GPU as a Service Market Size, Share & Industry Analysis, By Deployment Model (Private GPU Cloud, Public GPU Cloud, and Hybrid GPU Cloud), By Enterprise Type (SMEs and Large Enterprise), By Pricing Model (Pay-as-you-go and Subscription-based), By Application (Healthcare, BFSI, Manufacturing, IT & Telecommunication, Automotive, and Others), and Regional Forecast, 2026 – 2034

(Offer valid till 15th Jul 2026)

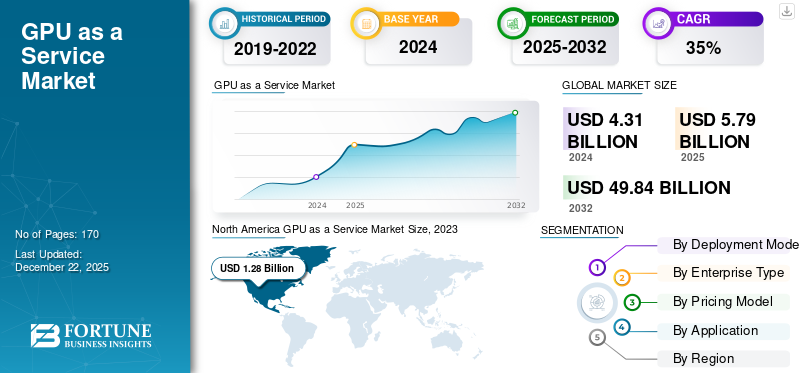

GPU as a Service Market Size and Industry Overview

The global GPU as a service market size was valued at USD 6.07 billion in 2025. The market is projected to grow from USD 8.66 billion in 2026 to USD 162.54 billion by 2034, exhibiting a CAGR of 44.3% during the forecast period. North America dominated the gpu as a service market with a market share of 39.37% in 2025.

GPU as a Service (GPUaaS) market is a cloud-based model that provides on-demand access to high-performance graphics processing units without requiring customers to purchase or manage physical hardware. It enables organizations to run compute-intensive workloads such as artificial intelligence training and inference, machine learning, data analytics, simulation, rendering, and high-performance computing through remote infrastructure.

These companies are focusing on new product launches and investment in R&D activity to expand their product portfolio. For instance, In March 2024, Microsoft Corporation launched the Azure ND H200 v5 VM series optimized for AI supercomputing, expanding Azure’s GPU instance portfolio for large-scale training and inference workloads.

Major GPUaaS providers such as Amazon Web Services, Microsoft Corporation, Alphabet, Inc., Alibaba Group, IBM Corporation are strengthening their competitive position by mergers and acquisitions (M&A) activities and expanding product offerings to increase their market shares.

Download Free sample to learn more about this report.

Impact of Generative-AI

Generative AI is Transforming GPUaaS into a Core Infrastructure Layer for Scalable AI Computing

The rapid adoption of Generative AI (Gen AI) has significantly accelerated demand for GPUaaS as enterprises require high-performance computing infrastructure to train and deploy large AI models. Training advanced AI models such as large language models and multimodal systems requires thousands of GPUs operating simultaneously, making cloud based GPU access more cost effective than building in house infrastructure. As a result, organizations across sectors including IT, finance, healthcare, and media are increasingly relying on GPUaaS platforms to scale AI workloads without large upfront capital investment.

Cloud providers and specialized GPUaaS vendors are expanding their GPU clusters and AI optimized infrastructure to support this demand. For instance, the training of large AI models can require several thousand GPUs running for weeks, consuming massive computing resources and power. This surge in AI workloads is driving hyperscalers and GPUaaS providers to invest heavily in advanced GPU architectures, high speed networking, and AI optimized data centers.

GPU as a Service Market Trends

Rising Adoption and Integration of Cloud GPUs Across Several Industries to Enhance Market Growth

Cloud GPU instances offer cloud applications without installing GPUs on the local device. These GPUs deliver more flexibility and bandwidth, leading to less hardware costs and total cost of ownership. The GPUs have been popular in the gaming industry for decades, and they are steadily gaining traction in healthcare, finance, architecture, data analytics, cybersecurity, and other sectors, owing to the wide range of advantages over traditional processors.

The cloud integration further elevates customers' financial services experience with risk management, quick data-driven predictions, and response to critical requests.

- In April 2025, as per the industry survey, a 60% increase in cloud GPU adoption for industries such as automotive, healthcare, and gaming. This surge is driven by the demand for AI-powered solutions, where businesses increasingly turn to GPUaaS to boost processing power without investing in on-premise hardware.

