to dominate the market with a share of 32.20% in 2026 as these materials are widely used in this industry to reduce the weight of vehicles. For instance, BMW opted to use composites for their life models, such as the BMW M3, BMW M4, BMW i8, and BMW i3, for weight-saving, emission-reduction, part-consolidation, strength and safety gains, and improved efficiency.

The building & construction segment is expected to grow considerably during the forecast period owing to the increasing demand for durable, lightweight, and high-performance materials. Composites, such as fiber-reinforced polymers (FRPs) and advanced resins, offer superior strength, resistance to corrosion, and reduced weight compared to traditional materials such as steel and concrete. These materials contribute to energy savings through improved insulation properties and reduce the environmental impact of construction projects due to their longevity and lower maintenance requirements.

The defense & aviation segment is predicted to witness notable growth in the coming years, driven by the increasing demand for high-performance and lightweight materials that can enhance the efficiency and operational capabilities of aircraft and defense systems. Composites, such as carbon fiber-reinforced polymers (CFRP) and aramid fibers, offer superior strength-to-weight ratios, corrosion resistance, and durability compared to traditional materials such as aluminum and steel. The automotive segment is expected to hold a 30.9% share in 2023.

COMPOSITES MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Composites Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market was valued at USD 40.4 billion in 2025, capturing 42.20% of global revenue, and is estimated to reach USD 43.64 billion in 2026. Asia Pacific held the majority share of the global market. The region is set to emerge as the fastest-growing market over the forecast period. The regional growth is due to the growing demand in major industries such as automotive & transportation, aerospace, building & construction, and electrical & electronics, which is expected to create a humongous opportunity for players in this market. Moreover, the rapid development of countries such as China and India and the existence of major manufacturers, such as Toray Industries Inc. and Mitsubishi Chemical Holdings Corporation, is expected to boost the regional market positively. The Japan market is projected to reach USD 5.17 billion by 2026, the China market is projected to reach USD 18.26 billion by 2026, and the India market is projected to reach USD 11.29 billion by 2026.

- Asia Pacific witnessed a growth from USD 40.4 Billion in 2025 to USD 43.64 Billion in 2026.

- In China, the Automotive segment is estimated to hold a 38.7% market share in 2023.

To know how our report can help streamline your business, Speak to Analyst

North America

North America contributed 29.70% to the global market in 2025, with a valuation of USD 28.42 billion, and is projected to reach USD 30.57 billion in 2026. The market in North America is growing significantly due to rising demand from the automotive and defense & aerospace industries. The use of product in aerospace has gained momentum in the past few decades, with more than 50% of the latest Airbus aircraft under the A350XWB lineup being made up of composite materials as compared to the older fleet, which only used 2–5% aerospace composites. The U.S. market is projected to reach USD 25.35 billion by 2026.

Europe

Europe accounted for USD 22.27 billion in 2025, representing 23.30% of the global market share, and is projected to reach USD 23.85 billion in 2026. Europe is expected to make substantial gains during the forecast timeframe. Rising spending on electrical vehicles supported by environmental norms has mainly led to the increasing adoption of lightweight materials in the automotive manufacturing in the region. The UK market is projected to reach USD 5.95 billion by 2026, while the Germany market is projected to reach USD 7.75 billion by 2026.

Latin America

In 2025, the Latin America market stood at USD 1.71 billion, representing 1.80% of global demand, and is projected to grow to USD 1.84 billion in 2026. Latin America is expected to showcase considerable growth in the global market during the forecast period, driven by developments in the automotive, aerospace, and construction sectors. Brazil and Mexico are leading in adopting composites due to their expanding automotive and construction industries. The region’s growing focus on infrastructure development and energy efficiency supports the use of composites for durable and cost-effective solutions.

Middle East & Africa

The market in Middle East & Africa reached USD 2.94 billion in 2025, representing 3.10% of total market revenue, and is projected to reach USD 3.14 billion in 2026. The Middle East & Africa region is expected to show tremendous growth. The growth of the market is driven by infrastructure development and the oil and gas sector. Countries such as Saudi Arabia and the UAE are investing in large-scale construction projects and industrial applications, where composites offer benefits such as corrosion resistance and high strength-to-weight ratios.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players to Focus on New Product Development and Invest in R&D to Maintain Dominance in Market

The competitive landscape of the market is rather fragmented, with several global & regional players operating. Some of the key players in the market include Owens Corning, Toray Industries, Inc., Teijin Limited, Hexcel Corporation, and Solvay. These players are engaged significantly in research and development to innovate and improve their product offerings. The adoption of various strategic developments, such as expansion and joint ventures, also helps them gain a competitive edge in the market. Moreover, the key players are focused on grabbing long-term supply contracts with the end-users to ensure the growth of their businesses. For example, in January 2019, Teijin Limited was awarded an extension contract to supply carbon fiber to Bombardier for the AIRBUS A220 till 2025.

LIST OF KEY MARKET PLAYERS PROFILED IN THE REPORT:

- Owens Corning (U.S.)

- Toray Industries, Inc. (Japan)

- Teijin Limited (Japan)

- Mitsubishi Chemical Holdings Corporation (Japan)

- Hexcel Corporation (U.S.)

- SGL Carbon (Germany)

- Huntsman International LLC. (U.S.)

- Solvay (Belgium)

- Exel Group(France)

- Veplas d.d. (Slovenia)

- Composite Solutions (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- June 2024: Plastics processor Ensinger is investing in production capacity expansion for its composites division. Very soon, a high-performance double belt press will begin operation in Rottenburg-Ergenzingen. The new facility enables the efficient production of thermoplastics composite materials.

- April 2024: Aurora Flight Sciences (Bridgeport, W.Va., U.S.), a Boeing Company, expanded its manufacturing facility in Bridgeport, West Virginia. The expansion adds almost 50,000 square feet to the facility to support significant growth for building high-quality composite components and assemblies across both current production programs and new opportunities in the aerospace industry.

- March 2024: Toray Advanced Composites launched the new product Toray Cetex TC915 PA+ into its extensive portfolio. Toray Cetex TC915 PA+ is excellent for sporting goods, high-performance industrial applications, automotive structures, energy (oil/gas & hydrogen), Urban Air Mobility (UAM), and Unmanned Aerial Systems (UAS) applications.

- July 2023: Toray Advanced Composites announced the planned expansion of its Morgan Hill (CA, USA) plant operations. The new facility will add 74,000 square feet (6,800 square meters) to the existing campus facilities.

- September 2019: INEOS Enterprises, a chemical company, completed the acquisition of the entire composites business from Ashland Global Holdings Inc. along with the BDO facility in Germany. This acquisition will help INEOS to strengthen its position in the global market.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, manufacturing processes used to produce these products, and end-use industries of the product. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, it encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) and Volume (Million Ton) |

|

Growth Rate |

CAGR of 7.90% from 2026 to 2034 |

|

Segmentation |

By Matrix

|

|

By Manufacturing Process

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 95.74 billion in 2025 and is projected to record a valuation of USD 189.62 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 40.4 billion.

Recording a CAGR of 7.90%, the market will exhibit steady growth during the forecast period.

In 2026, the automotive application segment led the market.

Growing demand from the automotive industry will drive the growth of the market.

Asia Pacific held the highest market share in 2025.

Properties such as durability, resistance properties, efficiency, and versatility will drive product adoption.

- 2021-2034

- 2025

- 2021-2024

- 350

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us