The rapid evolution of large, complex simulations and deep learning workloads has increased the use of HPC products and services to process large volumes of datasets, run analytics, and other applications. Businesses in almost every sector are increasingly employing GPU-assisted HPC infrastructure for data-intensive computing.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for GPU-Intensive Applications and Technological Advancements to Fuel Market Growth

The rise in the use of GPU-intensive applications such as 3D graphics rendering, machine learning, scientific computing, cryptocurrency mining, blockchain, and video editing has been driving the GPU as a service market growth. More businesses and individuals are seeking cloud-based GPU solutions to accelerate their computing needs without investing heavily in on-premises infrastructure.

Cloud-based GPU services have become more scalable than traditional on-premise solutions. Cloud GPU providers offer flexibility and cost-effectiveness, allowing businesses to scale their GPU usage based on demand without worrying about physical infrastructure. This shift has contributed to more businesses adopting cloud GPU services.

- In November 2025, ESDS Software Solution Limited introduced a sovereign‑grade GPUaaS platform designed to support high‑performance computing needs for AI, ML, and large language models (LLMs) in business, government, and research sectors, highlighting broader adoption of GPUaaS solutions.

MARKET RESTRAINTS

Data Security Concerns and Less Awareness in Developing Economies to Hamper Market Growth

Data security is one of the major issues that is anticipated to limit the market growth. Since the GPUaaS solution stores and processes data on the cloud, there is a higher risk of data loss, unauthorized access, and cyberattacks.

- In May 2024, a 2024 Cloud Security Report found that 61% of organizations reported experiencing cloud security breaches within the past year, with data security breaches emerging as the most common type of incident. This highlights that data loss, unauthorized access, and security risks remain significant concerns for cloud adoption.

Some cloud providers have limited availability of certain GPU types due to high demand or supply constraints. This can lead to challenges in scaling up GPU resources when needed.

MARKET OPPORTUNITIES

Integration of Cloud GPUs Across AI and Machine Learning Operations Boosts Market Growth

Integrating Cloud GPUs with AI and ML enhances productivity and reduces operational costs by enabling businesses to run these resource-intensive models without the need for on-premises infrastructure. ChatGPT, an AI-powered chatbot, has made it possible to create interaction-style conversations. ChatGPT is free for the users; it requires more powerful graphics processing units (GPUs) to handle more complex AI workloads. For instance,

- In October 2025, Nvidia Corporation, in collaboration with major hyperscalers, announced GPUaaS instances powered by Blackwell architecture GPUs, designed to accelerate LLM training and AI inference. These new instances promise up to 2× performance improvement over prior-generation A100/P5 instances for AI workloads.

The rapid evolution of deep learning has increased the use of HPC technology by researchers and engineers to produce large data, run analytics, and others in less time and price than traditional computing

Segmentation Analysis

By Deployment Model

Rising Deployment of Private GPU Cloud by Enterprise to Propel Segmental Growth

Based on the deployment model, the market is divided into private GPU cloud, public GPU cloud, and hybrid GPU cloud.

Private GPU cloud for the largest GPU as a service market share as enterprises prefer greater control over their computing infrastructure, data security, and regulatory compliance. Many organizations handling sensitive data, such as financial institutions, healthcare providers, and government agencies, rely on private cloud environments to maintain strict data governance and privacy standards. Private cloud also offers dedicated resources, which improves performance and reduces latency for critical workloads. Additionally, enterprises adopting AI, analytics, and high performance computing often deploy these workloads on private cloud environments to ensure reliability and security. As a result, the demand for private cloud infrastructure continues to remain strong across large enterprises globally.

Hybrid GPU cloud is anticipated to rise with a CAGR of 44.4% over the forecast period owing to the growing need for flexible and scalable IT infrastructure that combines both private and public cloud environments. Organizations are increasingly adopting hybrid cloud strategies to balance security with scalability, allowing sensitive workloads to remain on private infrastructure while leveraging public cloud for additional computing capacity.

By Enterprise Type

Strong Financial Capabilities and Higher Investment by Large Enterprise to Propel Market Growth

Based on the enterprise type, the market is divided into large enterprise and SMEs.

Large enterprise accounted for the largest market share owing to their strong financial capabilities and higher investment in advanced computing infrastructure. These organizations deploy GPU powered platforms to support large scale AI training, data analytics, and high performance computing workloads across multiple operations. Large enterprises also require dedicated computing power to handle complex applications such as autonomous systems, financial modeling, and advanced research. For instance, companies such as Microsoft and Google deploy thousands of GPUs in their cloud infrastructure to train and operate large AI models, which significantly drives demand for GPU based services among large organizations.

SMEs are anticipated to rise with a CAGR of 45.5% over the forecast period driven by the growing availability of affordable cloud based GPU services and the rising adoption of AI tools among startups and small businesses.

By Pricing Model

Rising Adoption of Pay-as-you-go Pricing Model to Propel Segmental Growth

Based on the pricing model, the market is bifurcated into pay-as-you-go and subscription-based.

Pay-as-you-go accounted for the largest market share in 2025. This model allows enterprises to pay only for the computing resources they consume, eliminating the need for large upfront investments in GPU infrastructure. It is particularly beneficial for AI training, experimentation, and short term high performance computing tasks where resource demand fluctuates. For instance, developers training AI models on platforms such as Amazon Web Services can access GPU instances on demand and pay only for the hours used, making it a preferred pricing option for startups, researchers, and enterprises conducting intermittent AI workloads.

Subscription-based is anticipated to rise with a CAGR of 40.0% over the forecast period driven by the increasing demand for predictable costs and long term access to GPU resources. Enterprises that run continuous AI workloads, machine learning operations, and large scale data analytics often prefer subscription plans that provide reserved GPU capacity and stable pricing.

By Application

To know how our report can help streamline your business, Speak to Analyst

Increasing Deployment of AI Driven Applications in IT & Telecom to Propel Segmental Growth

Based on the application, the market is divided into healthcare, BFSI, manufacturing, IT & telecommunication, automotive, and others.

IT & telecommunication accounted for the largest market share owing to increasing deployment of AI driven applications, cloud computing services, and large scale data processing requirements. Telecom operators and technology companies require high performance GPU infrastructure to support network optimization, data analytics, and AI model training. Additionally, the rapid expansion of cloud services and data centers is significantly increasing the demand for GPU resources in this sector. For instance, companies such as Google and Microsoft use large GPU clusters in their cloud platforms to support AI services, machine learning workloads, and advanced data processing applications.

Manufacturing is anticipated to rise with a CAGR of 47.7% over the forecast period driven by the growing adoption of AI powered automation, digital twins, and predictive maintenance solutions in industrial operations. GPU computing enables manufacturers to process large volumes of sensor and production data for real time monitoring and optimization of factory processes.

GPU as a Service Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America GPU as a Service Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valuing at USD 2.252 billion, and also maintained the leading share in 2026, with USD 3.009 billion. The North America market is gaining traction owing to the presence of major players, including Amazon Web Services, Inc., Vast.ai, Google LLC, and Microsoft Corporation, among others. The key players in the region are adopting strategies such as acquisition, partnership, and product launches to expand their business, enhance their presence, and improve their customer base.

- In June 2025, Google announced the general availability of NVIDIA GPU support on its Cloud Run platform, enabling enterprises to access GPUs with pay-per-use billing for AI inference and model deployment. This launch was aimed at expanding Google’s AI infrastructure portfolio and attracting customers requiring scalable GPU resources for generative AI and machine learning workloads.

U.S. GPU as a Service Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market value was approximated at around USD 1.50 billion in 2025, accounting for roughly 25.0% of global sales.

Asia Pacific

Asia Pacific will grow at a highest CAGR of 54.9% during the forecast period and recorded a valuation of USD 1.29 billion in 2025. The region’s market growth is owing to aggressive expansion of high-performance compute infrastructure that supports advanced workloads and reduces latency for regional users. For example, in November 2025, GMI Cloud announced a USD 500 million AI data center project in Taiwan that will house around 7,000 NVIDIA Blackwell GB300 GPUs and offer GPUaaS capabilities once operational by 2026, illustrating strong investment in local GPU capacity to serve enterprise demand.

Japan GPU as a Service Market

The Japan market size in 2025 was recorded at around USD 0.17 billion, accounting for roughly 3.0% of global revenue. The region’s growth is attributed to the rapid adoption of artificial intelligence, high performance computing, and advanced robotics across key industries. The country has a strong technological ecosystem with major investments in AI research, semiconductor development, and cloud infrastructure. Japanese enterprises are increasingly utilizing GPU powered cloud platforms to accelerate machine learning, data analytics, and autonomous system development.

China GPU as a Service Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 0.40 billion, representing roughly 7% of global sales.

India GPU as a Service Market

The Indian market value in 2025 was recorded at around USD 0.30 billion, accounting for roughly 5% of global revenue.

Europe

Europe is projected to record a second highest growth rate of 41.8% in the coming years. The region’s growth is being propelled by expanding local high-performance GPU infrastructure and deep strategic collaborations between global technology leaders and regional providers. A key example is NVIDIA GTC Paris building Europe’s first industrial AI cloud in Germany featuring 10,000 GPUs to support manufacturing and engineering workloads, with partners including Siemens, Ansys, and Cadence, demonstrating strong industrial demand for service-oriented GPU compute.

U.K. GPU as a Service Market

The U.K. market in 2025 was valued at around USD 0.26 billion, representing roughly 4.0% of global revenues.

Germany GPU as a Service Market

Germany’s market reached approximately USD 0.36 billion in 2025, equivalent to around 6.0% of global sales.

South America and Middle East & Africa

South America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The South America market reached a valuation of USD 0.32 billion in 2025. South America and the Middle East & Africa market growth is owing to the increasing adoption of cloud computing, rising investments in digital infrastructure, and growing demand for artificial intelligence and data analytics across emerging economies. In the Middle East & Africa, the GCC reached a value of USD 0.16 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Product Launch and Enhancement to Reinforce Competitive Advantage

The growing adoption of AI and machine learning across various industries has increased the demand for robust computing resources. Key players are developing high-performance hardware GPUs by integrating and deploying virtualized GPU resources and offering them to organizations. Moreover, with the help of service providers and cloud offerings, companies aim to gain a strong market presence across geographies.

- In May 2025, NVIDIA launched DGX Cloud Lepton, a global AI compute platform and marketplace connecting developers to a large network of GPU resources from cloud partners, enabling scalable access to tens of thousands of GPUs for AI workloads.

- In November 2024, Rackspace Technology launched an on‑demand GPU‑as‑a‑Service powered by NVIDIA accelerated computing, expanding its multicloud and AI infrastructure offerings. This product enhancement provides customers with flexible, scalable GPU resources for AI, ML, analytics, and rendering workloads without upfront capital investment, aligning with market demand for flexible GPUaaS solutions.

The enhancement and expansion of the current product portfolio raise the position of vendors in the market.

LIST OF KEY GPU AS A SERVICE COMPANIES PROFILED

- Alphabet, Inc. (U.S.)

- Alibaba Group Holding Limited (China)

- Microsoft Corporation (U.S.)

- IBM Corporation (U.S.)

- Amazon Web Services, Inc. (U.S.)

- Oracle Corporation (U.S.)

- Tencent Cloud (China)

- Lambda (U.S.)

- CoreWeave (U.S.)

- VULTR (U.S.)

- Other Companies

KEY INDUSTRY DEVELOPMENTS

- November 2025: Lambda announced a multibillion-dollar agreement with Microsoft to deploy AI infrastructure powered by tens of thousands of NVIDIA GPUs, expanding available GPU cloud capacity for enterprise AI workloads.

- October 2025: Oracle and AMD announced an expanded collaboration, with OCI set to become a launch partner for a large AI supercluster powered by AMD Instinct MI450 Series GPUs, broadening Oracle’s accelerator portfolio beyond NVIDIA for AI scale use cases.

- September 2025: Alibaba Cloud unveiled full-stack AI updates and announced major upgrades to AI infrastructure, reinforcing its role as a cloud provider focused on efficient training and deployment of large AI models.

- April 2025: Google Cloud announced the expansion of its AI Hypercomputer architecture by introducing support for NVIDIA Blackwell GPUs, designed to accelerate large-scale generative AI and foundation model workloads. The upgrade enhances Google Cloud’s GPU portfolio for training and inference, offering improved performance, networking efficiency, and scalable AI cluster capabilities for enterprises deploying large language models (LLMs).

- February 2025: AWS expanded its partnership with Anthropic, committing additional infrastructure support to scale foundation model training and inference workloads on AWS GPU clusters. The collaboration reinforces AWS’s position as a key infrastructure provider for AI model developers.

REPORT COVERAGE

The global GPU as a service market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 44.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Deployment Model, Enterprise Type, Pricing Model, Application, and Region |

| By Deployment Model |

|

| By Enterprise Type |

|

| By Pricing Model |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 6.07 billion in 2025 and is projected to reach USD 162.54 billion by 2034.

In 2025 the market value stood at USD 2.39 billion.

The device market is expected to exhibit a CAGR of 44.3% during the forecast period.

By application, the IT & telecommunication segment is expected to lead the market.

The rising demand for GPU-Intensive applications coupled with technological advancements to fuel the market growth.

AWS, Microsoft, Alphabet, Alibaba, and IBM are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us